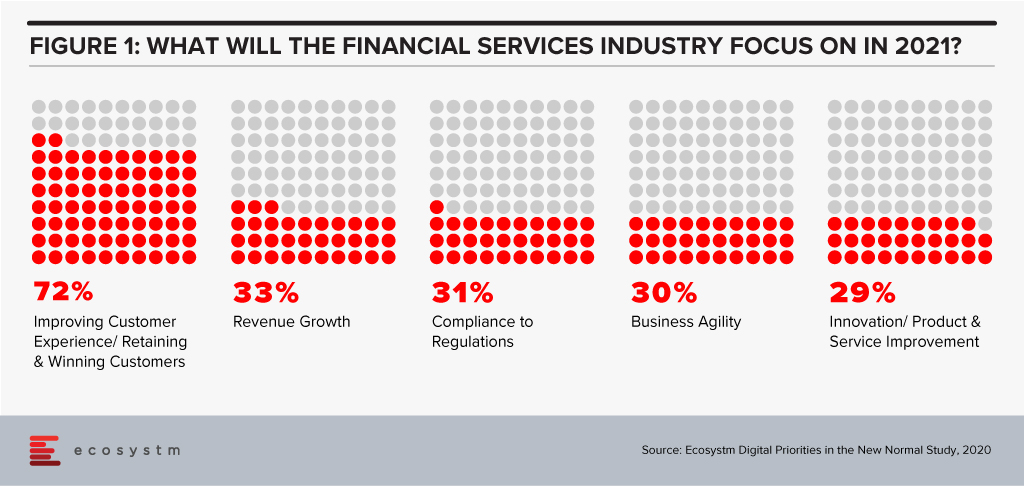

The disruption that we faced in 2020 has created a new appetite for adoption of technology and digital in a shorter period. Crises often present opportunities – and the FinTech and Financial Services industries benefitted from the high adoption of digital financial services and eCommerce. In 2021, there will be several drivers to the transformation of the Financial Services industry – the rise of the gig economy will give access to a larger talent pool; the challenges of government aid disbursement will be mitigated through tech adoption; compliance will come sharply back into focus after a year of ad-hoc technology deployments; and social and environmental awareness will create a greater appetite for green financing. However, the overarching driver will be the heightened focus on the individual consumer (Figure 1).

2021 will finally see consumers at the core of the digital financial ecosystem.

Ecosystm Advisors Dr. Alea Fairchild, Amit Gupta and Dheeraj Chowdhry present the top 5 Ecosystm predictions for FinTech in 2021 – written in collaboration with the Singapore FinTech Festival. This is a summary of the predictions; the full report (including the implications) is available to download for free on the Ecosystm platform.

The Top 5 FinTech Trends for 2021

#1 The New Decade of the ‘Empowered’ Consumer Will Propel Green Finance and Sustainability Considerations Beyond Regulators and Corporates

We have seen multiple countries set regulations and implement Emissions Trading Systems (ETS) and 2021 will see Environmental, Social and Governance (ESG) considerations growing in importance in the investment decisions for asset managers and hedge funds. Efforts for ESG standards for risk measurement will benefit and support that effort.

The primary driver will not only be regulatory frameworks – rather it will be further propelled by consumer preferences. The increased interest in climate change, sustainable business investments and ESG metrics will be an integral part of the reaction of the society to assist in the global transition to a greener and more humane economy in the post-COVID era. Individuals and consumers will demand FinTech solutions that empower them to be more environmentally and socially responsible. The performance of companies on their ESG ratings will become a key consideration for consumers making investment decisions. We will see corporate focus on ESG become a mainstay as a result – driven by regulatory frameworks and the consumer’s desire to place significant important on ESG as an investment criterion.

#2 Consumers Will Truly Be ‘Front and Centre’ in Reshaping the Financial Services Digital Ecosystems

Consumers will also shape the market because of the way they exercise their choices when it comes to transactional finance. They will opt for more discrete solutions – like microfinance, micro-insurances, multiple digital wallets and so on. Even long-standing customers will no longer be completely loyal to their main financial institutions. This will in effect take away traditional business from established financial institutions. Digital transformation will need to go beyond just a digital Customer Experience and will go hand-in-hand with digital offerings driven by consumer choice.

As a result, we will see the emergence of stronger digital ecosystems and partnerships between traditional financial institutions and like-minded FinTechs. As an example, platforms such as the API Exchange (APIX) will get a significant boost and play a crucial role in this emerging collaborative ecosystem. APIX was launched by AFIN, a non-profit organisation established in 2018 by the ASEAN Bankers Association (ABA), International Finance Corporation (IFC), a member of the World Bank Group, and the Monetary Authority of Singapore (MAS). Such platforms will create a level playing field across all tiers of the Financial Services innovation ecosystem by allowing industry participants to Discover, Design and rapidly Deploy innovative digital solutions and offerings.

#3 APIfication of Banking Will Become Mainstream

2020 was the year when banks accepted FinTechs into their product and services offerings – 2021 will see FinTech more established and their technology offerings becoming more sophisticated and consumer-led. These cutting-edge apps will have financial institutions seeking to establish partnerships with them, licensing their technologies and leveraging them to benefit and expand their customer base. This is already being called the “APIficiation” of banking. There will be more emphasis on the partnerships with regulated licensed banking entities in 2021, to gain access to the underlying financial products and services for a seamless customer experience.

This will see the growth of financial institutions’ dependence on third-party developers that have access to – and knowledge of – the financial institutions’ business models and data. But this also gives them an opportunity to leverage the existent Fintech innovations especially for enhanced customer engagement capabilities (Prediction #2).

#4 AI & Automation Will Proliferate in Back-Office Operations

From quicker loan origination to heightened surveillance against fraud and money laundering, financial institutions will push their focus on back-office automation using machine learning, AI and RPA tools (Figure 3). This is not only to improve efficiency and lower risks, but to further enhance the customer experience. AI is already being rolled out in customer-facing operations, but banks will actively be consolidating and automating their mid and back-office procedures for efficiency and automation transition in the post COVID-19 environment. This includes using AI for automating credit operations, policy making and data audits and using RPA for reducing the introduction of errors in datasets and processes.

