Southeast Asia’s banking sector is poised for significant digital transformation. With projected Net Interest Income reaching USD 148 billion by 2024, the market is ripe for continued growth. While traditional banks still hold a dominant position, digital players are making significant inroads. To thrive in this evolving landscape, financial institutions must adapt to rising customer expectations, stringent regulations, and the imperative for resilience. This will require a seamless collaboration between technology and business teams.

To uncover how banks in Southeast Asia are navigating this complex landscape and what it takes to succeed, Ecosystm engaged in in-depth conversations with senior banking executives and technology leaders as part of our research initiatives. Here are the highlights of the discussions with leaders across the region.

#1 Achieving Hyper-Personalisation Through AI

As banks strive to deliver highly personalised financial services, AI-driven models are becoming increasingly essential. These models analyse customer behaviour to anticipate needs, predict future behaviour, and offer relevant services at the right time. AI-powered tools like chatbots and virtual assistants further enhance real-time customer support.

Hyper-personalisation, while promising, comes with its challenges – particularly around data privacy and security. To deliver deeply tailored services, banks must collect extensive customer information, which raises the question: how can they ensure this sensitive data remains protected?

AI projects require a delicate balance between innovation and regulatory compliance. Regulations often serve as the right set of guardrails within which banks can innovate. However, banks – especially those with cross-border operations – must establish internal guidelines that consider the regulatory landscape of multiple jurisdictions.

#2 Beyond AI: Other Emerging Technologies

AI isn’t the only emerging technology reshaping Southeast Asian banking. Banks are increasingly adopting technologies like Robotic Process Automation (RPA) and blockchain to boost efficiency and engagement. RPA is automating repetitive tasks, such as data entry and compliance checks, freeing up staff for higher-value work. CIMB in Malaysia reports seeing a 35-50% productivity increase thanks to RPA. Blockchain is being explored for secure, transparent transactions, especially cross-border payments. The Asian Development Bank successfully trialled blockchain for faster, safer bond settlements. While AR and VR are still emerging in banking, they offer potential for enhanced customer engagement. Banks are experimenting with immersive experiences like virtual branch visits and interactive financial education tools.

The convergence of these emerging technologies will drive innovation and meet the rising demand for seamless, secure, and personalised banking services in the digital age. This is particularly true for banks that have the foresight to future-proof their tech foundation as part of their ongoing modernisation efforts. Emerging technologies offer exciting opportunities to enhance customer engagement, but they shouldn’t be used merely as marketing gimmicks. The focus must be on delivering tangible benefits that improve customer outcomes.

#3 Greater Banking-Fintech Collaboration

The digital payments landscape in Southeast Asia is experiencing rapid growth, with a projected 10% increase between 2024-2028. Digital wallets and contactless payments are becoming the norm, and platforms like GrabPay, GoPay, and ShopeePay are dominating the market. These platforms not only offer convenience but also enhance financial inclusion by reaching underbanked populations in remote areas.

The rise of digital payments has significantly impacted traditional banks. To remain relevant in this increasingly cashless society, banks are collaborating with fintech companies to integrate digital payment solutions into their services. For instance, Indonesia’s Bank Mandiri collaborated with digital credit services provider Kredivo to provide customers with access to affordable and convenient credit options.

Partnerships between traditional banks and fintechs are essential for staying competitive in the digital age, especially in areas like digital payments, data analytics, and customer experience.

While these collaborations offer opportunities, they also pose challenges. Banks must invest in advanced fraud detection, AI monitoring, and robust authentication to secure digital payments. Once banks adopt a mindset of collaboration with innovators, they can leverage numerous innovations in the cybersecurity space to address these challenges.

#4 Agile Infrastructure for an Agile Business

While the banking industry is considered a pioneer in implementing digital technologies, its approach to cloud has been more cautious. While interest remained high, balancing security and regulatory concerns with cloud agility impacted the pace. Hybrid multi-cloud environments has accelerated banking cloud adoption.

Leveraging public and private clouds optimises IT costs, offering flexibility and scalability for changing business needs. Hybrid cloud allows resource adjustments for peak demand or cost reductions off-peak. Access to cloud-native services accelerates innovation, enabling rapid application development and improved competitiveness. As the industry adopts GenAI, it requires infrastructure capable of handling vast data, massive computing power, advanced security, and rapid scalability – all strengths of hybrid cloud.

Replicating critical applications and data across multiple locations ensures disaster recovery and business continuity. A multi-cloud strategy also helps avoid vendor lock-in, diversifies cloud providers, and reduces exposure to outages.

