Two weeks ago, Michael Dell made the big announcement that Dell Technologies would spin off their shareholding in VMware, leading to a share price spike for both companies. A lot has already been written about the move – we would like to highlight a market-based view which we feel will be significant for the two companies going forward.

First let us break down the facts around the deal:

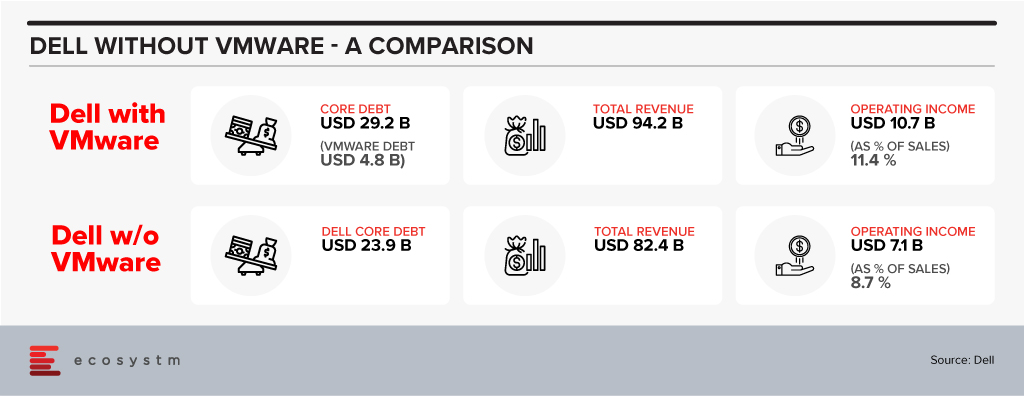

As has been analysed threadbare the deal reduces the total debt Dell is carrying and will even reduce the ratio of Dell debt to EBITDA. As a result, it is highly likely that Dell’s credit rating will move up from their current BB+ level to investment grade – which can have a lot of implications for future capital raising. There is also a buzz in the market that Dell Technologies may also sell off Boomi soon and write down another USD 3 Billion approximately in debt.

It is interesting to note that the company has been willing to let go off VMware even though it will dilute their profitability ratios – VMWare business being obviously more profitable than Dell’s traditional businesses which are heavily based on products.