There is enormous economic pressure to deliver cost savings and reduce risks through the adoption of technology. Financial Services leaders believe that insights gathered from compliance should help other areas of the business, and this requires a completely different mindset. Given the manual and semi-automated nature of current AML compliance, human-only efforts slow down processing timelines and impact business productivity. KYC will leverage AI and real-time environmental data (current accounts, mortgage payment status) and integration of third-party data to make the knowledge richer and timelier in this adaptive economic environment. This will make lending risk assessment more relevant.

#5 Driven by Post Pandemic Recovery, Collaboration Will Shape FinTech Regulation

Travel corridors across border controls have started to push the boundaries. Just as countries develop new processes and policies based on shared learning from other countries, FinTech regulators will collaborate to harmonise regulations that are similar in nature. These collaborative regulators will accelerate FinTech proliferation and osmosis i.e. proliferation of FinTechs into geographies with lower digital adoption.

Data corridors between countries will be the other outcome of this collaboration of FinTech regulators. Sharing of data in a regulated environment will advance data science and machine learning to new heights assisting credit models, AI, and innovations in general. The resulting ‘borderless nature’ of FinTech and the acceleration of policy convergence across several previously siloed regulators will result in new digital innovations. These Trusted Data Corridors between economies will be further driven by the desire for progressive governments to boost the Digital Economy in order to help the post-pandemic recovery.

Public sector organisations are looking at 2021 as the year where they either hobble back to normalcy or implement their successful pilots (that were honed under tremendous pressure). Ecosystm research finds that 60% of government agencies are looking at 2021 as the year they make a recovery to normal – or the normal that finally emerges. The path to recovery will be technology-driven, and this time they will look at scalability and data-driven intelligence.

Ecosystm Advisors Alan Hesketh, Mike Zamora and Sash Mukherjee present the top 5 Ecosystm predictions for Cities of the Future in 2021. This is a summary of our Cities of the Future predictions – the full report (including the implications) is available to download for free on the Ecosystm platform here.

The Top 5 Cities of the Future Trends for 2021

#1 Cities Will Re-start Their Transformation Journey by Taking Stock

In 2021 the first thing that cities will do is introspect and reassess. There have been a lot of abrupt policy shifts, people changes, and technology deployments. Most have been ad-hoc, without the benefit of strategy planning, but many of the services that cities provide have been transformed completely. Government agencies in cities have seen rapid tech adoption, changes in their business processes and in the mindset of how their employees – many who were at the frontline of the crisis – provide citizen services.

Technology investments, in most cases, took on an unexpected trajectory and agencies will find that they have digressed from their technology and transformation roadmap. This also provides an opportunity, as many solutions would have gone through an initial ‘proof-of-concept’ without the formal rigours and protocols. Many of these will be adopted for longer term applications. In 2021, they will retain the same technology priorities as 2020, but consolidate and strengthen on their spend.

#2 Cities Will be Instrumented Using Intelligent Edge Devices

The capabilities of edge devices continue to increase dramatically, while costs decline. This reduces the barriers to entry for cities to collect and analyse significantly more data about the city and its people. Edge devices move computational power and data storage as close to the point of usage as possible to provide good performance. Devices range from battery powered IoT devices for data collection through to devices such as smart CCTV cameras with embedded pattern recognition software.

Cities will develop many use cases for intelligent edge devices. These uses will range from enhancing old assets using newer approaches to data collection – through to accelerating the speed and quality of the build of a new asset. The move to data-driven maintenance and decision-making will improve outcomes.

#3 COVID-19 Will Impact City Design

The world has received a powerful reminder of the vulnerability of densely populated cities, and the importance of planning and regulating public health. COVID-19 will continue to have an impact on city design in 2021.

A critical activity in controlling the pandemic in this environment is the test-and-trace capabilities of the local public health authorities. Technology to provide automated, accurate, contact tracing to replace manual efforts is now available. Scanning of QR codes at locations visited is proving to be the most widely adopted approach. The willingness of citizens to track their travels will be a crucial aid in managing the spread of COVID-19.

Early detection of new disease outbreaks, or other high-risk environmental events, is essential to minimise harm. Intelligent edge devices that detect the presence of viruses will become crucial tools in a city’s defence.

Intelligent edge devices will also play a role in managing building ventilation. Well-ventilated spaces are an important factor in controlling virus transmission. But a limited number of buildings have ventilation systems that are capable of meeting those requirements. Property owners will begin to refit their facilities to provide better air movement.

#4 Technology Vendors Will Emerge as the Conductors of Cities of the Future

The built environment comprises not only of the physical building, but also the space around the buildings and building operations. The real estate developer/investor owns the building – the urban fabric, the relationship of buildings to each other, the common space and the common services provided to the city, is owned by the City. The question is who will coordinate the players, e.g. business, citizens, government and the built environment. Ideally the government should be the conductor. However, they may not have sufficient experience or knowledge to properly implement this role. This means a capable and knowledgeable neutral consultant will at least initially fill this role. There is an opportunity for a technology vendor to fill that consulting role and impact the city fabric. This enhanced city environment will be requested by the Citizen, driven by the City, and guided by Technology Vendors. 2021 will see leading technology vendors working very closely with cities.

#5 Compliance Will be at the Core of Citizen Engagement Initiatives

Many Smart Cities have long focused on online services – over the last couple of years mobile apps have further improved citizen services. In 2020, the pandemic challenged government agencies to continue to provide services to citizens who were housebound and had become more digital savvy almost overnight. And many cities were able to scale up to fulfill citizen expectations.

However, in 2021 there will be a need to re-evaluate measures that were implemented this year – and one area that will be top priority for public sector agencies is compliance, security and privacy.

The key drivers for this renewed focus on security and privacy are:

- The need to temper the focus of ‘service delivery at any cost’ and further remind agencies and employees that security and privacy must comply with standard to allow the use of government data.

- The rise of cyberattacks that target not only essential infrastructure, but also individual citizens and small and medium enterprises (SMEs).

- The rise of app adoption by city agencies – many that have been developed by third parties. It will become essential to evaluate their compliance to security and privacy requirements.