Hybrid cloud adoption offers benefits but also presents challenges for banks. Managing the environment is complex, needing coordination across platforms and skilled personnel. Ensuring data security and compliance across on-prem and public cloud infrastructure is demanding, requiring robust measures. Network latency and performance issues can arise, making careful design and optimisation crucial. Integrating on-prem systems with public cloud services is time-consuming and needs investment in tools and expertise.

#5 Cyber Measures to Promote Customer & Stakeholder Trust

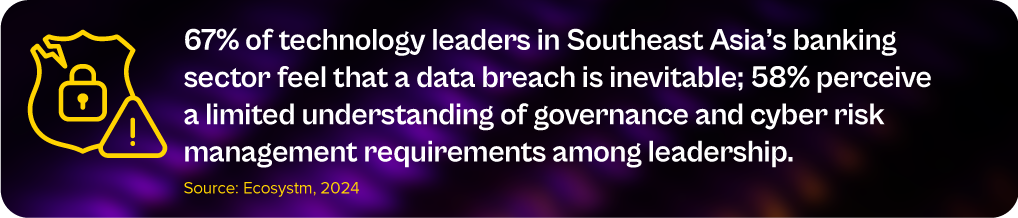

The banking sector is undergoing rapid AI-driven digital transformation, focusing on areas like digital customer experiences, fraud detection, and risk assessment. However, this shift also increases cybersecurity risks, with the majority of banking technology leaders anticipate inevitable data breaches and outages.

Key challenges include expanding technology use, such as cloud adoption and AI integration, and employee-related vulnerabilities like phishing. Banks in Southeast Asia are investing heavily in modernising infrastructure, software, and cybersecurity.

Banks must update cybersecurity strategies to detect threats early, minimise damage, and prevent lateral movement within networks.

Employee training, clear security policies, and a culture of security consciousness are critical in preventing breaches.

Regulatory compliance remains a significant concern, but banks are encouraged to move beyond compliance checklists and adopt risk-based, intelligence-led strategies. AI will play a key role in automating compliance and enhancing Security Operations Centres (SOCs), allowing for faster threat detection and response. Ultimately, the BFSI sector must prioritise cybersecurity continuously based on risk, rather than solely on regulatory demands.

Breaking Down Barriers: The Role of Collaboration in Banking Transformation

Successful banking transformation hinges on a seamless collaboration between technology and business teams. By aligning strategies, fostering open communication, and encouraging cross-functional cooperation, banks can effectively leverage emerging technologies to drive innovation, enhance customer experience, and improve efficiency.

A prime example of the power of collaboration is the success of AI initiatives in addressing specific business challenges.

This user-centric approach ensures that technology addresses real business needs.

By fostering a culture of collaboration, banks can promote continuous learning, idea sharing, and innovation, ultimately driving successful transformation and long-term growth in the competitive digital landscape.

India’s digital journey has been nothing short of remarkable, driven by a robust Digital Public Infrastructure (DPI) framework known as the India Stack. Over the past decade, the government, in collaboration with public and private entities, has built this digital ecosystem to empower citizens, improve governance, and foster economic growth.

The India Stack is a set of open APIs and platforms that provide a foundation for large-scale public service delivery and innovation. It enables governments, businesses, startups, and developers to leverage technology to offer services to millions of Indians, especially those in underserved areas.

The India Stack is viewed as a layered infrastructure, addressing identity, payments, data, and services.

Click here to download The India Stack: A Foundation for Digital India as a PDF

Four Pillars of the Digital Stack

The four layers of India Stack include:

- Presenceless Layer. Aadhaar enables remote authentication, providing a digital ID that requires only a 12-digit number and a fingerprint or iris scan, eliminating the need for physical documents. It prevents duplicate and fake identities.

- Paperless Layer. Reliance on digital records, using Aadhaar eKYC, eSign, and Digital Locker. It enables secure digital storage and retrieval, creating a paperless system for verifying and accessing documents anytime, on any device.

- Cashless Layer. Led by NPCI, this aims to universalise digital payments. UPI enables instant, secure money transfers between bank accounts using a simple Virtual Payment Address (VPA), moving transactions into the digital age for transparency and ease of use.

- Consent Layer. Enables secure, user-controlled data sharing through electronic consent, allowing data to flow freely. The Account Aggregator ecosystem benefits most, with AA acting as a thin data aggregation layer between Financial Information Providers (FIPs) and Financial Information Users (FIUs).

The Impact of the India Stack

The India Stack has played a pivotal role in the country’s rapid digitalisation:

Financial Inclusion. Aadhaar-enabled payment systems (AePS) and UPI have significantly expanded financial access, increasing inclusion from 25% in 2008 to 80% in 2024, particularly benefiting rural and underserved communities.

Boost to Digital Payments. The India Stack has fuelled exponential growth in digital payments, with UPI processing 10 billion monthly transactions. This has driven the rise of digital wallets, fintech platforms, and digitisation of small businesses.