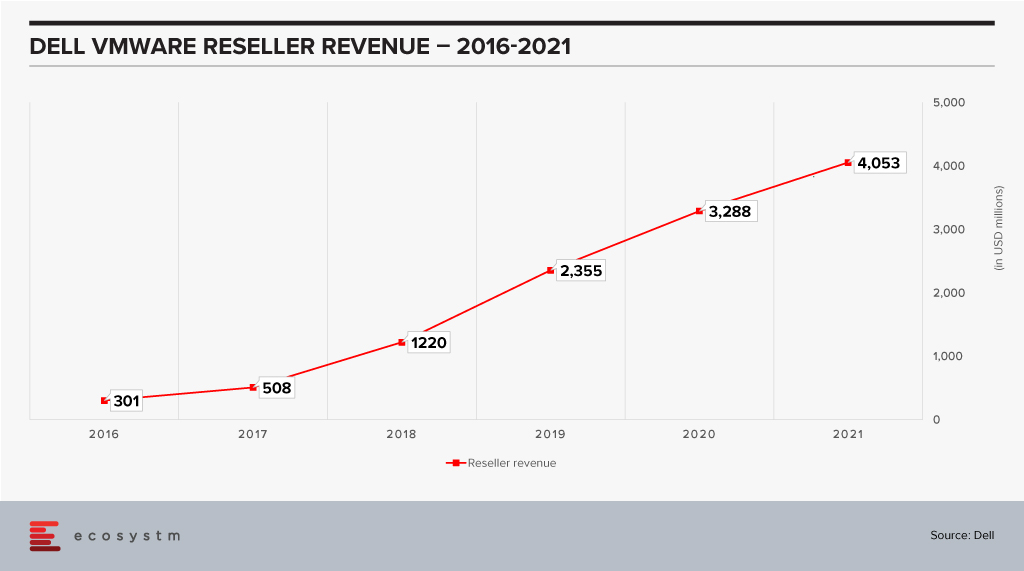

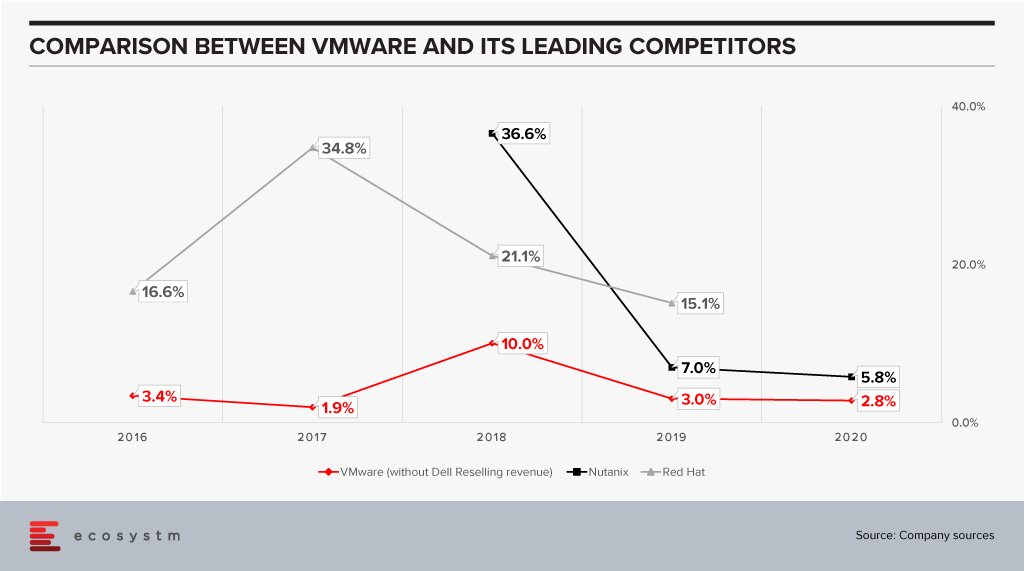

The last few years has seen Dell reselling a fair amount of VMware products. From a number of perspectives Dell has been a key reseller for VMware and now contributes almost 34% of VMware’s revenues.

This chart is a testament to the power of execution that is inherent within Dell. This performance was aided by market growth – but even then it is remarkable how Dell has been able to scale up taking VMware to their customers. The two companies have very different sales cycles. A VMware sale typically has a longer cycle with a completely different set of touchpoints from the boxes that Dell is so good at selling – which have shorter cycles. The sales cycle for EMC products is closer to VMware’s which would have helped. The sales of the VXRail hyperconverged appliance have also jumped in recent times and this would have driven an equivalent spike in VMware revenues. It is still a remarkable achievement to be able to bring these three diverse groups together and grow revenue.

Market Impact of the Spin-Off

Does it make sense then for VMware to part with their largest reseller? Would it not be better for VMware to continue to drive this and use Dell’s execution skills to drive more growth? Data suggests that there could be another twist to this story.