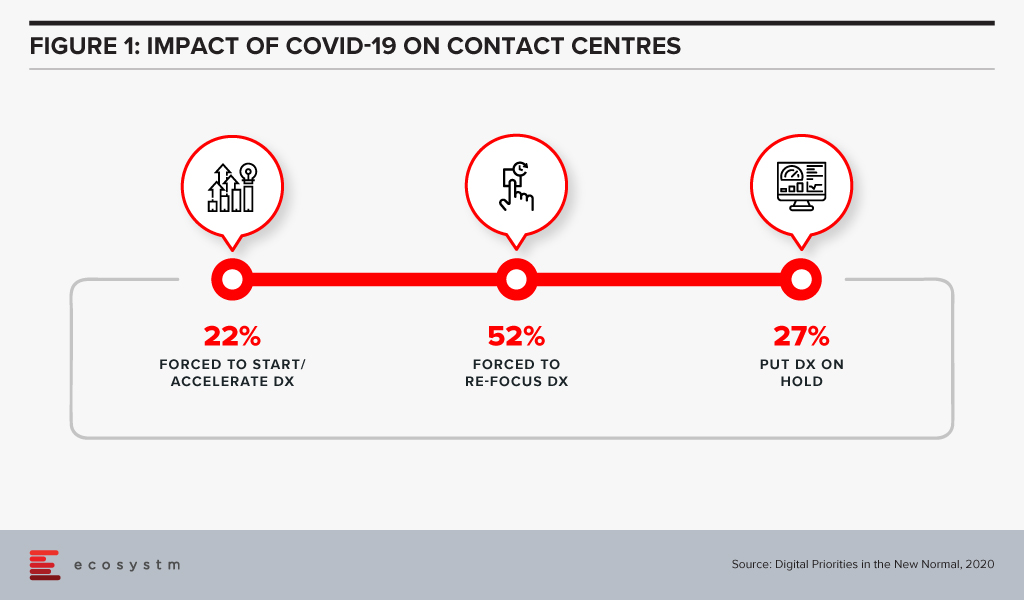

Running a contact centre has been extremely challenging in 2020. Contact centres have had to ensure business continuity, keep the focus on customer experience, and manage and motivate a largely remote workforce. Since the outbreak of COVID-19, not only have contact centres seen high inbound activity, but they have also had to manage agents who are dispersed and working remotely. 2020 has seen many contact centres starting, accelerating or re-focusing their digital transformation initiatives (Figure 1).

2021 will see contact centres focusing on transformation, not only to survive but also because their organisations and clients will expect more process efficiency and better customer experience. Ecosystm Advisors Audrey William and Ravi Bhogaraju present the top 5 Ecosystm predictions for Contact Centres Trends in 2021.

This is a summary of our predictions on the top 5 Contact Centre Trends for 2021 – the full report (including the implications) is available to download for free on the Ecosystm platform here.

The Top 5 Contact Centre Trends for 2021

- Remote Working Will Force Contact Centres to Re-evaluate Security Measures

Security has always been a concern for contact centre leaders. Improper data use by agents and agents breaching confidentiality are the biggest security challenges for contact centres. This has been further heightened, especially the fear of agents purposely breaching confidentiality while working from home.

Contact centres are still trying to figure out the best security measures when managing customer data, especially in the work-from-home environment. There is greater scrutiny over security and compliance measures – what agents view, how agents access the data, when agents log in and out of the system. Outsourcing providers will also have to guarantee high levels of security – a trusted relationship and defining the best practices on working from home will not be sufficient.

Many contact centres will trial different methods – from installing video surveillance cameras, desktop monitoring tools and access controls. Others will test technologies that can mask the information captured through mobile devices. This presents immense opportunities for vendors, as contact centres will rely heavily on technology to re-invent their security practices.

- Contact Centres will Invest in Conversational AI – Chatbots will No Longer be Enough

Many enterprises have rushed into deploying chatbots with expectations that these engines can solve the problem of high call volumes. The outcomes have often been poor, leaving customers frustrated and opting to interact with a live agent instead. Implementing a basic chatbot does not fully solve the problem and will force companies back to the drawing board.

Conversational AI offers a different experience by designing multiple forms of dialogues and conversations. It requires conversational design and the algorithms go through rigour from the start. The aim should be to make the channel irresistible – one that customers have confidence in, and that can reduce the need to email or call an agent. Successful uses cases have shown that conversational AI can reduce calls and repetitive queries by 70-90%. Ecosystm research finds that contact centres are ramping up their self-service capabilities and their adoption of AI and machine learning.

- Offshore Centres will Re-invent Themselves and Make a Comeback

2020 has seen contact centres in offshore locations struggle to offer services to global clients. Many of these operators have been plagued by poor internet connectivity at agents’ homes, and unfavourable home working environments. These outsourcing locations remain vital however, for multiple reasons – for example the range of services offered, agent specialisation, costs or diversity in agent profile.

Contact centre outsourcing providers will make a comeback in 2021 and we can expect new models to appear. Many providers across the globe have been running successful work-from-home only operations for years – other outsourcing providers will learn from these best practices. Organisations will find that bringing jobs back to high-cost locations will incur more costs. A full onshore model may not be the right model for business continuity, and organisations will prefer to have back-up locations to ensure continuity of services if another pandemic or catastrophe happens. Organisations will want to see the outsourcing providers offer them a choice of location – they will prefer some services to be delivered from offshore locations and others to remain onshore.

- Digital and Mobile will be the Cornerstone of Deeper Customer Engagement

COVID-19 has changed how customers want to be served, and organisations have had to re-evaluate how they use their channels – e.g. email, web, chat and voice. Customer profiles and expectations have changed over the year and they are more digital savvy and are more likely to interact with brands through digital and mobile apps. They will expect a single point of interaction – for their enquiries and to complete their transactions. For instance, they will expect to chat while filling up shopping carts. Introducing chat capabilities within mobile apps is a good way to impress customers – this can be an effective way to push promotions and upsell. Capabilities such as the ability to directly place a call from a website will make the customer experience exceptional. Customers will expect to move between channels easily when interacting with a brand.

