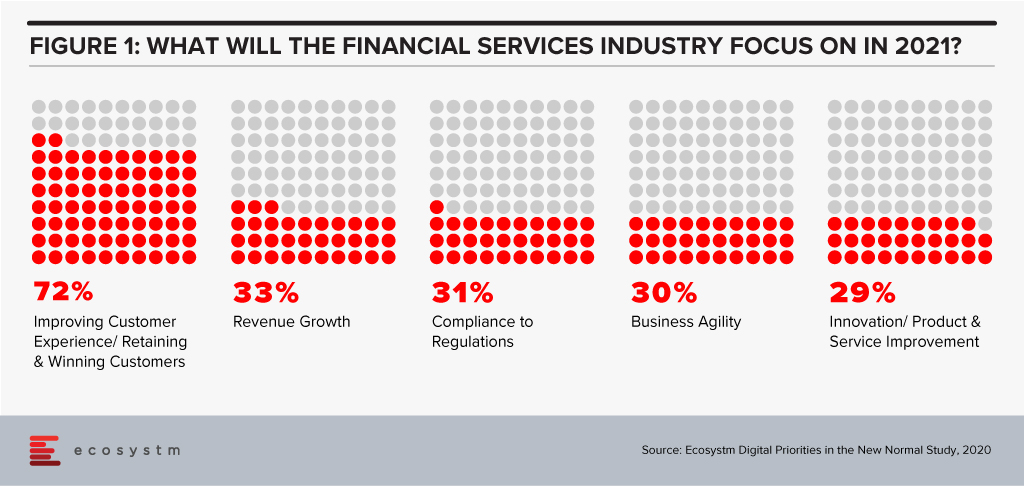

The disruption that we faced in 2020 has created a new appetite for adoption of technology and digital in a shorter period. Crises often present opportunities – and the FinTech and Financial Services industries benefitted from the high adoption of digital financial services and eCommerce. In 2021, there will be several drivers to the transformation of the Financial Services industry – the rise of the gig economy will give access to a larger talent pool; the challenges of government aid disbursement will be mitigated through tech adoption; compliance will come sharply back into focus after a year of ad-hoc technology deployments; and social and environmental awareness will create a greater appetite for green financing. However, the overarching driver will be the heightened focus on the individual consumer (Figure 1).

2021 will finally see consumers at the core of the digital financial ecosystem.

Ecosystm Advisors Dr. Alea Fairchild, Amit Gupta and Dheeraj Chowdhry present the top 5 Ecosystm predictions for FinTech in 2021 – written in collaboration with the Singapore FinTech Festival. This is a summary of the predictions; the full report (including the implications) is available to download for free on the Ecosystm platform.

The Top 5 FinTech Trends for 2021

#1 The New Decade of the ‘Empowered’ Consumer Will Propel Green Finance and Sustainability Considerations Beyond Regulators and Corporates

We have seen multiple countries set regulations and implement Emissions Trading Systems (ETS) and 2021 will see Environmental, Social and Governance (ESG) considerations growing in importance in the investment decisions for asset managers and hedge funds. Efforts for ESG standards for risk measurement will benefit and support that effort.

The primary driver will not only be regulatory frameworks – rather it will be further propelled by consumer preferences. The increased interest in climate change, sustainable business investments and ESG metrics will be an integral part of the reaction of the society to assist in the global transition to a greener and more humane economy in the post-COVID era. Individuals and consumers will demand FinTech solutions that empower them to be more environmentally and socially responsible. The performance of companies on their ESG ratings will become a key consideration for consumers making investment decisions. We will see corporate focus on ESG become a mainstay as a result – driven by regulatory frameworks and the consumer’s desire to place significant important on ESG as an investment criterion.

#2 Consumers Will Truly Be ‘Front and Centre’ in Reshaping the Financial Services Digital Ecosystems

Consumers will also shape the market because of the way they exercise their choices when it comes to transactional finance. They will opt for more discrete solutions – like microfinance, micro-insurances, multiple digital wallets and so on. Even long-standing customers will no longer be completely loyal to their main financial institutions. This will in effect take away traditional business from established financial institutions. Digital transformation will need to go beyond just a digital Customer Experience and will go hand-in-hand with digital offerings driven by consumer choice.

As a result, we will see the emergence of stronger digital ecosystems and partnerships between traditional financial institutions and like-minded FinTechs. As an example, platforms such as the API Exchange (APIX) will get a significant boost and play a crucial role in this emerging collaborative ecosystem. APIX was launched by AFIN, a non-profit organisation established in 2018 by the ASEAN Bankers Association (ABA), International Finance Corporation (IFC), a member of the World Bank Group, and the Monetary Authority of Singapore (MAS). Such platforms will create a level playing field across all tiers of the Financial Services innovation ecosystem by allowing industry participants to Discover, Design and rapidly Deploy innovative digital solutions and offerings.

#3 APIfication of Banking Will Become Mainstream

2020 was the year when banks accepted FinTechs into their product and services offerings – 2021 will see FinTech more established and their technology offerings becoming more sophisticated and consumer-led. These cutting-edge apps will have financial institutions seeking to establish partnerships with them, licensing their technologies and leveraging them to benefit and expand their customer base. This is already being called the “APIficiation” of banking. There will be more emphasis on the partnerships with regulated licensed banking entities in 2021, to gain access to the underlying financial products and services for a seamless customer experience.

This will see the growth of financial institutions’ dependence on third-party developers that have access to – and knowledge of – the financial institutions’ business models and data. But this also gives them an opportunity to leverage the existent Fintech innovations especially for enhanced customer engagement capabilities (Prediction #2).

#4 AI & Automation Will Proliferate in Back-Office Operations

From quicker loan origination to heightened surveillance against fraud and money laundering, financial institutions will push their focus on back-office automation using machine learning, AI and RPA tools (Figure 3). This is not only to improve efficiency and lower risks, but to further enhance the customer experience. AI is already being rolled out in customer-facing operations, but banks will actively be consolidating and automating their mid and back-office procedures for efficiency and automation transition in the post COVID-19 environment. This includes using AI for automating credit operations, policy making and data audits and using RPA for reducing the introduction of errors in datasets and processes.

There is enormous economic pressure to deliver cost savings and reduce risks through the adoption of technology. Financial Services leaders believe that insights gathered from compliance should help other areas of the business, and this requires a completely different mindset. Given the manual and semi-automated nature of current AML compliance, human-only efforts slow down processing timelines and impact business productivity. KYC will leverage AI and real-time environmental data (current accounts, mortgage payment status) and integration of third-party data to make the knowledge richer and timelier in this adaptive economic environment. This will make lending risk assessment more relevant.

#5 Driven by Post Pandemic Recovery, Collaboration Will Shape FinTech Regulation

Travel corridors across border controls have started to push the boundaries. Just as countries develop new processes and policies based on shared learning from other countries, FinTech regulators will collaborate to harmonise regulations that are similar in nature. These collaborative regulators will accelerate FinTech proliferation and osmosis i.e. proliferation of FinTechs into geographies with lower digital adoption.

Data corridors between countries will be the other outcome of this collaboration of FinTech regulators. Sharing of data in a regulated environment will advance data science and machine learning to new heights assisting credit models, AI, and innovations in general. The resulting ‘borderless nature’ of FinTech and the acceleration of policy convergence across several previously siloed regulators will result in new digital innovations. These Trusted Data Corridors between economies will be further driven by the desire for progressive governments to boost the Digital Economy in order to help the post-pandemic recovery.