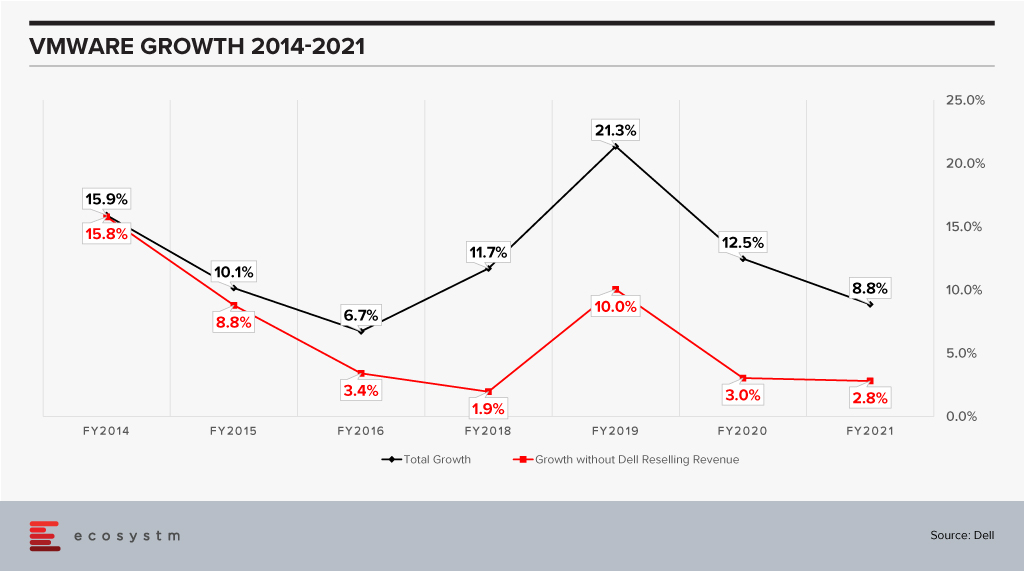

VMware has been growing impressively as a company when one looks at the black line and while the growth has slowed in percentage terms, this is on a much higher revenue base. FY2021 revenue is close to 2x the revenue in FY2014. However, when one considers it without the Dell reselling revenue (the red line) it looks a lot less impressive especially in the last couple of years when it is an anemic 3%. When comparing this growth we also see a slowdown of sorts in recent years for VMware.

Til Dell acquired EMC – and VMware in consequence – they were working closely with other vendors such as Nutanix and driving solid growth for them. As they pivoted to doing more with VMware, did this then mean that other vendors – of either bare metal or cloud – drifted away from VMware?

Anecdotal evidence suggests that vendors such as HPE became more cautious and tried to diversify their business. It is entirely possible that if we looked at VMware as two separate businesses – one with Dell and one independent – the independent business has been losing share in the last few years.

The optical separation from Dell may then help VMware in rebuilding stronger relationships with the other players in the market including the hyperscalers. This may fuel further VMware growth. To do that VMware will have to manage a balancing act:

- On the one hand keep growing their reseller revenue with Dell. They are on a good wicket so far and need to make sure this continues. While the revenue from appliances – which come loaded with VMware – is a sure-fire proposition, other growth needs to be harvested carefully. Dell has a multitude of offerings and taking their eyes of the VMware ball is super easy.

- Build trust and closer ties with the other vendors to keep driving revenue. VMware’s leadership in the market means they already have ties with other industry leaders like HPE, AWS and so on. These will need to become much deeper; VMware will need to build the trust that they will give these vendors equal status even as they are building new appliances with Dell.

The one complicating factor here is that Michael Dell remains the Chairman of the Board of VMware. This may give other vendors pause and they may still want to keep their options open instead of putting all eggs into the VMware basket.

Ecosystm Comments

VMware is at a fairly critical inflection point in their business. The growth of cloud technologies still bodes well for virtual machines which has been their mainstay, but this is also likely to drive growth for more containerisation. They have great products for that part of the business also. However, as container adoption is likely to explode VMware would not want vendors to shift, to say Red Hat, and develop deeper partnerships with them or other competitors. They would like to keep the vendors on VMware – be it a virtual machine or a container. One does feel the future battle for VMware really rests on how well they will be able to grow in the container space. This will have to be done while continuing to innovate to keep the lead in the virtual machine space. Doing it will be quite a feat!!

Finally, what then of Dell? The company seems to have a talent for running businesses which are in long-term secular decline – but running those businesses well. Their PC business is delivering almost 7% operating income and has continued to show growth. The PC market last year was on fire thanks to the pandemic which dramatically increased the demand for devices – growth was double digits for a market which has declined almost every year since 2011. As Dell is fond of saying the PC industry has sold over 5 billion machines since the PC was declared dead!

The server market seems to have stagnated over the last couple of years which is a bit of a surprise given the growth in cloud. Dell’s revenue has declined two years in a row pointing to possible issues which need fixing in that part of the business.

As the company focuses on these key challenges in the market it probably makes sense for them to lower their debt and earn more freedom to operate. One never knows – given the number of surprises that Michael Dell has engineered over the last decade such as taking Dell private, acquiring EMC, stabilising it, then going public again, making a windfall in the process – if he has some other rabbits yet to be pulled out of his hat!!!

Access insights on adoption of key Cloud solutions in regions/countries and industries. Insights include drivers and inhibitors of adoption, budget allocation, and preferred implementation partners.