- Workplace Collaboration Will be Fully Integrated into Contact Centres

Contact centres will reassess their business and talent models. The focus on employees will be in two major areas:

- Productivity. The contact centre floor dynamics have changed in how agents are spread out across outsourcing locations and in-house contact centres. Agents are no longer located in the same room or floor and do not have access to their usual way of work – continual training, digital signage that provides guidance and demonstrates KPIs, conversations with supervisors, managers, and team members for guidance or assistance, easy access to back-office functions and so on. This can impact their productivity.

- Engagement. Contact centre staff often work in high-stress environments -chasing sales targets and deadlines, handling complaints – and it is important for managers and supervisors to be able to engage and motivate them constantly. Remote working has further exacerbated the stress for those agents who do not have a conducive working environment at home.

Contact centres will increasingly look to workplace collaboration platforms and tools to improve employee productivity and experience.

Earlier this month, Telefónica Germany announced it will use Amazon Web Services (AWS) to virtualise its 5G core for a proof of concept (POC) in an industrial use case and plans to move to commercial deployment in 2021. Part of the POC process is to ensure compliance with all applicable data protection guidelines and certifying them according to relevant industry standards.

“With the virtualisation of our 5G core network, we are laying the foundation for the digital transformation of the German economy. This collaboration with AWS is an important part of our strategy for building industrial 5G networks”, said Markus Haas, CEO of Telefónica Germany.

Sentiment about cloud – especially public cloud – has been on a slight roller-coaster ride since they emerged back in the “noughties”: From initial reluctance to reluctant acceptance – to customer driven enthusiasm to scaling back and migrating back data and apps to on-premises data centres or private clouds to a more recent acceptance, that most enterprise resources may work best in a hybrid or public cloud environment.

Still, the viewpoint of many is still that core resources for the most part belong on-premises – especially if they are essential for the running of the business or involves sensitive data.

It is in this light that the Telefónica Germany announcement is interesting. On the face of it, it may appear that this is a possible major validation of public cloud as a platform for core systems and sensitive data. Although the core network components will remain on a different platform delivered by Ericsson, there is clearly an element of that.

Perception on Public Cloud

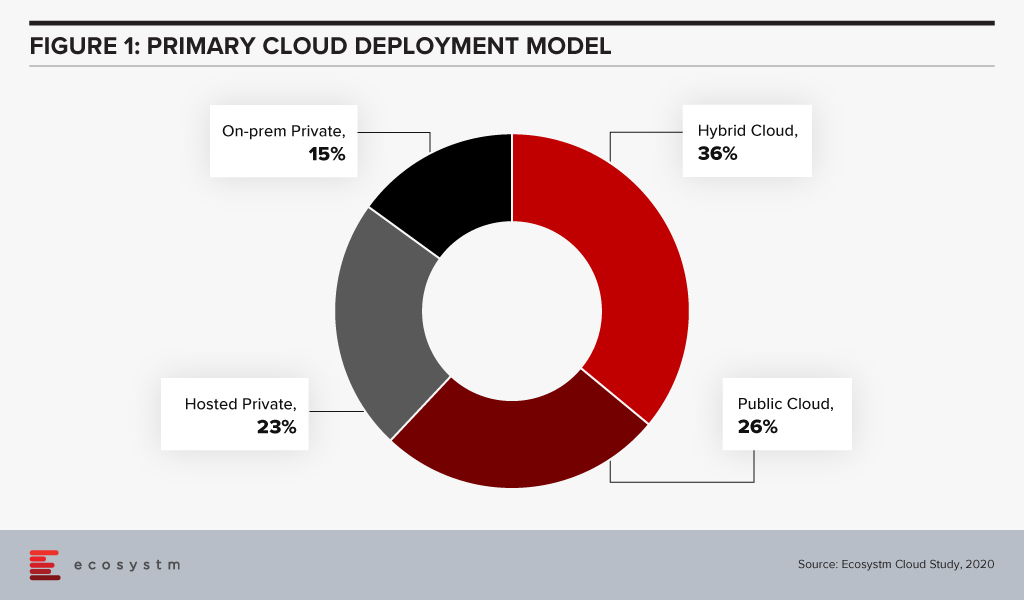

Many organisations remain sceptical with regards to public cloud. Ecosystm data shows that almost 40% have private cloud as their primary cloud deployment model (Figure 1); roughly a third have gone for a hybrid model and only around one quarter have chosen a public cloud model.

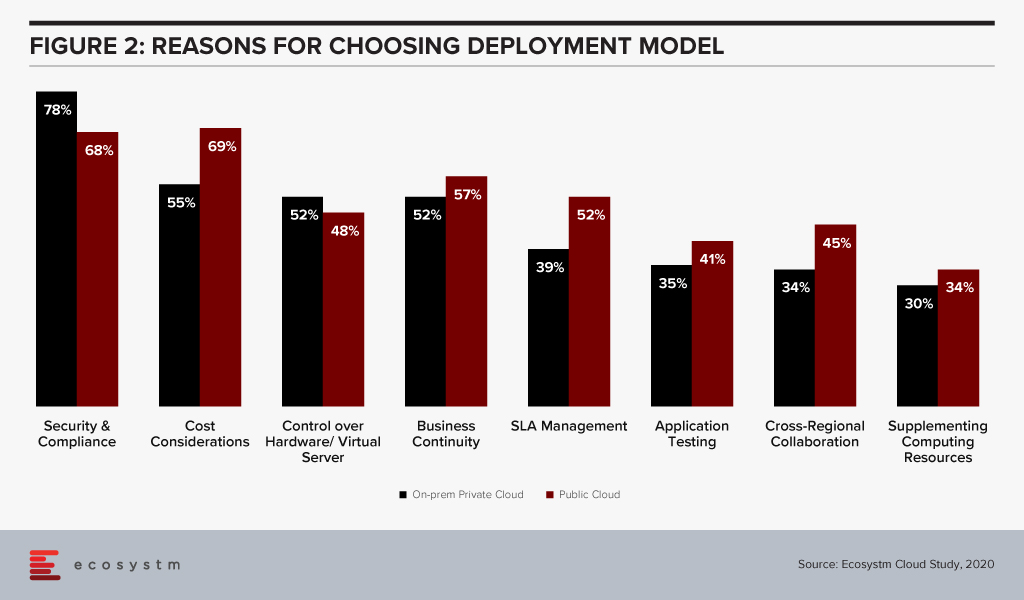

Most cloud deployment strategies ultimately come down to an evaluation of cost vs. risk and this evaluation is clearly demonstrated in Ecosystm data. Close to 80% of those choosing an on-premises private cloud model mention security and compliance as a main reason whereas cost considerations are the main reason for those opting for a public cloud model (Figure 2). What our data also shows is that public cloud providers are not necessarily winning the argument of cost savings among users.