Organisations are finding that the ways to do work and conduct business are evolving rapidly. It is evident that we cannot use the perspectives from the past as a guide to the future. As a consequence both leaders and employees are discovering and adapting both their work and their expectations from it. In general, while job security concerns still command a big mindshare, the simpler productivity measures are evolving to more nuanced wellness measures. This puts demands on the CHRO and the leadership team to think about company, customer and people strategy as one holistic way of working and doing business.

Organisations will have to re-think their people and technology to evolve their Future of Work policies and strategise their Future of Talent. There are multiple dimensions that will require attention.

Hybrid is Becoming Mainstream

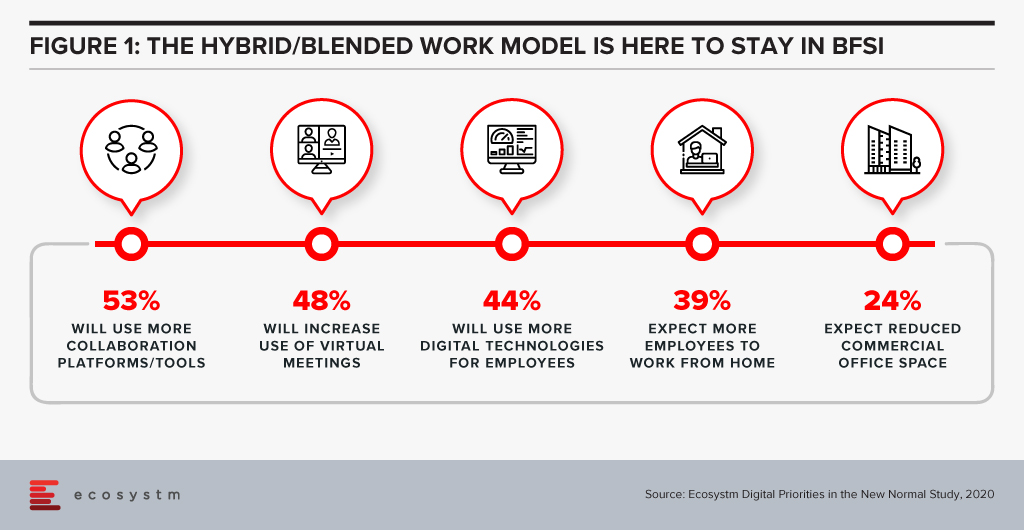

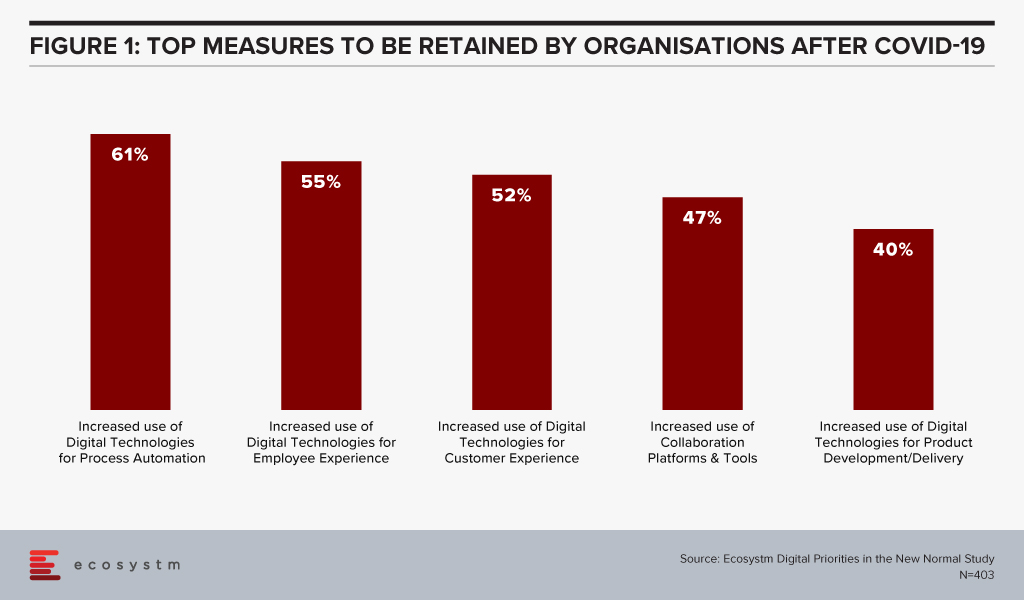

It is clear that hybrid workplaces are here to stay. Ecosystm research finds that in 2021 BFSI organisations will use more collaboration tools and platforms, and virtual meetings (Figure 1). Nearly 40% expect more employees to work from home, but only about a quarter of organisations are looking to reduce their physical workspaces. Organisations will give more choice to employees in the location of their work – and employees will choose to work from where they are more productive. The Hybrid model will be more mainstream than it has been in the last few months.

Companies are coming to terms with the fact that there is no single answer to operating in the new world. Experimentation and learnings are continuously captured to create the right workforce and workplace model that works best. Agility both in terms of being able to undersand the market as well as quickly adapt is becoming quite important. Thus being able to use different models and ways of working at the same time is the new norm.

Technology and Talent are Core

Talent and tech are the two core pillars that companies need to look at to be successful against their competition. It is becoming imperative to create synergy between the two to deliver a superior value proposition to customers. Companies that are able to bring the customer and employee experience journeys together will be able to create better value. HR tech stacks need to evolve to be more deliberate in the way they link the employee experience, customer experience, and the culture of the organisation. That’s how the Employee Value Proposition (EVP) comes to life on a day-to-day basis to the employers. With evolving work models, the tech stack is a key EVP pillar.

Governments will also need to partner with industry to make such talent available. Singapore is rolling out a new “Tech.Pass” to support the entry of up to 500 proven founders, leaders and experts from top tech companies into Singapore. Its an extension of the Tech@SG program launched in 2019, to provide fast-growing companies greater assurance and access to the talent they need. The EDB will administer the pass, supported by the Ministry of Manpower.

Attracting the Right Talent

Talent has always been difficult to find. Even with globalisation, significant investment of time and resources is needed to find and relocate talent to the right geography. In many instances this was not possible given the preferences of the candidates and/or the hiring managers. COVID-19 has changed this drastically. Remote working and distributed teams have become acceptable. With limitations on immigration and travel for work, there is a lot more openness to finding and hiring talent from outside the traditional talent pool.

However it is not as simple as it seems. The cost per applicant (CPA) – the cost to convert a job seeker to a job applicant – had been averaging US$11-12 throughout 2019 according to recruiting benchmark data from programmatic recruitment advertising provider, Appcast. But, the impact of COVID-19 saw the CPA reach US$19 in June – a 60% increase. I expect that finding right talent is going to be a “needle in a haystack” issue. But this is only one side of the coin – the other aspect is that the talent profile needed to be successful in roles that are all remote or hybrid is also significantly different from what it was before. Companies need to pay special attention to what kind of people they would like to hire in these new roles. Without this due consideration it is very likely that there would be difficulty in on-boarding and making these new hires successful within the organisation.