Nutanix has emerged as a leading hyper converged infrastructure (HCI) provider and is partnering with public cloud infrastructure providers to bring greater value to its customers. Last week saw the partnership between Microsoft and Nutanix, aimed to evolve the hybrid offerings of both providers. As part of this collaboration, both companies will focus on extending Nutanix hybrid cloud infrastructure to Azure. The collaboration will include the development of Nutanix-ready nodes on Azure to support Nutanix Clusters and services. The benefits expected include improved cost, security, and efficiency. Clients will also be able to deploy Azure instances from Nutanix interface for a consistent experience across their cloud environment. The solution is aimed to eliminate re-tooling, re-architecting processes and other technical challenges of maintaining a hybrid environment.

Ecosystm Principal Advisor, Darian Bird says, “The announcement of Nutanix Clusters on Azure is another piece of the hybrid puzzle that will allow Nutanix clients to extend their private cloud environments into public infrastructure. Organisations want the control associated with a private cloud but with the flexibility to scale up and down in the public cloud. Key to hybrid cloud is an additional layer that enables applications to be shifted from one cloud to another, either to prevent lock-in or to choose the best environment depending on the circumstances.”

The deal will also broaden the sales and support experience for Microsoft and Nutanix. “Nutanix has emphasised licence portability as a key characteristic of its hybrid cloud strategy. Microsoft clients will be able to use Azure credits to pay for Nutanix software, while those already with Nutanix licences will be able to port those over to Clusters on Azure. Simplified cloud procurement will be critical for IT departments looking to optimise cloud expenditure across multiple providers.”

Bird adds, “Organisations will now be able to manage servers, containers, and data services on Nutanix HCI, on prem or in the cloud through a single control pane with Azure Arc. Microsoft has realised that producing a true hybrid cloud system requires it to manage as many types of infrastructure as possible, whether they come from niche partners or major competitors. IT departments want the choice of supplier without adding complexity to their systems.”

Nutanix Strengthening its Partner Ecosystem

“The partnership with Microsoft Azure comes only a month after Nutanix announced the general availability of Clusters on AWS. Considering Nutanix’s close connection to Google, it seems likely that it will also launch on the search giant’s cloud before long,” says Bird.

Last year, Nutanix partnered with HPE for the general availability of HPE’s integrated hybrid cloud as a service offering, HPE GreenLake for Nutanix, and the HPE ProLiant DX solution.

Earlier in the month, Nutanix launched its global partner multi-cloud program – Elevate – to bring Nutanix’s global partner ecosystem under one integrated architecture managed through consistent tools, resources and platforms, to accelerate their clients’ multi-product, multicloud roadmap in their transformation journeys.

“Nutanix has made great strides in its shift from hardware vendor to HCI provider and it’s now focused on delivering tools that enable the shift to cloud. These recent moves will help Nutanix catch up to VMware and become a viable alternative in a hybrid cloud environment,” says Bird.

We have all felt the effects of the global pandemic and experienced the profound effects on the way we work – at least those of us who are fortunate enough to still be working despite the pandemic.

COVID-19 has – at least for a while – changed how we work and how IT systems can safely support this new work style.