For many organisations today, security and compliance concerns are still a valid point against public cloud as a primary deployment model. However, as we see more and more initiatives like Telefónica Germany, this argument diminishes – and it will become harder for IT organisations to convince senior management that this is still the way to go.

The Edge Complements the Cloud

The other noteworthy take-away from the Telefónica Germany initiative is how cloud-enabled edge computing is being embraced by the network design to ensure lower latencies for those who need it. The company states, “If companies use 5G network functions based on the cloud-based 5G core network of Telefónica Germany / O2 in the future, they will no longer need a physical core network infrastructure at their logistics and production sites, for example, but only a 5G radio network (RAN) with corresponding antennas.”

As I’m sure that you are an avid reader of Ecosystm Predicts every year, this should not come as a surprise as we wrote about something like this in the Top 5 Cloud Trends for 2020. Although some are touting Edge computing as the ultimate replacement of Cloud, we then believed – and still do – that it will be complimentary rather than competing technology. Cloud-based setups can benefit from pushing computing heavy workloads to the Edge in much the same way as IoT and provides a great platform for managing the Edge computing endpoints.

But to go back to the private cloud bit – while private cloud is not going away in the foreseeable future, we may be starting to see its demise in the more distant future.

To paraphrase a famous Brit: Now this is not the end. It is not even the beginning of the end. But it is, perhaps, the end of the beginning for private cloud.

Identifying emerging cloud computing trends can help you drive digital business decision making, vendor and technology platform selection and investment strategies.Gain access to more insights from the Ecosystm Cloud Study.

As the search for a COVID-19 vaccine intensifies, there is a global focus on the Life Sciences industry. The industry has been hit hard this year – having to deliver overtime through a disrupted supply chain, unexpected demand spikes, and reduction of revenues from their regular streams. Life sciences organisations are already challenged by the breadth of their focus – across R&D and clinical discovery; Manufacturing & Distribution; and Sales & Marketing. Increasingly, many pharmaceutical and medtech organisations choose to outsource some of these functions, which brings to fore the need for a robust compliance framework. In the Ecosystm Digital Priorities in the New Normal Study, two-thirds of life sciences organisations mention that they have either been forced to start, accelerate or refocus their Digital Transformation initiatives – the remaining one-third have put their Digital Transformation on hold. The industry is clearly at an inflection point.

Challenges of the Life Sciences Industry

Continued Focus on R&D. Life sciences companies operate in an extremely competitive global market where they have to work on new products against a backdrop of competition from generics and a global concern over rising healthcare expenditure. Apart from regulatory challenges, they also face immense competition from local manufacturers as they enter each new market.

Re-thinking their Distribution Strategy. Sales and distribution for many pharma and medtech organisations have been traditional – using agents, distributors, clinicians, and healthcare providers. But now they need to change their go-to-market strategies, target patients and consumers directly and package their product offerings into value-added services. This will require them to incorporate customer experience enhancers in their R&D, going beyond drug discovery and product innovation.

Tracking Global Regulations. Governments across the world are trying to manage their healthcare budgets. They are also more focused on chronic disease management. The focus has shifted to value-based medicine in general, but pharma and medtech products are being increasingly held accountable by health outcomes. Governments are increasingly implementing drug reforms around what clinicians can prescribe. Global Life Sciences organisations have to constantly monitor the regulations in the multiple countries where they operate and sell. They are also accountable for their entire supply chain, especially ensuring a high product quality and fraud prevention.

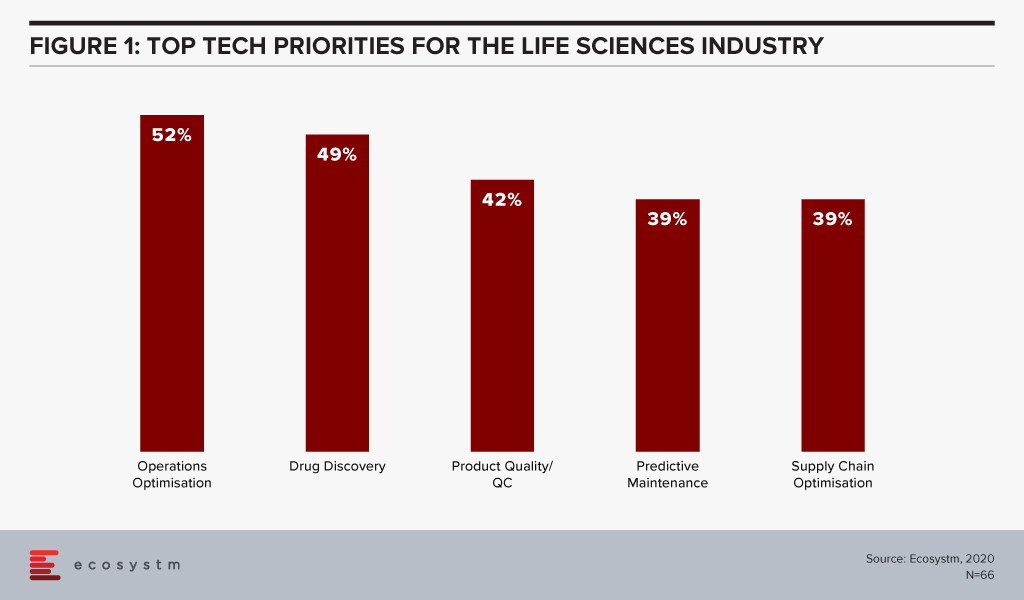

The global Ecosystm AI study reveals the top priorities for Life Sciences organisations, focused on adopting emerging technologies (Figure 1). They appear to be investing in emerging technology especially in their R&D and clinical discovery and Manufacturing functions.