Automation Augmentation and Skills

The pace at which companies are choosing to automate or apply AI is increasing. This is changing the work patterns and job requirements for many roles within the industry. According to the BCG China AI study on the financial sector 23% of the roles will be replaced by AI by 2027. The roles that will not be replaced will need a higher degree of soft skills, critical thinking and creativity. However, automation is not the endgame. Firms that go ahead with automation without considering the implications on the business process, and the skills and roles it impacts will end up disrupting the business and customer experience. Firms will have to really design their customer journeys, their business processes along with roles and capabilities needed. Job redesign and reskilling will be key to ensuring a great customer experience

Analytics is Inadequate Without the Right Culture

Data-driven decision-making as well as modelling is known to add value to business. We have great examples of analytics and data modelling being used successfully in Attrition, Recruitment, Talent Analytics, Engagement and Employee Experience. The next evolution is already underway with advanced analytics, sentiment analysis, organisation network analysis and natural language processing (NLP) being used to draw better insights and make people strategies predictive. Being able to use effective data models to predict and and draw insights will be a key success factor for leadership teams. Data and bots do not drive engagement and alignment to purpose – leaders do. Working to promote transparency of data insights and decisions, for faster response, to champion diversity, and give everyone a voice through inclusion will lead to better co-creation, faster innovation and an overall market agility.

Creating a Synergy

We are seeing a number of resets to what we used to know, believe and think about the ways of working. It is a good time to rethink what we believe about the customer, business talent and tech. Just like customer experience is not just about good sales skills or customer service – the employee experience and role of Talent is also evolving rapidly. As companies experiment with work models, technology and work environment, there will a need to constantly recalibrate business models, job roles, job technology and skills. With this will come the challenge of melding the pieces together within the context of the entire business without falling into the trap of siloed thinking. Only by bringing together businesses processes, talent, capability evolution, culture and digital platforms together as one coherent ecosystem can firms create a winning formula to create a competitive edge.

Singapore FinTech Festival 2020: Talent Summit

For more insights, attend the Singapore FinTech Festival 2020: Infrastructure Summit which will cover topics on Founders success and failure stories, pandemic impact on founders and talent development, upskilling and reskilling for the future of work.

2020 saw a shutdown in both supply and demand which has effectively put the brakes on many economic activities and forced a complete rethink on how to continue doing business and maintain social interactions. The COVID-19 pandemic has accelerated digitalisation of consumers and enterprises, and the telecommunications industry has been the pillar which has kept the world ticking over. The rise in data use coupled with the fervent growth of the digital economy augurs well for the telecom sector in 2021.

Ecosystm Advisors Claus Mortensen, Rahul Gupta, and Shamir Amanullah present the top 5 Ecosystm predictions for Telecommunications & Mobility trends for 2021. This is a summary of the predictions – the full report (including the implications) is available to download for free on the Ecosystm platform.

The Top 5 Telecommunications & Mobility Trends for 2021

- The 5G Divide – Reality for Some and Hype for Others

Despite the economic challenges in 2020, GSMA reports that the global 5G subscriptions doubled QoQ in Q2 2020 to hit at least 137.7 million subscribers. This accounts for 1.5% of total subscribers – and is expected to rise to 30% by 2025.

The value of 5G will become increasingly mainstream in the next few years. 5G offers a tailored user-centric approach to network services, low latency and significantly higher number of connections which will power a new era of mobile Internet of Everything (IoE).

However, there are many operators who are still sceptical about 5G. In the US, many operators failed to get any tangible positives from 5G. In the near term, many operators will continue to evolve their 5G capabilities – a full grown standalone 5G technology implementation in some verticals might take longer.

The unsuccessful launch of 5G by the US operators does not mean that 5G is a failure, however. It also implies that we need to look at other geographies to lead us into 5G – and Asia Pacific may well emerge as a leader in this space. China, for example, leads the drive in 5G adoption; and 5G smartphones account for more than half of global sales in recent months.

- Telecom Operators Will Accelerate Digital Transformation

Telecom operators are facing increasing demands for cutting-edge services and top-notch customer experience (CX). The global pandemic has caused revenue loss, due to struggling economies and many operators will aim to reduce OpEX to circumvent these financial pressures, raise the quality of CX and retain existing customers. To realise this, there will be much focus on improvement in efficiencies, better operations management as well as improving the IT stack. These digital transformation efforts will enable rapid and flexible services provisioning, which will be better prepared for the tailored services customers now demand.

Many operators are increasingly incorporating cloudification alongside the 5G network deployment. Operators are moving towards transforming their operations and business support systems to a more virtualised and software-defined infrastructure. 5G will operate across a range of frequencies and bands – with significantly more devices and connections becoming software-defined with computing power at the Edge. Operators will also harness the power of AI to analyse massive volumes of data from the networks accessed by millions of devices in order to improve CX, ramp up operational efficiencies as well as introduce new services tailored to customer needs to increase revenue.

- Remote Working Will Transform Telecommunications Networks

The changing patterns in peak network traffic and the substantial movement of traffic from central business districts to residential areas require a fundamental rethink in network traffic management. In addition, many businesses continue to ramp up digital transformation efforts to conduct business online as physical channels will remain limited. Consumer onboarding will also be fervent, as organisations look at business recovery – resulting in increase in bandwidth requirements.

The increasing remote working trend is amplifying the need for greater cybersecurity. Cybersecurity has catapulted in importance as the pandemic has seen a worrying increase in attacks on banks, cloud servers and mobile devices, among others. Cyber-attack incidents specifically due to remote working, has seen a rise. A telecom operator’s compromised security can have country-wide, and even global consequences.

- SASE Will Grow – and Sprawl

Although it was perhaps originally seen as an Over-The-Top (OTT) provisioned competitive service to operators’ MPLS services, many telecom service providers have been embracing SD-WAN over the years as part of their managed services portfolio. “Traditional” SD-WAN offers some of the flexibility needed to address the change towards a more distributed access and the workload requirements that the pandemic has accelerated – the technology does not address all of the issues related to this transformed workspace.

Employees are now working from a variety of locations and workloads are becoming increasingly distributed. To address this change, organisations are challenged to move workloads and applications between platforms, potentially compromising security. Despite all the challenges that the pandemic brought with it – both human and technical – it has also provided organisations with an opportunity to rethink their IT and WAN architectures and to adopt an approach that has security at its core.

We believe that secure access service edge (SASE), which is a model for combining SD-WAN and security in a cloud-based environment, will see a drastic rise in adoption in 2021 and beyond.

- OTT Players Will Continue their Expansion in the Telecommunications Space

Facebook, Google, Amazon are no longer considered as web companies as they moved from standalone ‘web’ companies to become OTT providers and are now significant players in telecom space. With the Facebook-Jio deal in India earlier this year, and with Google and Amazon actively eyeing the telecom space, these players will continue to explore this space especially in the emerging markets of Asia and Africa. There are telecom providers in these countries which will be prime targets for partnerships. These operators could be those that have a large customer base, are struggling with their bottom lines or are already looking at exit routes. OTT players were already offering services like voice, messaging, video calling and so on which have been the domain expertise of mobile operators for a long time. The market will see instances where telecom providers will sell small stakes to OTT players at a premium and get access to the vast array of services that these OTT providers offer.

Contact centres were already on a path to modernisation – which got accelerated by the COVID-19 crisis. The need for omnichannel delivery and better insights from customer data has forced contact centres to adopt cloud solutions. Ecosystm Principal Advisor Audrey William says, “There is still a disconnect between integrating and synchronising customer data between Sales, Marketing and Customer Teams. However, the market is starting to see contact centre vendors work closer with vendors in customer experience management segment.”