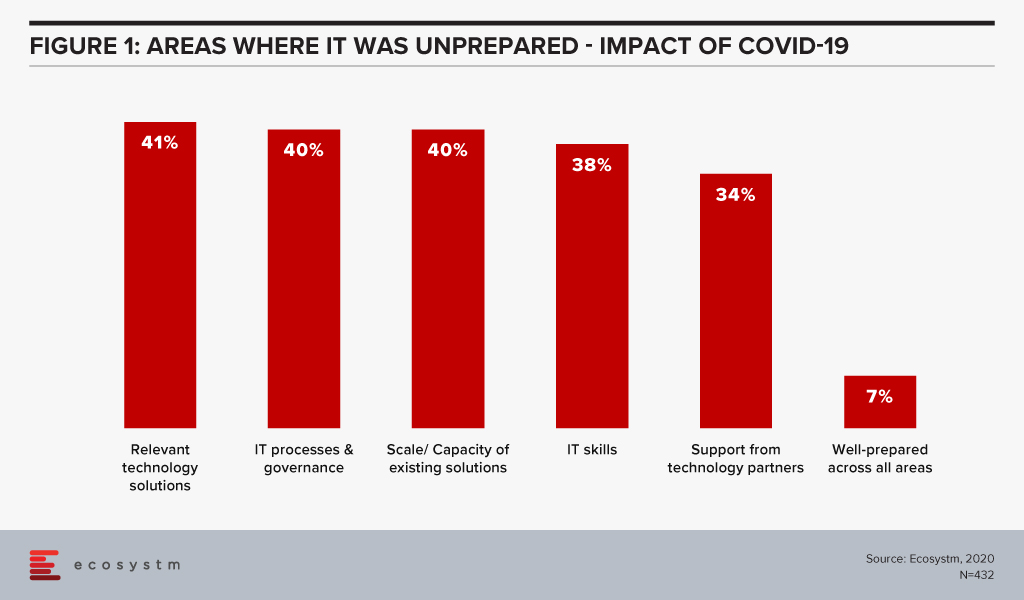

Our ongoing Ecosystm study on Digital Priorities in the New Normal shows how the crisis has forced organisations to re-evaluate their cybersecurity risks and measures. It also showed that the IT environment of most organisations was woefully unprepared for the changes that occurred (Figure 1). Perhaps unsurprisingly, fewer than 7% said that their IT environment was fully prepared and close to 40% reported lacking scale, capacity and IT skills in-house.

We are here to help you!

The combination of these shortcomings may very well push more organisations to outsource their security management to Managed Security Service Providers (MSSPs) – a service space that has been growing rapidly in recent years.

Many IT organisations are fairly familiar with MSSPs, but COVID-19 may have forced many to re-evaluate their choices as the work and threat landscapes have changed.

To help organisations evaluate their options going forward, we at Ecosystm are extremely excited to launch our Managed Security Service Providers VendorScope for the Asia Pacific region.

This new tool can help technology buyers understand which vendors are leading this space, which are the ones that have market momentum and which are executing and delivering on their promised capabilities. Unlike similar vendor evaluations on the market, the positioning of vendors in Ecosystm VendorScopes is based solely on quantifiable feedback given by the Tech Buyer community, in the global Ecosystm Cybersecurity Study, that is live and ongoing on the Ecosystm platform. It is thus independent of analyst bias or opinion or vendor influence – customers directly rate their suppliers in our ongoing market benchmarks and assessments.

It is also free to access and share for all Ecosystm subscribers!

Fragmented Asia Pacific MSSP Market

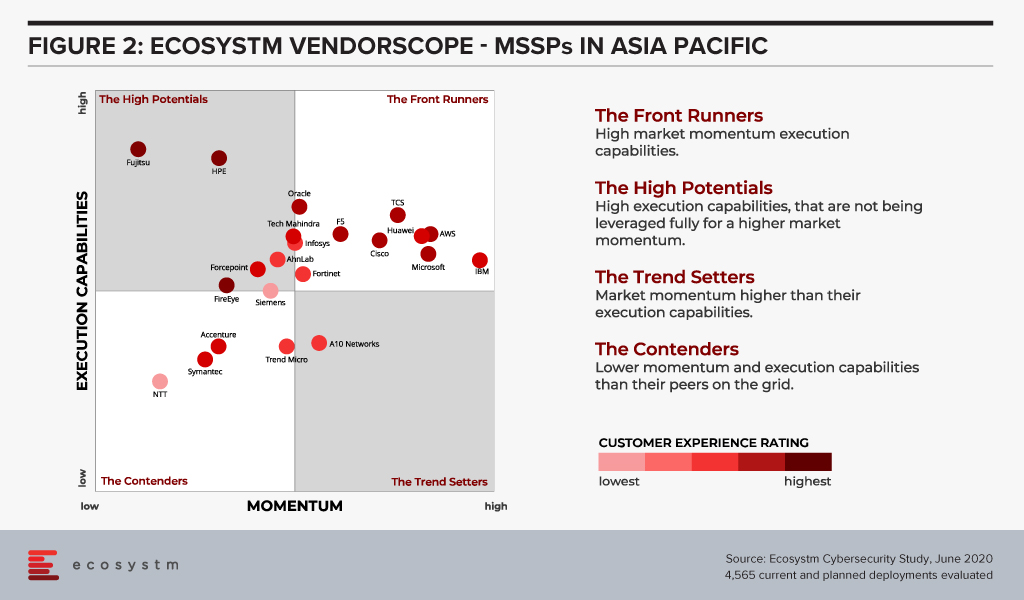

The VendorScope clearly shows how fragmented the MSSP market is. Not only is the number of vendors that have a customer base significant enough to appear on the grid very large (22) – but about half of them are in, or verging on being in, the “Front Runner” segment (Figure 2).