Technology as an Enabler of Life Sciences Transformation

Discovery and Development

With the evolution of technology, Life Sciences organisations are able to automate much of the mundane tasks around drug discovery and apply AI and machine learning to transform their drug discovery and development process. They are increasingly leveraging their ecosystem of smaller pharma and medtech companies, research laboratories, academic institutions, and technology providers to make the process more time and cost efficient.

Using an AI algorithm, the researchers at the Massachusetts Institute of Technology have discovered an antibiotic compound that can kill many species of antibiotic-resistant bacteria. MIT’s algorithm screens millions of chemical compounds and chooses the antibiotics which have the potential to eliminate bacteria resistant to existing drugs. Harvard’s Wyss Institute for Biologically Inspired Engineering is manufacturing 3D printed organ-on-a-chip to give insights on cell, tissue, and organ biology to help the pharma sector with drug development, disease modelling and finally in the development of personalised medicine.

Life Sciences are also engaging more with technology partners – whether emerging start-ups or established players. Pfizer and Saama are working together on AI clinical data mining. The companies are developing and deploying an AI-based analytical tool where Pfizer provides clinical data and domain knowledge to train models on the Saama Life Science Analytics Cloud (LSAC). Saama was identified as a partner at a hackathon. Sanofi and Google have established a new virtual Innovation Lab to develop scientific and commercial solutions, using multiple Google capabilities from cloud computing to AI.

Tech providers also keep evolving their capabilities in the Life Sciences industry for more efficient drug discovery and better treatment protocols. Microsoft’s Project Hanover uses machine learning to develop a personalised drug protocol to manage acute myeloid leukaemia. Similarly, Apple’s ResearchKit – an open-source framework is meant to help researchers and developers create iOS-based applications in the field of medical research.

Manufacturing and Logistics

The industry also faces the challenges faced by any Manufacturing organisation and has the need to deploy manufacturing analytics, and advanced supply chain technology for better process and optimisation and agility. There is also the need for complete visibility over their supply chain and inventory for traceability, safety, and fraud prevention. Emerging technologies such as Blockchain will become increasingly relevant for real-time track and trace capability.

The MediLedger Network was established as an open network to the entire pharma supply chain. The project brings a consortium of some of the world’s largest pharmaceutical companies, and logistics providers to improve drug supply chain management.

Since the data on the distributed ledger is encrypted, it creates a secure system without any vulnerabilities. This eliminates counterfeit products and ultimately ensures the quality of the pharma products and promotes increased patient safety. To foster security and improve the supply chain, the United States Food and Drug Administration (USFDA) successfully completed a pilot with a group including IBM, KPMG, Merck and Walmart to support U.S. Drug Supply Chain Security Act (DSCSA) to trace vaccines and prescription medicines throughout the country.

Diagnostics and Personalised Healthcare

As more devices (consumer and enterprise) and applications enter the market, people will take ownership and interest in their own health outcomes. This is seeing a continued growth in online communities and comparison sites (on physicians, hospitals, and pharmaceutical products). Increasingly, insurance providers will use data from wearable devices for a more personalised approach; promoting and rewarding good health practices.

Beyond the use of wearables and health and wellness apps, we will also see an exponential increase of home-based healthcare products and services – whether for primary care and chronic disease management, or long-term and palliative care. As patients become more engaged with their care, the life sciences industry is beginning to serve them through personalised approach, medicines, right diagnosis and through advanced medical devices and products.

An online tool developed by the University of Virginia Health Systems helps identify patients that have a high risk of getting a stroke and helps them reduce that risk. This tool calculates the patient’s probability of suffering a stroke by measuring the severity of their metabolic syndrome – taking into account a number of conditions that include high blood pressure, abnormal cholesterol levels and excess body fat. Life Sciences organisations are increasingly having to invest in customer-focused solutions such as these.

Wearables with special smart software to monitor health parameters, gauge drug compatibility and monitor complications are being implemented by Life Sciences organisations. The US FDA approved a pill called Abilify MyCite fitted with a tiny ingestible sensor that communicates with a patch worn by the patient to transmit data on a smartphone. Medtech companies continue to develop FDA approved health devices that can monitor chronic conditions. Smart continuous glucose monitoring (CGM) and insulin pens send blood glucose level data to smartphone applications allowing the wearer to easily check their information and detect trends.

Technologies such as AR/VR are also enabling Life Sciences companies with their diagnostics. Regeneron Pharmaceuticals has created an AR/VR app called “In My Eyes” to better diagnose vision impairment in patients.

What is interesting about these personalised products is that not only do they improve clinical outcomes, they also give Life Sciences companies access to rich data that can be used for further product development and improvement.

The Life Sciences industry will continue to operate in an unpredictable and competitive market. This is evident by the several mergers and acquisitions that we witness in the industry. As they continue to use cutting-edge technology for their R&D practices, they will leverage technology to transform other functions as well.

Last week, the Australia government joined other countries in the Asia Pacific region in highlighting the growth of attack surface in the midst of the COVID-19 pandemic.