Genesys and Adobe are collaborating on integrating Genesys cloud and the Adobe Experience Platform. The deeper integration of both platforms is aimed to give organisations a better omnichannel presence. The platform is live for users and Genesys and Adobe will introduce other features and capabilities throughout 2020. Genesys is already a partner of Adobe’s Exchange Program designed for technology partners to supplement Exchange Marketplace with extensions and applications for Adobe Creative Cloud users.

Augmenting the CX journey through Data Synchronization

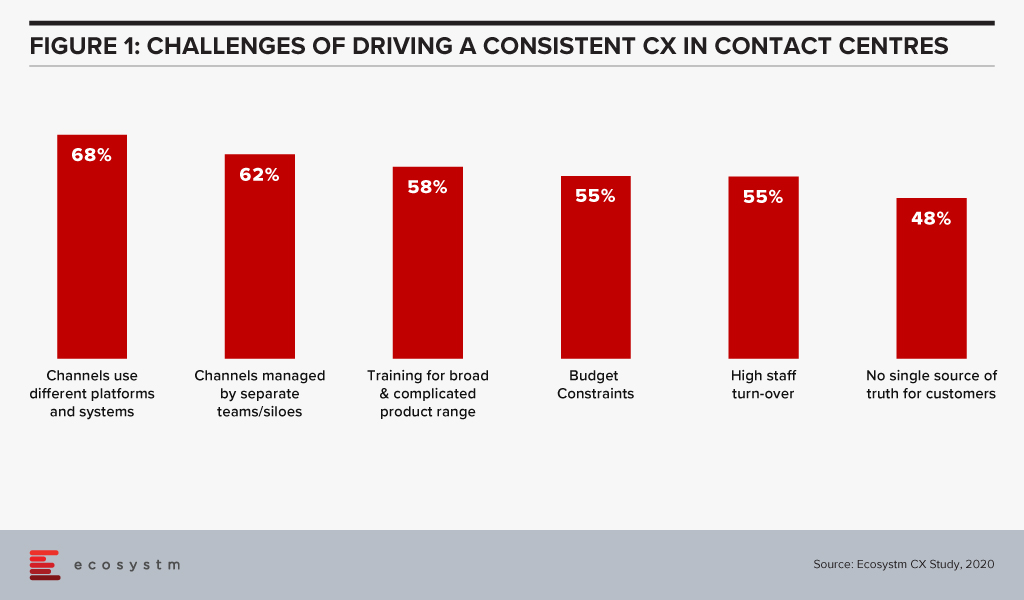

Ecosystm data finds that 62% of contact centres have driving omnichannel experience as a key customer experience (CX) priority and 57% want to analyse data across multiple data repositories. However, when asked about the challenges of driving consistent CX, data access and integration appears to be a barrier in achieving their priorities. These challenges are the reason why getting a “true view” of the customer data has been an arduous task and achieving consistent CX continues to be a struggle.

William says. “The customer data collected by a particular service or department does not always move along in real-time with the customer interactions across different touchpoints. This complicates maintaining a real-time customer profile and impacts the CX.”

“Sales and Marketing have different KPIs and tend to view customer data from different angles. The data from in-store, Marketing and Sales interactions sits within departmental silos. They may deal with the same customers and not follow them through their entire journey. This leads to missed opportunities in reaching out to them at the right time with the right products to upsell, resell or provide better CX. Data synchronisation across channels, would solve that problem.”

Integrating Genesys and Adobe Experience Platform will give organisations the capability to provide contact centre agents with real-time customer data and profiles from a single point to provide an personalised experience. The platform is powered by Genesys Predictive Engagement that uses AI to provide more intelligence based on past interactions to drive effective, data-driven conversations. In addition to this, the partnership also enables businesses and marketing departments to customise campaigns and extend their digital and voice capabilities for optimal conversions. William says, “The ability to use AI to understand customer intent, behaviour and patterns is critical as it will allow brands to re-look at how to design the customer journey. When you keep using the same and outdated profile, it will be hard to have discussions around intent, customer interest and assess how customer priorities have changed. Accurate and automate data profiling will lead to more targeted and accurate marketing campaigns.”

Genesys Deepening Industry Partnerships

Genesys is re-shaping its strategy on Contact Centre as a Service (CCaaS) offerings through partnerships and working on its vision of providing Experience as a Service to its global clients. The need for CCaaS has been accelerated by the pandemic. Last month Genesys signed a five year deal with Infosys to develop and deploy cloud CX and contact centre solutions.

Earlier this year, Genesys partnered with MAXIMUS, a US Government services provider to set up the MAXIMUS Genesys Engagement Platform, an integrated, cloud-based omnichannel contact centre solution driven by the government requirement for public sector organisations to provide seamless customer experiences similar to those offered in the private sector.

The company has also partnered with various other industry leaders like Microsoft, Google Cloud, and Zoom to roll out cloud-based innovations to benefit customers.

Click below to access insights from the Ecosystm Contact Centre Study on visibility into organisations’ priorities when running a Contact Centre (both in-house and outsourced models) and the technologies implemented and being evaluated

The COVID-19 crisis has required major resets in how organisations function – across industries and economies. In this environment of intense changes, businesses that have been agile in their operations and were better digitally enabled have thrived, while others have struggled. Irrespective of whether an organisation has been able to pivot fast to thrive or struggled to cope, it is very clear that the Future of Work is here now. Every organisation has had to make some changes to their People and work practices. It is time to (re) focus on employee experience holistically so that organisations can be ready for whatever model of work becomes prevalent in the future. I have recently published a report offering guidance to business leaders and HR Teams on how to make holistic workplace shifts, with inputs from Ecosystm Principal Advisors, Tim Sheedy and Audrey William.

Employee Experience at the Core of Customer Strategies

It has become increasingly clear that customer experience (CX) is not just about good sales skills or customer service. It is about the overall experience of the customer from start to post-purchase. Customers are focused on not just what they are buying but also on how they are treated along their entire journey. Good CX has consistently shown to help increase price premium, impulse buying, and loyalty. Consequently, one bad experience can drive a customer away forever. Customers pay for your products or services, but it is your people who can really deliver the experience.

Audrey says, “As it becomes clear that we are headed for a hybrid/blended model of work, employee experience (EX) has to be a key focus area for organisations. Organisations will have to support remote work and simultaneously evolve their physical workplaces so that employees have the choice to come into work. But business leaders and HR will definitely have to come together to re-evaluate their policies around employees and improving EX – irrespective of where they choose to work from.”

The Role of Productivity in the Digital Workplace

Productivity has been at the core of an organisation’s desire to be a digital workplace. Tim says, “A digital workplace is one that has the capability to support any employee to access the process, information or system they need on their device of choice, in their moment and location of need. In the wake of the pandemic, the digital workplace went from being a ‘good idea’ to an ‘absolute necessity’ – and the seeds were sown to build true digital workplaces, years ahead of plan.”

This is the time to retain that focus on productivity. A lot of energy is being spent in defining and measuring productivity. The focus seems to have shifted to how to get the best out of the remote/hybrid workforce. It is time for business leaders and HR to go back to the drawing board to re-define what productivity means to their organisations.

Tim says, “The focus should be on enabling productivity rather than on monitoring activity. Productivity is an outcome, not a process. So, measure the outcome, improve the process. Productivity will be driven at an organisational level through removing friction from overall operational processes, to make things more streamlined and effective to create more value.”