There are a few key factors that contribute to this picture:

- The services they offer tend to align well with the customers’ organisational strategies and to integrate well with existing systems. This, basically, can be boiled down to one word: Cloud. Most organisations have IT strategies revolving around multiple and/hybrid cloud deployments and using MSSPs makes a lot of sense.

- Momentum for this service segment is generally high. The MSSP space is experiencing high growth these days and we see a fairly high number of mentions for both current and planned deployments with many of the vendors in the study.

Despite the large number of vendors in the “Front Runner” segment, a famous few stick out. IBM appears to have a higher market momentum than its competitors and together with Microsoft, they have the largest share of mind with potential customers in this space.

But other vendors are hot on their heels. AWS and F5 stand out with their relatively high presence in the region, and TCS and Huawei appear to have stronger than average pipelines.

Where we do see weak spots with most vendors is in quality of service and the connected customer experience, which historically have proven to be a potential Achilles’ heel for many vendors in high growth areas. As the MSSP space matures, we would expect customer experience to become increasingly important when customers choose a service provider.

We would certainly encourage any organisation that is looking into managed security to not ignore or downplay the customer service and support aspect. IT security is a complex area – even if it is managed by a service provider – and the service providers’ ability and flexibility in this area can make a huge difference.

Fujitsu and HPE stick out with regards to QoS and customer service. These two are also good examples of how the vendors differ and seemingly could complement each other. In a sense, one could almost see the MSSP VendorScope as an early blueprint for which mergers and acquisitions (M&As) would make sense – at least for those that are driven by the pursuit of skill sets and competencies and not just market share.

In the Top 5 Cybersecurity and Compliance Trends for 2020, Ecosystm predicted that 2020 will witness a significant uplift in M&A activities in the cybersecurity market. Of course, with the global pandemic, all bets are off, and the predicted M&A wave may have been delayed by a year or so.

But the MSSP space certainly appears ripe for consolidation.

Ecosystm Vendorscope: Managed Security Service Providers

Signup for Free to download the Ecosystm Vendorscope: Managed Security Service Providers report

Thriving in the New Normal – Overcoming Our Challenges Together

In this webinar, we will discuss how we can help you and your organisation during these difficult times. To keep your business running, remote workplace solutions have become essential. We want to share capabilities on how to stay connected—and stay secure—while we work remotely.

In The Top 5 Cloud trends for 2020, Ecosystm Principal Analyst, Claus Mortensen had predicted that in 2020, cloud and IoT will drive edge computing.

“Edge computing has been widely touted as a necessary component of a viable 5G setup, as it offers a more cost-effective and lower latency option than a traditional infrastructure. Also, with IoT being a major part of the business case behind 5G, the number of connected devices and endpoints is set to explode in the coming years, potentially overloading an infrastructure based fully on centralised data centres for processing the data,” says Mortensen.

Although some are positioning the Edge as the ultimate replacement of cloud, Mortensen believes it will be a complementary rather than a competing technology. “The more embedded major cloud providers like AWS and Microsoft can become with 5G providers, the better they can service customers, who want to access cloud resources via the mobile networks. This is especially compelling for customers who need very low latency access.”

Affirmed Networks Brings Microsoft to the 5G Infrastructure Table

Microsoft recently announced that they were in discussions to acquire Affirmed Networks, a provider of network functions virtualisation (NFV) software for telecom operators. The company’s existing enterprise customer base is impressive with over 100 major telecom customers including big names such as AT&T, Orange and Vodafone. Affirmed Networks’ recently appointed CEO, Anand Krishnamurthy says that their virtualised cloud-native network, Evolved Packet Core, allows for scale on demand with a range of automation capabilities, at 70% of the cost of traditional networks. The telecom industry has been steadily moving away from proprietary hardware-based infrastructure, opting for open, software-defined networking (SDN). This acquisition will potentially allow Microsoft to leverage their Azure platform for 5G infrastructure and for cloud-based edge computing applications.