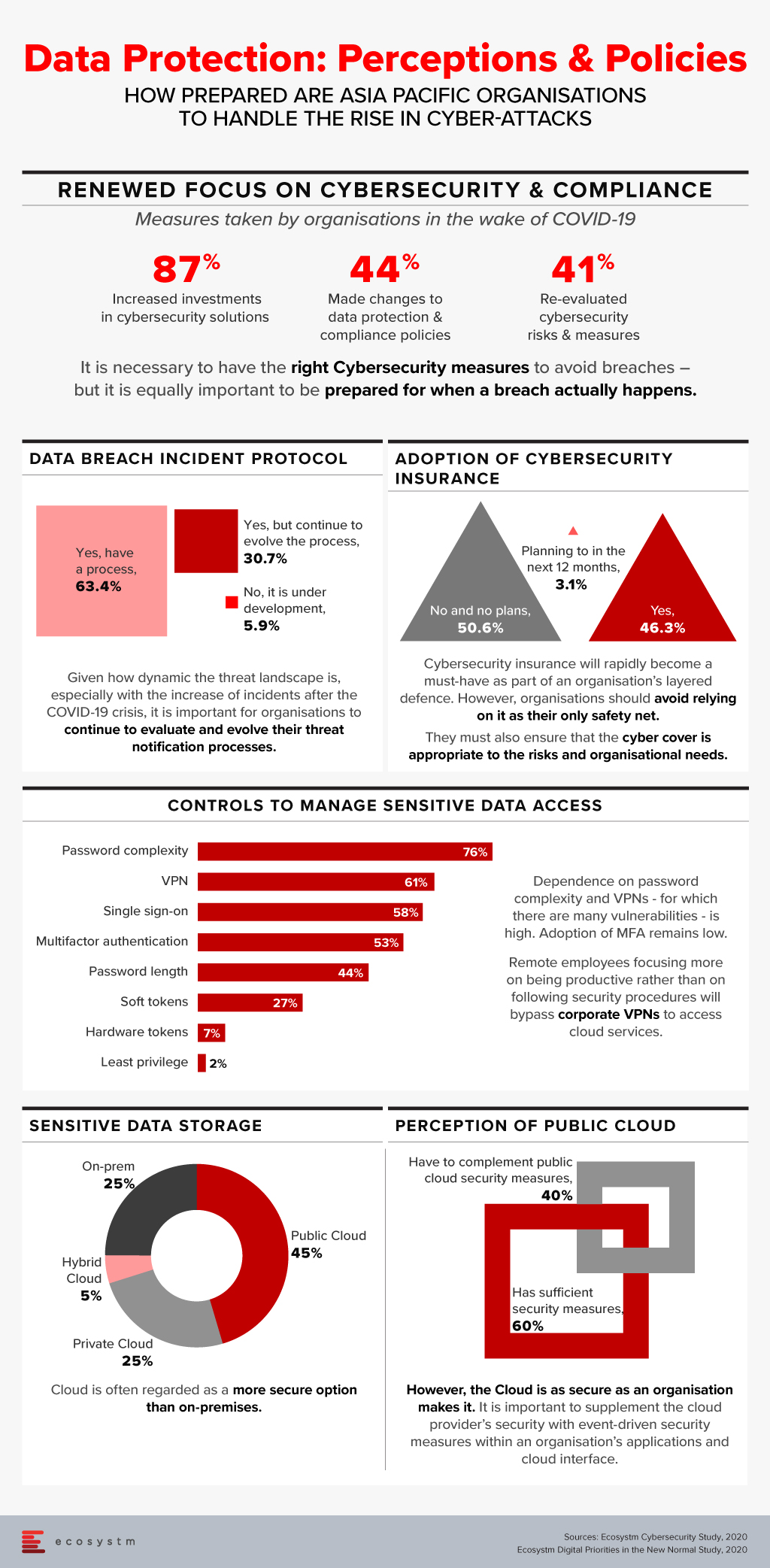

In our recently launched study Digital Priorities in the New Normal, we find that 87% of organisations in the Asia Pacific have increased investments in one or more cybersecurity solutions. However, this has to be backed by a reassessment of organisations’ risk positions and a re-evaluation of data protection and compliance policies.

There has been a widespread adoption of hybrid and multi-cloud architectures in the recent past and this trend is only expected to go up in the near future. A hybrid cloud adoption has its challenges though; including the need for organisations to baseline their security practices across so many different environments. Organisations that are aware of the cybersecurity risks associated are increasingly looking for external specialised help in managing their cloud security measures, especially with an aim to automate the processes.

Zscaler Acquires CloudNeeti

In a recent announcement, Zscaler announced its intentions to acquire Cloudneeti, a niche Cloud Security Posture Management (CSPM) start-up based in Redmond, Washington. This is set to expand Zscaler’s Cloud Security Platform capabilities to include data protection. With this acquisition, Zscaler will be able to complement its own offerings to provide:

- A complete Data Protection and Exposure Prevention suite, that works across locations, users and applications and ensures better compliance with regulations

- A Unified Compliance Assurance platform that provides compliance visibility and breach mitigation across the multiple SaaS applications an organisation uses

- Risk Reduction through automated remediations following both industry compliance laws and organisations’ own risk management program guidelines

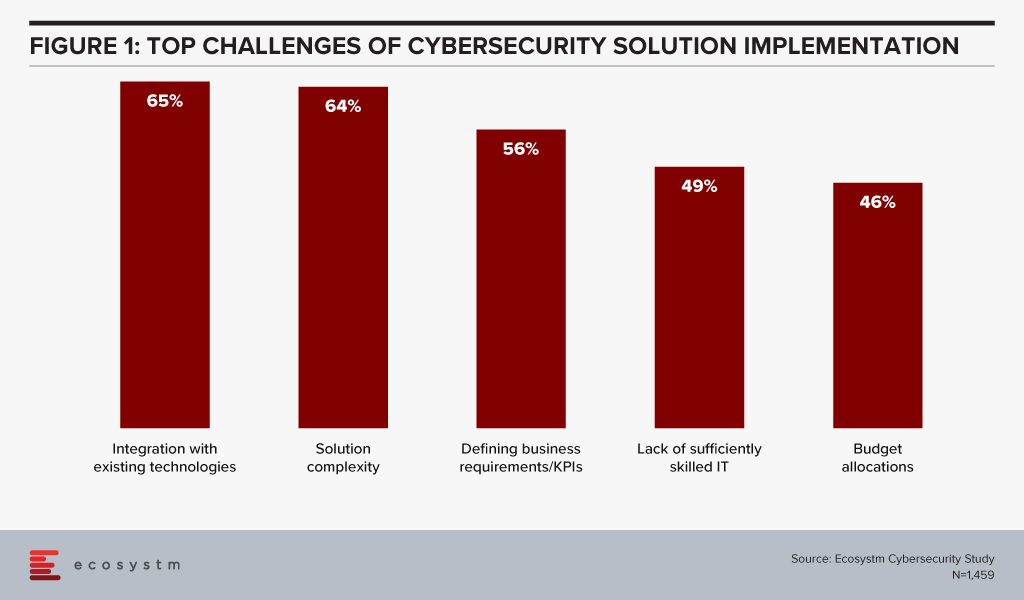

Ecosystm research finds that organisations are struggling with their cybersecurity implementations, especially as the solutions get increasingly complicated to combat the complex and evolving threat environment (Figure 1). Integration with existing cybersecurity measures, and a lack of sufficiently skilled IT staff to handle the myriad needs of the multiple systems and applications, builds a strong case for automation in cybersecurity practices.