The True Implication of Flexibility

There has been a rapid shift in practices around working from home and flexibility. But it is time now for organisations to create a framework (policy, performance expectation and management) to manage these practices. Many companies do not really understand the implications of flexible working to their business. In fact, they may be unaware of shifts in work patterns that have taken place in the last few months and the impact these shifts are having on the business.

Framework around flexible working should be backed by data and an understanding of the feasibility of such practices. If your employee has to work on her compulsory day off, then you do not have a truly flexible work practice. This will have a negative impact on employee experience and ultimately on your business.

The Evolution of Employee Engagement

Audrey says, “One of the areas that business leaders and HR will have to bear in mind is that despite flexible working hours, employees might be overworked – it is emerging as a common problem with working from home. It is common that many employees are working longer hours.”

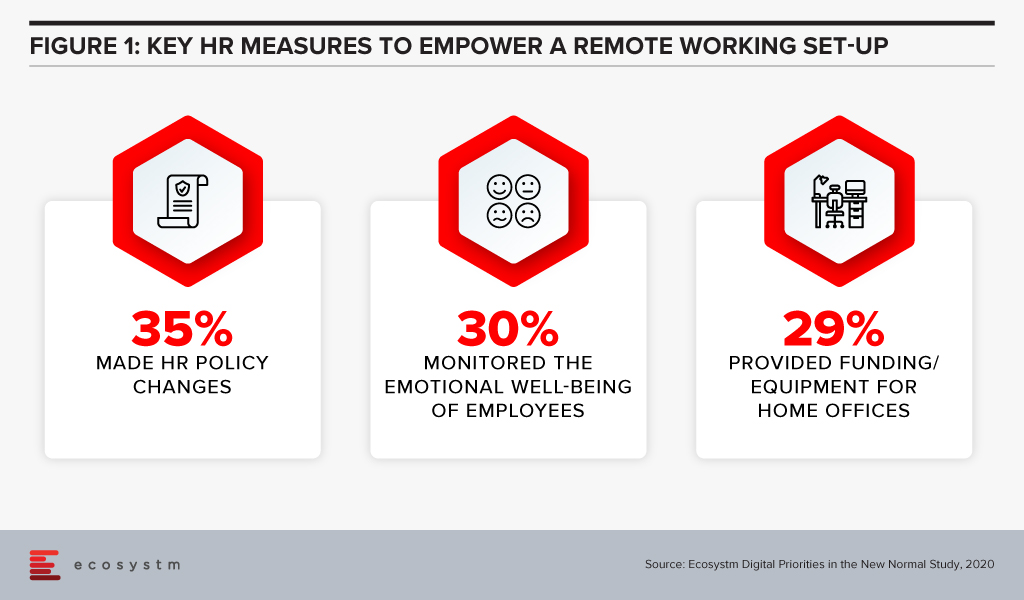

Ecosystm research finds that some organisations have been evolving their HR practices, since the start of this crisis (Figure 1).

But more needs to be done. Organisations have to work really hard to replicate their employee engagement and social hours in the virtual world. It is critical that organisations design mechanisms of keeping employees connected – to each other, as well as to the organisation. “Virtual social groups” not only provide this connection, it can also be a rich source of input for HR and wellness teams to quickly adapt their programs to meet the changing needs of employees.

Shift in Managerial Styles

Performance management has been traditionally done through annual cycles, and by monitoring and tracking. In the Future of Work, organisations will have to increasingly give their employees the choice of working from home. Meetings, check-ins, 1:1 and team huddles for close monitoring will not work in this remote/hybrid model.

It is time to stop close monitoring and really focus on outcome-based management. And this will have to start with re-skilling people managers. Training should be provided on softer skills such as emotional intelligence, being able to sense across boundaries and digital spaces, and being able to be responsive to employees’ needs. The people manager must evolve into being a coach and a mentor – internal coaching and mentoring networks will have to be established. Line managers, business leaders and HR teams will need to collaborate more to ensure that these skills are developed and that the right support system is in place.

Your CEO and Board are asking you to cut costs and do more with the IT budget.

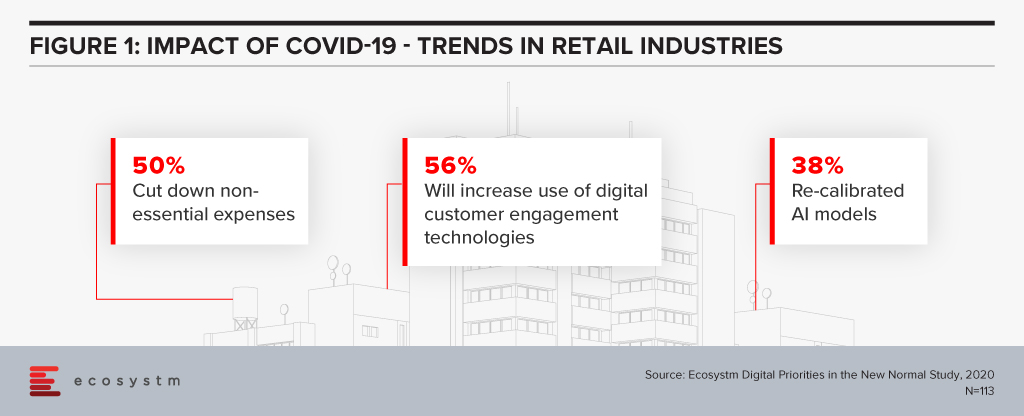

This is the usual refrain you get used to as a Chief Digital or Information Officer. COVID-19 has increased the need for cost savings, without compromising your organisation’s mission. In Ecosystm’s on-going research, Digital Priorities in the New Normal – a COVID-19 Study, there are several common themes that emerge for retailers.

The impact of the cost-cutting measures that organisations are implementing, on CDOs and CIOs has been discussed in my report Managing Costs in the New Normal, where I provide guidance on how to address the necessary cuts.

Super Retail Group (SRG) recently presented at SalesForce Live on their success in using AI to improve their customer engagement – linking digital customer engagement and re-calibration of AI models. I want to highlight a couple of aspects of SRG’s experience for those retailers addressing these themes.

Increasing Customer Engagement

In a well-run online presence, retailers acquire a significant amount of data about their customers’ online behaviour. Data such as customer’s purchase history as well as how they traverse the site, how long they remain on the site and how they leave – often without purchasing. The challenge is how you can collect and use this data to improve the customer experience (CX) and increase sales in our new normal.

SRG, trading under banners such as Super Cheap Auto, BCF and Rebel across Australasia, has adopted a Salesforce tool called Einstein to address this challenge. SRG is using this AI engine to present product recommendations in several contexts across a customer’s online journey.

The impact of COVID-19 means overall sales across the group has declined. At the same time, online sales have grown to be generating almost 20% of the overall sales. Within these online sales, the AI recommendation engine has directly influenced 1 in 5 customer purchases.

SRG has developed a significant base of customer data since they introduced omnichannel and club offers; and are now seeing the return from this investment. Recommendation engines operate best when they have quality data in volume – and the proportion of and growth in, online customers using these recommendations is a guide to the quality of the platform.

Coping with Increasing Online Demands

Ecosystm research finds that over 56% of retailers are increasing their use of digital technologies for CX and will continue to invest after the immediate crisis. As always, getting the right value from this increased expenditure will be critical to a retailer’s price competitiveness and profitability.