Ecosystm Principal Advisor, Shamir Amanullah says, “The telecommunications industry is suffering from a decline in traditional services leading to a concerted effort in reducing costs and introducing new digital services. To do this in preparation for 5G, carriers are working towards transforming their operations and business support systems to a more virtualised and software-defined infrastructure. 5G will be dynamic, more than ever before, for a number of reasons. 5G will operate across a range of frequencies and bands, with significantly more devices and connections, highly software-defined with computing power at the Edge.”

Microsoft is by no means the only tech giant that is exploring this space. Google recently announced a new solution, Anthos for Telecom and a new service called the Global Mobile Edge Cloud (GMEC), aimed at giving telecom providers compute power on the Edge. At about the same time, HPE announced a new portfolio of as-a-service offering to help telecom companies build and deploy open 5G networks. Late last year, AWS had launched AWS Wavelength that promises to bring compute and storage services at the edge of telecom providers’ 5G networks. Microsoft’s acquisition of Affirmed Networks brings them to the 5G infrastructure table.

Microsoft Continues to Focus on 5G Offerings

The acquisition of Affirmed Networks is not the only Microsoft initiative to improve their 5G offerings. Last week also saw Microsoft announce Azure Edge Zones aimed at reducing latency for both public and private networks. AT&T is a good example of how public carriers will use the Azure Edge Zones. As part of the ongoing partnership with Microsoft, AT&T has already launched a Dallas Edge Zone, with another one planned for Los Angeles, later in the year. Microsoft also intends to offer the Azure Edge Zones, independent of carriers in denser areas. They also launched Azure Private Edge Zones for private enterprise networks suitable for delivering ultra low latency performance for IoT devices.

5G will remain a key area of focus for cloud and software giants. Amanullah sees this trend as a challenge to infrastructure providers such as Huawei, Ericsson and Nokia. “History has shown how these larger software providers can be fast, nimble, innovative, and extremely customer-centric. Current infrastructure providers should not take this challenge lightly.”

Data Management and Digital Transformation: Inextricably Intertwined

Digital transformation (DX) is at the top of the strategic objectives list for most organisations. However, one key aspect of DX that is often overlooked and causes problems if not adequately prepared for, is the issue of data management. Before you can reap the benefits of your data – which is the core of DX – you need to have control over it first.

Most enterprise data is scattered across multiple locations on-premise and in various clouds (public, private, hybrid). It is trapped in infrastructure silos or buried in long-forgotten storage systems, or back-up devices. This makes it difficult and time-consuming for IT to control or access and hinders data exploitation for the business.

The topic of data management, although not as exciting sounding as DX, or analytics, is substantially more critical to business success, so I invite you to join Ecosystm, HPE, Cohesity, and PTC at our Executive Luncheon on “Data Management & Digital Transformation: Inextricably Intertwined”. In a collegiate and sharing environment, we will discuss how you can take back control of your data and simplify the way your company protects, controls and extracts value from your data across all sources.

This session is designed to share and learn with your peers and industry experts on some of the following topics:

- Relevance and importance of Data Management to your Digital Transformation initiatives and enabling your business to derive competitive advantage from all of your data

- Discussion on the key issues around data management including data collection, storage, coping with growth, data protection and privacy, and management and use of data from the center to the edge

- Best practices in data management – based on a short interactive roundtable discussion format where you workshop one of a selection of data management challenges as a table and exchange ideas and solutions

Fuelling innovation in a hyper converged world

The incredible pace of innovation is demanding speed and agility from IT to introduce new services in a secure and trusted manner. These demands are coming from different business functions who are all looking at the IT team to enable their business processes. IT needs to provide them the flexibility to pilot, fail, grow and prioritise these new capabilities in a rapid manner.

Hyperconvergence provides the agility and economics of cloud with the enterprise’s capabilities of the on-demand infrastructure.

EVERYTHING AS A SERVICE –

Accelerating Innovation through the Democratisation of Infrastructure & Applications

We are in a consumption economy as customers move towards paying as they use a product rather than owning it themselves. How can IT teams support businesses in transitioning to this new business model?