Ecosystm Principal Advisor, Alex Woerndle says, “Automation is critical in cybersecurity, given the volume of data, alerts and incidents that are being dealt with on a daily basis, globally. Automating recurrent and high-volume tasks is a critical step in getting on top of this challenge.”

Importance of Automating Cybersecurity Processes

Woerndle sees a growing role for CSPM providers for multiple reasons. “Firstly, a lot of companies are finding that they cannot be ‘fully cloud’ and as such, end up with a complex architecture spanning on-premise, private cloud environments and multiple public cloud tenancies. Secondly, due to poorly planned cloud migrations, changing priorities, differences in service requirements, cost differences and also personal preferences across multiple teams, a lot of companies end up consuming different services across multiple public cloud providers (Azure, AWS, GCP, and so on). IT teams are struggling to be experts in all aspects of the shared responsibility model and with the capabilities to secure the various services. Finally, there is a constant stream of upgrades and addition of new services team members, given the easy accessibility public cloud environments provide. CSPM solutions provide the ability to establish baselines, enforce security controls and run regular checks to ensure compliance. Doing this manually is time consuming, expensive and always three steps behind.”

Woerndle also sees further complications because of the COVID-19 crisis. “COVID-19 has shifted the world to remote working overnight. Once workers are outside of the trusted corporate network and have access to cloud resources from their home networks, additional complexity to the corporate security posture is highlighted. Depending on how organisations have prepared for this, they either maintain control of all services and applications, and the access into each, or if not prepared, open direct access to a lot of unsecured applications from potentially very unsecured networks.” In fact Zscaler has seen its stock prices rising in the aftermath of the global crisis.

However, Woerndle warns, “While the conversation certainly supports the use of CSPMs, there is a lot more to it in terms of securing home networks, identity and access management, and so on.”

Zscaler’s acquisition of CloudNeeti certainly appears to be a timely move, in the current environment when organisations are struggling with a lack of resources with the extensive knowledge to understand all private and public cloud environments. There are controls required to secure each application, resource and system within an organisation – along with the time and effort required to implement, monitor, audit and improve cybersecurity measures over time.

Cybersecurity will remain an important topic of discussion on the world forum. 2020 is predicted to see an increasing number of state-sponsored cyber-attacks especially on utilities and public infrastructure. In addition, the number of AI based devices will increase which will receive specific attention from regulators for data and cybersecurity. Finally, there will be opportunities for mergers and acquisitions and investments in established cybersecurity providers to remain innovative and growing.

Here are the Top 5 Cybersecurity Trends for 2020, that we believe, will impact both businesses and consumers in 2020.

The Top 5 Cybersecurity Trends for 2020

The Top 5 Cybersecurity Trends for 2020 are drawn from the findings of the global Ecosystm Cybersecurity Study and is also based on qualitative research by Ecosystm Principal Advisors Alex Woerndle, Carl Woerndle and Claus Mortensen.

-

API Vulnerabilities will Become a Main Hacker Target

APIs grant access and provide transparency for developers – providing access and insights from both internal and external data. But they are inherently insecure. We have already seen several high-profile API breaches and announced API bugs. For example, in October 2018, Google had to shut down Google+ after an API bug exposed details for over 500,000 users.

We believe the problem will get significantly worse in 2020, with API attacks quickly becoming one of – if not the most – frequent target for hackers.

-

Operational Technology Security will Continue to Lag in 2020

Operational Technology (OT) refers to the hardware and software used to monitor and manage how devices that run on an organisation’s infrastructure perform. These devices have become smarter, remotely accessible and increasingly connected to networks. However, they were never designed with this in mind.

With organisations continuing to focus on data breaches – the investment in OT security will continue to lag. This will create a ‘security debt’ over coming years for those that do not invest in preventative controls now.

-

AI Training will Receive Attention from Regulators and the Public as a Possible Infringement of Privacy

News that Amazon’s Alexa was eavesdropping on its users, and that Apple’s Siri and Google’s Assistant, also kept recordings to help train their AI raised many concerns about how data to train AI is collected and stored. Apart from the initial consternation in the press and on social media, nothing much seems to have happened from a regulatory perspective.

2020 will be the year when AI training relying on consumer data will start to become regulated.

-

Major GDPR Fines in 2020 will Force MNCs to Invest in Security Compliance

GDPR came into effect in May 2018, but we still have not seen huge amounts of fines being issued in the EU. Only two fines were issued in 2018, while at least 17 were known to be issued in the first half of 2019, totalling about EUR 52 million. In the third quarter of 2019, at least 12 fines were issued totalling about EUR 328 million.

The trend is clear: Expect to see a magnitude of companies across EU be penalised in 2020. We also expect several fines above EUR 100 million and GDPR impacting countries outside the EU.

-

Mergers & Acquisitions will Ratchet up Significantly in 2020

The fragmented global security market consists of thousands of vendors and consultancies. Every day a swathe of new start-ups announces their ground-breaking new technology. Coupled with significant investments in tertiary education and industry certifications for a growing workforce, the next generation of cybersecurity entrepreneurs are entering with force.

We believe that this creates both threats and opportunities for established cybersecurity providers that need to remain innovative and growing. Similarly, this presents smaller or more niche cybersecurity start-ups with an avenue for funding or acquisition.

Ecosystm in partnership with SGInnovate, the government-backed organisation that promotes Deep Tech in Singapore, released a series of four reports covering areas of mutual interest: Cybersecurity, Artificial Intelligence, Cities of the Future and Healthtech. ‘Ecosystm Predicts: The Top 5 Cybersecurity Trends for 2020’ report is a part of this collaboration and is available for download from Ecosystm and SGInnovate websites.

Download Report: The top 5 Cybersecurity trends for 2020

The full findings and implications of the report ‘Ecosystm Predicts: The Top 5 Cybersecurity Trends for 2020’ are available for download from the Ecosystm platform. Signup for Free to download the report and gain insight into ‘the top 5 Cybersecurity trends for 2020’, implications for tech buyers, implications for tech vendors, insights, and more resources. Download Link Below ?