With online sales growing dramatically, SRG’s online share of sales has more than doubled over April and May, the potential return from an engaging online CX has increased significantly. In turn, this has increased the importance of the online CX to a retailer’s competitive positioning and market share.

Tech leaders will be expected to provide direction on how to achieve this improvement, with AI engines offering an increasingly important tool in increasing the speed of response to changing customer behaviours.

With their mapping of customer journeys, SRG has been able to target specific stages in the journey for the use of the AI recommendation engine. Their focus on increasing the size and value of a customer’s basket provides the explicit measure of success. And SRG’s customers are showing their enthusiasm for these recommendations. The share of online sales influenced by the AI engine grew by over 600% in the past 12 months.

Customer expectations are continually being redefined by their experiences across the online environment, not just by retailers. In our new normal, with online becoming significantly important, retailers need to be consistently improving their offer to remain competitive.

Our study results shows that retailers are taking this step and will need to pay careful attention to their cost base and profitability while making these changes. SRG’s success with the AI engine shows that this is possible.

Lessons to Learn

COVID-19 has changed customer behaviour significantly, and tech leaders are identifying new tools and processes to improve their CX in line with these changes. SRG has continued its customer-focused omnichannel approach by adopting the Salesforce Einstein AI engine. By using one of their key sales metrics – size and value of basket – they have been able to assess the contribution of this tool.

There are some clear lessons for other retailers from their experience:

- Be very clear on why you are introducing the new tool – how you are going to achieve value.

- Understand the foundation that you need, to introduce new technology. You will find being successful using AI without quality data in volume will be difficult.

- Experiment and learn quickly from experience gained. In this cost-constrained world, don’t over-commit to a new approach without evidence.

- Use products and services that have a low cost of entry and a variable cost model. Cloud services generally provide this cost model.

Our research, along with press release such as SRG’s, show that retail leaders are continuously improving their customer engagement. As a tech leader, you need to be aware that customers will vote with their clicks, for retailers that are delivering.

And getting those non-essential costs out has never been more critical.

I recently came across an article which makes 7 predictions for a post COVID world. Upon reflection, I agree with the predictions to varying degrees and decided to comment further.

First, let me share a couple of general observations. Currently, we are still in the eye of the storm. Many are unable to see any light at the end of the tunnel. There is quite a bit of negative sentiments, and some fail to see that the situation will ever improve. I am sure similar thoughts occurred during other crises: the 1918 Pandemic (Spanish Flu); the Great Depression of the 1930s; the Dot.com bust of 2001; SARS in 2003; and the Global Financial Crisis/Great US Recession of 2007. During each of these events, a sense of impending Armageddon came over much of the population. Certainly, in each instance, people did experience some personal and social permanent changes, with which they learned to adapt and cope. But, inevitably, the world did go on and Armageddon did not occur.

One of the basic truths I believe, is that humans require and crave interaction with other humans. Think about the videoconferencing applications. The use of these apps grew exponentially as the main communication channel. Instead of just audio, it was audio and video. These mediums greatly assisted society in coping and adapting. Mankind, and the Natural World, will always find a way.

Here are the predictions from the article:

- Companies that traffic in digital services and e-commerce will make immediate and lasting gains

- Remote work will become the default

- Many jobs will be automated, and the rest will be made remote-capable

- Telemedicine will become the new normal, signaling an explosion in med-tech innovation

- The nationwide student debt crisis will finally abate as higher education begins to move online

- Goods and people will move less often and less freely across national and regional borders

- After an initial wave of isolationism, multilateral cooperation may flourish

I very much agree with the author’s first prediction. This one is fairly obvious, as it has proven true throughout the crisis with providers such as Amazon, Zoom and others. It is expected to continue into the post COVID world. This is also evident from the findings of the Ecosystm research on the impacts of COVID-19. Organisations intend to continue to use digital technologies, even after the immediate crisis is over (Figure 1).

A Natural State of Equilibrium will Emerge

I believe for each of the areas described in the predictions, there will be various levels of long-term modification. None of them will return to their pre COVID-19 state, as we have all experienced going down the rabbit hole. During the pandemic, due largely to the lockdowns, the pendulum swung significantly towards one side. Many times, when people predict a new view, the current state is considered the New Normal. For me, the relevant question is: Will things stay as they are now, or will there be a new natural state of equilibrium? If so, what will it look like, in each of these areas? I don’t believe there is one answer, or one New Normal for all the dimensions being discussed. I believe a new normal state will potentially be different for each individual, each company/entity and each condition. In a post COVID-19 world there could be 50 shades of grey in each of these areas.

One of the predictions states that remote work will become the default. It must be remembered that part of work is a collaborative effort. While video conferencing has enabled collaborative efforts, the importance of the accidental interaction at the break room, printer, etc. can’t be under-estimated. It is these unscheduled interactions that enable accidental collaboration which can lead to great solutions. Thus, there will be many shades to the Future of Work – there will not be one absolute.

A similar example is a prediction for higher education. Part of the learning process a university offers is interacting with people who are not similar to your background or beliefs. That is one of the benefits of a diverse university. Similar to the corporate environment, many different types of learning environments will enable a person to gain great experiences from the time at university.

The advantage of all these alternatives will be the additional options and benefits to people post COVID compared to the pre COVID-19 world. It will present many great opportunities for entrepreneurs and innovators, as well as end-users and consumers. It will create new and iterative ‘middle spaces’. It will be possible for a David to emerge and challenge a Goliath(s).

The two Chinese characters for the word ‘crisis’ are “danger” and “opportunity”. Just as we are in a dangerous time now, it has also presented new and different opportunities. Those opportunities will continue to exist even when the danger has passed. I am also reminded of the old expression “May you live in interesting times”. It very much applies to all of us now and in the future. I wish the same for all of you.

Stay Safe. Stay Healthy. Stay Mentally Positive.

The COVID-19 pandemic has presented us with a set of circumstances that we have never seen before – health, safety, and economic livelihoods are being affected. Companies are being asked to take on roles that they are not familiar with. The global situation continues to evolve rapidly, and we are all having to adapt as we go. During this time, the expectations of customers and employees are evolving in tandem. Companies should look at understanding this evolution and take fuller advantage of the opportunity this evolution will present.

CX at the Centre Stage

Customers have always been the top priority for businesses. In the last few years, we have seen the transition that organisations are making from selling to creating; evolving from selling products to solutions to experiences. This has led to reframing of the selling methodology and, consequently, the technology and people skills needed to make that happen.

While companies have been able to understand the need to make this shift intellectually, it needs to be backed by the right investments in their people and customers. However, industry estimates find that only about 10% of organisations put money where their mouth is. Those that have been able to do so, have been consistently able to meet and exceed their goals.