More importantly, how can IT leverage this model to deliver speed, agility and innovation to the business?

How do you get the full benefits of a scalable model and continue to have the full control over security, data privacy and

regulatory requirements? Specifically, we will discuss four major themes as companies transition to this model.

- Hybrid IT models

- Managing privacy and security

- Migration strategies

- Changing the cost dynamics

HPE’s announcement in Madrid regarding its build out of Edge Computing services and solutions is to be expected as more of its customers and prospects look to establish comprehensive data and systems management functions at the edge of the IT network. As more data is created outside of the traditional data centre walls, IT needs to be able to provide the same level of integrity for the remote locations. HPE’s announcement of the Edgeline systems management fills that gap. However, this does signal to CIOs and lines of businesses that they will now have to continue this build out of full remote distributed IT services to include data backup, recovery, application device management, etc :- expect HPE to continue to make future announcements to meet those needs. Industrial partners such as industrial players like PTC will benefit from this announcement as it will enable their products to run in a more enterprise-class environment.

HPE’s announcement to provide an open link platform between industrial and IT connectivity protocols is again a reflection of a maturing IoT market. As businesses move from proof of concept into production, more varied input sources from differing factory floor devices could or should be connected. The open link platform is a way to encourage and speed up that connectivity.

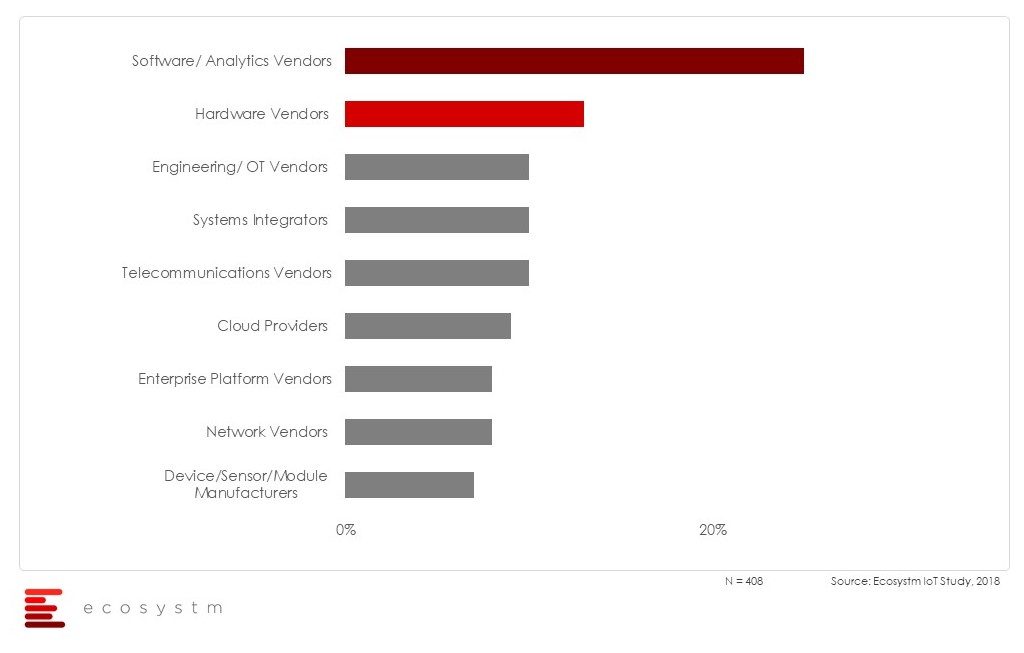

However, our IoT study data indicates that enterprises who are adopting large scale IOT projects prefer to work with software and analytics vendors, rather than pure-play hardware vendors. Today’s announcement is a way for HPE to demonstrate to its customers and prospects that it is more than an ‘edge server’ hardware company, but that it can provide full systems management services. Its biggest competitor in this field, DELL EMC will argue that it too can provide these services across its company portfolio.

Figure: Primary Partners for Current IoT Projects

Finally: our advice to tech buyers is that those who want to build out an edge infrastructure will need to plan to support a fully integrated data and systems management environment and therefore look to a vendor who can replicate their enterprise solutions and support capabilities. This may be in contrast to their distributed cloud computing strategy which HPE have not articulated but will need to over time.