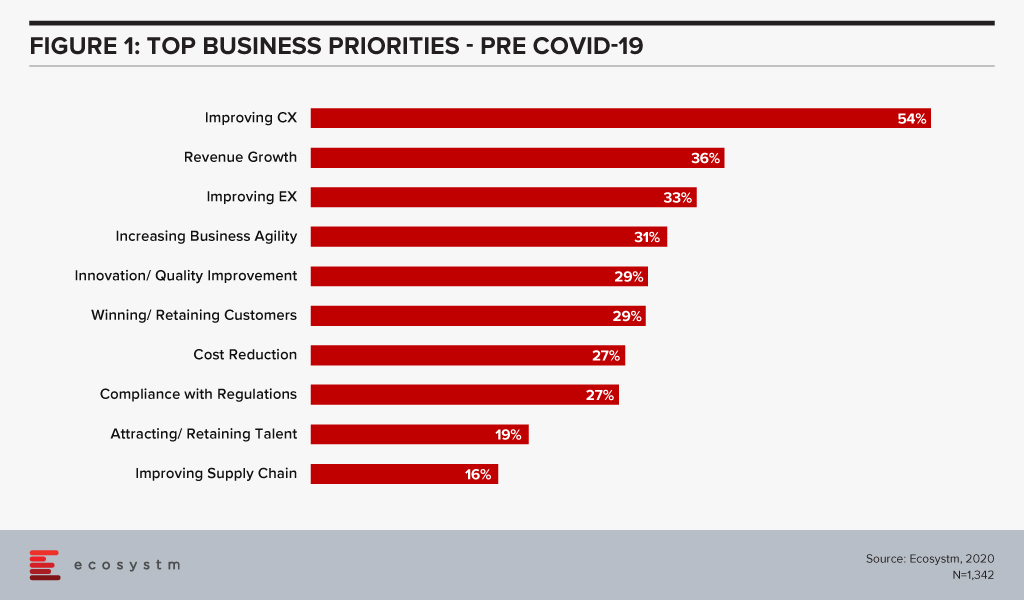

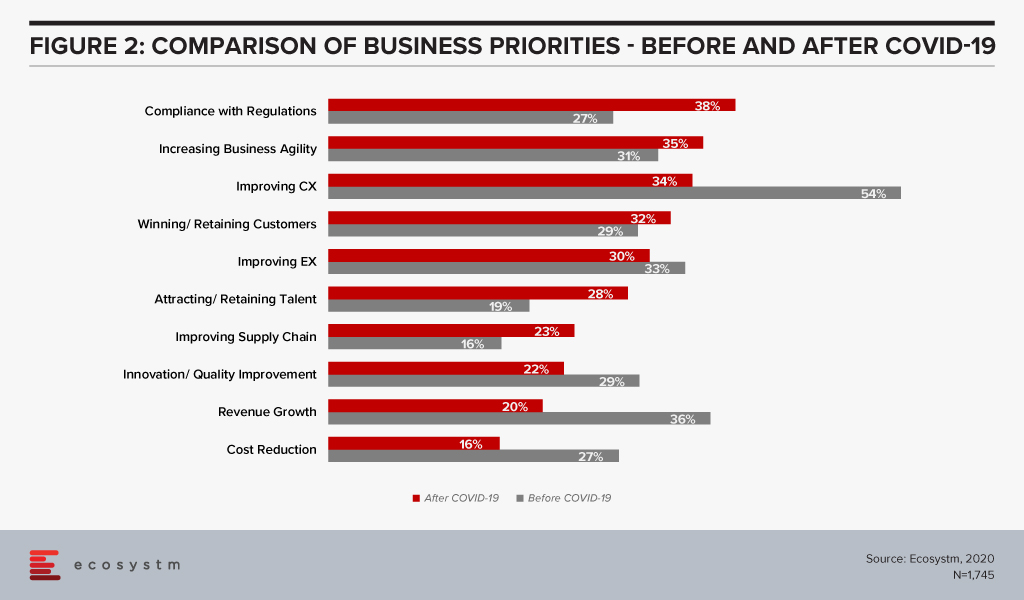

As such, investments in customer experience (CX) technology is taking centre stage. Ecosystm research finds that improving CX has been the top business priority for organisations, before COVID-19 (Figure 1).

If we take a deeper dive into CX, it becomes clear that CX is not just about good sales skills or customer service. It is about the overall experience of the customer from start to post-purchase. Customers are focussed on not just what they are buying but also on how they are treated along their entire journey. Good CX has consistently shown to help increase price premium, impulse buying and loyalty. Consequently, one bad experience can drive a customer away forever.

So, what does improving CX look like? A vast majority would think technology. That is only part of the story; the key component of making your CX strategy come to life is your people. Customers pay for your products or services, but it is your people who can really deliver the experience. Glassdoor research shows that there is a clear link between employee and customer satisfaction. On an average, a 1-point increase in company rating on Glassdoor is associated with a 1.3-point increase in customer satisfaction, measured by the American Customer Satisfaction Index (ACSI).

So, the fact that only 33% prioritise employee experience (EX) (Figure 1) shows a gap in understanding how to achieve excellent CX. In this gap lies the true opportunity of gaining sustainable competitive advantage.

Reset During COVID-19

Due to COVID-19 all of us have had to re look at who we are and how we operate. It has really changed the world of work and business, almost overnight. Companies have invested a significant amount of time on just enabling their employees to stay safe and work from home. Overnight, access to physical offices was gone and everyone was transitioned to digital workspaces.

The Ecosystm Digital Priorities in the New Normal study, that was initiated to gauge the immediate and longer term impact of the pandemic finds that during the crisis, the focus on employees increased drastically, with 75% of organisations introducing measures to manage their employees, while 30% focused more on their customers.

This is a complete reversal in the focus of the organisations. Employees have come into sharper focus. This should be good news. Yes, it is – but partly so.

Initial focus has been rightly on safety and on employees being able to work from home. This was an “adapt” mode, focussed on services like payroll, handling employee queries and onboarding without disruption. After the initial crisis-handling, organisations have been able to focus on digital learning and skills enhancement, while others have been trying to increase productivity (predominantly through giving access to collaboration tools).

The Journey Ahead

As we continue to work in the new normal, one thing comes out even stronger: the new experience needs to be seamlessly connected between all channels – and be agile and more human. It is now even more evident that organisations and people – that are its lifeblood – need to constantly adapt and pivot to meet these changing landscapes.

Customer expectations have evolved in the last few months from a cost and product view, to being loyal to companies that show more empathy and are able to solve their problems. Employee expectations have also evolved, simultaneously – and it now goes beyond a good pantry and an engaging, fun-loving environment. Employees today value connectedness, and expect the organisation to show more care (so they can do their work effectively), and create opportunities for them to grow (job security) as they continue to grapple with the situation.

Thus, the more relevant the EX product and the faster it can adapt to the evolving situation, the better it translates into better engagement and loyalty. But what will definitely be required of organisations, is a continued focus on their employees. If we compare the business priorities before and after COVID-19, we get an indication that EX might once again be left behind in organisations’ obsession about their customers (Figure 2).

The gap is not as wide as before COVID-19 hit us – but there appears to be a shift towards a customer focus. This is evolving differently from our expectations and can potentially cause a misalignment.

Opportunity to Reshape

The reset has pushed EX and CX expectations closer to each other when it comes to designing experience with the company. The opportunity lies in taking a more holistic view of the company business – bringing HR, IT, Customer Success and Marketing teams together into agile tribes and guilds – to design a consistent CX by improving EX.

This would help to increase the speed of prototyping new experiences, and consequently drive greater visibility of what is needed – from skills to IT systems. Overall, it will drive a greater degree of connectedness between the employee and customer worlds; resulting in better engagement and loyalty.

A decade ago, the axiom of a successful business model was to identify a need, find the market and then develop an idea or product that fits into that chain. It was a process of inserting a product in the customer’s already existing experience journey with the hope that the product/idea would deliver efficiency to the client. This efficiency could be financial, operational, marketing or cost savings – the uni-product, uni-feature approach.

There has been enough said about the many companies that failed to innovate beyond their existing product/feature and failed to stay ahead of the game. Nokia and Blackberry remain at the centre of any discussion about “lack of innovation”. There are others like Kodak, Canon, Napster, Palm, Blockbuster – that were devoured by innovative competitors.

The predators were ones with the vision to see the entire value chain and not just their own product. Netflix created content and distributed it, Apple touched the lives of their customers in multiple ways and AirBnb provided accommodation inventory, choice and booking all in one. The new secret sauce is to provide the customer with an ecosystem and not a product!

The Need to Transform

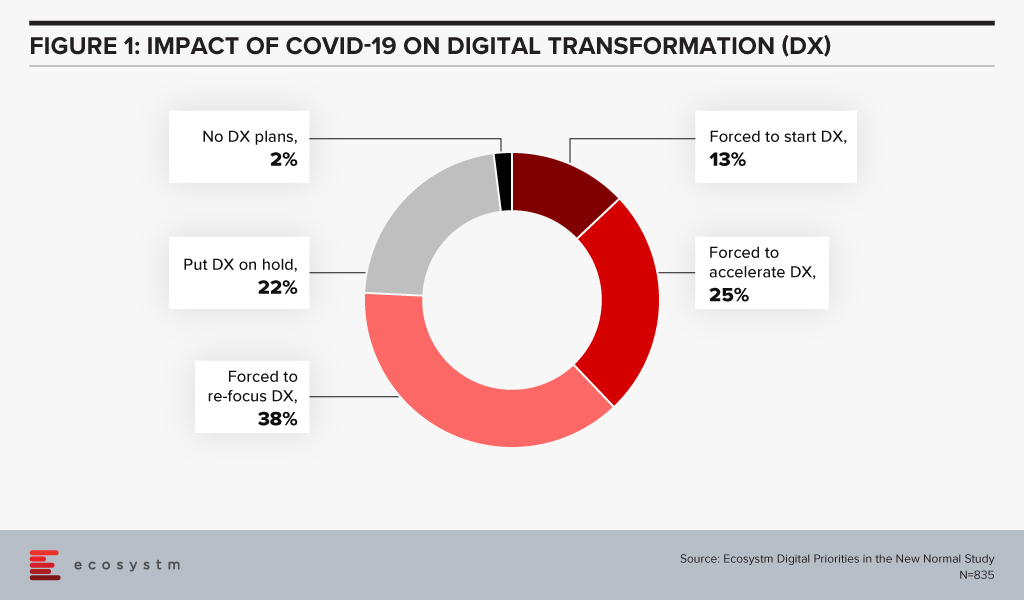

Cut to the COVID era – there are many businesses facing the downturn and experiencing the “moments of truth” giving rise to a desperate attempt to innovate, transform, survive, and come out as the rising stars. Ecosystm research finds that 98% of organisations have re-evaluated their Transformation roadmap (Figure 1), while 75% have started, accelerated or refocused their DX initiatives.

New business models are evolving, and accelerating digitalisation is the result. The digital movement, be it in food delivery or payments, is here to stay. This digital acceptance and absorption exaggerate the need for business models that capture holistic ecosystems and entire customer journeys, due to reasons that separate the hunter and the hunted.

- Margins will never be the same again as in the uni-product model. Using the F&B analogy; with the increasing number of customers wanting to dine in the comfort of their homes, restaurants cannot use ambiance as the price differentiator. Since most restaurants are available on food delivery services, customers are getting brand agnostic. This is the start of commoditisation of dining. Restaurants (or food caterers now!) will need to play the price card to remain competitive resulting in compressed margins. The food delivery market is expected to grow 4-fold to USD 8 billion by 2025 but with lower margins. This example of the food delivery model will be the same as experienced by retail, apparel and other industries.

- Customer experience will still be the differentiator and lever for loyalty and repeat purchase. Factors like proximity, parking, in-store experience, and store layout are fast getting replaced by the ease of navigation, user experience, seamless check out and finally efficient and timely delivery. The ease of transaction including multiple steps of search, assessment, evaluation, payment and delivery is of paramount importance. Customers do not want fractured journeys with multiple drop-offs. A unified seamless journey will win.

- Virtual, Digital and Automation are the three mantras that management consultants are betting on. However, this trilogy will not guarantee survival since the road to recovery is not a straight one. Different work schedules, observing various curves and on what point of the curve the business, its customer and the market are at, will add to the complexity of decision making and transformation.

Given the above, an obvious strategy to beat the existential crisis is to transform and seek out sustainable operating models. However, it may not be so simple since most businesses may not be able to change models as quickly as needed. There is an inherent cost to change since the existing processes and procedures have been well oiled and smoothed over time. The much-needed change requires the infusion of the 3Ts (time, technology, training) and associated costs. Most often, there is an inverse correlation noticed between the sturdiness of the business and its ability to be flexible to change. Businesses that are “rock-solid” and profitably sturdy and stable, have high inertia of transformation versus FinTech businesses, as an example, that pride themselves with nimble operations but are financially fragile and may not be able to absorb the cost of speedy transformation.

This Sturdy-Flexible continuum is the tight rope walk that businesses will need to walk in this need for transformation. Businesses that embark on this walk alone will find it extremely painful and lonely. Especially in the case of small business owners who are scared and low on all 3Ts.

The Rise of Ecosystems

The new world has manifested that businesses that use physical space or assets as their competitive advantage are more prone to be impacted. Retail, Education, Hospitality and Entertainment are some obvious examples that have been impacted by the physicality in their propositions. Digital businesses are more agile but have suffered in their inability to scale up in time to capture the increased demand.

Fashion retailer FJ Benjamin has decided to shut 300 physical stores and rely on online sales. This strategy also helps to utilise precious time to scale diversification. Other retailers too have been going down the FJ Benjamin path and ramping up eCommerce as this trend is expected to stick beyond COVID-19.

Zouk, the renowned nightclub with 30,000 square feet of space in Singapore uses this venue as a live streaming venue during the day to host bazaars for eCommerce vendors. From June 2020, it launched an online shop selling merchandise, bottled cocktails and food from its RedTail kitchen.

Transformation of businesses will require capabilities that were not created within their models. The instinct to survive in the short term will require businesses to create symbiotic partnerships. This will require some fresh thinking by business leaders.

- Change the “Build” obsession and not try to own every leg of the customer journey. That will not only take time but also distract capital and management.

- Rethink the customer needs – and this time think of the entire journey rather than an inward view of product-market fits. Customer needs are changing at breakneck speeds, so chasing and “building” these “fits” will always remain a common string amongst laggards.

- Connect with like-minded ecosystem players and complement strengths with a single-minded focus on solving customer problems.

- View technology stacks through the lens of your partners. There may be opportunities available from near open source technology solutions.

For example, FJ Benjamin will need the last-mile-delivery capability that will be provided by partners who have optimised in that field, Zouk has tied up with Lazada to host the bazaars and GrabFood is using underutilised taxi capacity to meet the increased demand for food delivery. There are many other examples in the O2O (Offline to Online) space.

This ecosystem approach is also relevant to other sectors like Financial Services. These firms also need to understand the changing consumer needs faster, with a mantra to deliver. Aspire, originally an alternate lending platform has gone through a metamorphosis and transformed into a Neobank. From a uni-product loan provider, it is now solving for a business account, card solution, integration with expense management solutions and continue to provide loans. Capabilities not necessarily built in-house.

The changing world will give rise to business models that will integrate and complement each other. Businesses with an ecosystem mindset will be winners while others might just be relegated to oblivion.