Better Government Services. Aadhaar authentication has improved the delivery of government schemes like Direct Benefit Transfers (DBTs), Public Distribution System (PDS), and pensions, ensuring transparency and reducing leakages.

The India Stack: A Catalyst for Startup Success

The India Stack is fuelling startup innovation by providing a robust digital infrastructure. It enables entrepreneurs to build services like digital payments, eCommerce, and financial solutions for underserved populations. Platforms such as Aadhaar and UPI have paved the way for businesses to offer secure, seamless transactions, allowing startups like Paytm and BharatPe to thrive. These innovations are driving financial inclusion, empowering rural entrepreneurs, and creating opportunities in sectors like lending and healthtech, supported by global and domestic investments.

From Local Success to Global Inspiration

The impact of the India Stack’s success is being felt worldwide. Global giants such as Google Pay, WhatsApp, and Amazon Pay are drawing inspiration from it to enhance their global payment systems. Alphabet CEO Sundar Pichai plans to apply lessons from Google Pay’s Indian experience to other markets.

While India Stack has achieved significant success, there is still room for improvement. Strengthening data privacy and security is crucial as personal data collection continues to expand. The Digital Personal Data Protection Act aims to address these issues, but balancing innovation with privacy protection remains a challenge.

Bridging the digital divide by expanding Internet access and improving digital literacy, especially for rural and older populations, is key to ensuring that everyone can benefit from the India Stack’s advantages.

Innovation and collaboration are the cornerstones of FinTech success stories. Successful FinTechs have identified market gaps and designed innovative solutions to address these gaps. They have also built an ecosystem of partners – such as other FinTechs, large corporates and financial services organisations – to deliver better customer experiences, create process efficiencies and make compliance easier.

As FinTechs have become mainstream over the years the innovations and the collaborations continue to make technology and business headlines.

Here are some recent trends:

- The Growth of Cross-border Finance. Globalisation and the rise of eCommerce have created a truly global marketplace – and financial agencies such as the MAS and those in the EU are responding to the need.

- Transparency through Smart Contracts. As businesses and platforms scale applications and capabilities through global partnerships, there is a need for trusted, transparent transactions. Symbiont‘s partnership with Swift and BNB Chain‘s tie-up with Google Cloud are some recent examples.

- Evolution of Digital Payments. Digital payments have come a long way from the early days of online banking services and is now set to move beyond digital wallets such as the Open Finance Association and EU initiatives to interlink domestic CBDCs.

- Banks Continue to Innovate. They are responding to market demands and focus on providing their customers with easy, secure, and enhanced experiences. NAB is working on digital identity to reduce fraud, while Standard Chartered Bank is collaborating with Bukalapak to introduce new digital services.

- The Emergence of Embedded Finance. In the future, we will see more instances of embedded financial services within consumer products and services that allows seamless financial transactions throughout customer journeys. LG Electronics‘ new NFT offering is a clear instance.

Read below to find out more.

Download The Future of Finance: FinTech Innovations & Collaborations as a PDF

Recognising FinTechs that are changing lives, creating impact, demonstrating innovation, and building ecosystems to shape the Digital Future.

CATEGORIES:

Global Platform. Organisations that provide a platform to bring together industry stakeholders such as financial services institutions and FinTechs to drive ease of collaboration and innovation by accelerating proof of concept deployments

Financial Inclusion Impact. Organisations that promote financial inclusion in the unbanked and the underbanked with a focus on bridging the economic divide

Sustainable Finance Impact. Organisations that promote sustainable finance and have ESG values

Global Banking. Banks and financial services organisations that embrace digital technology for excellence in customer experience, process efficiency and/or compliance

Global Payments. Innovative use of technology and business models in payment areas

Global Lending. Innovation in alternative finance in areas such as microfinance for individuals and small & medium enterprises, P2P lending and crowdfunding

Customer Experience. Organisations that are driving an exceptional experience for their customers and setting new benchmarks within the industry

Global InsureTech. Excellence and innovation in InsureTech in areas such as micro-insurance, usage-based pricing, process optimisation and underwriting efficiency

To find out about the winners, read on.

To download Ecosystm Red: Global Digital Futures Awards for FinTech Awards Winners as a PDF, please click here.

In the blog, The Top 5 Fintech Trends for 2020, we had spoken about the impact of Fintech on financial inclusion. “Fintech will have a much greater impact than we realise, and we will continue to see it drive the induction of the unbanked into the mainstream economy. The growth in mobile phone penetration, however, continues to grow at a faster pace than banking accessibility across emerging economies. We will continue to see Fintech play a significant role in driving greater inclusion, especially to bring in the underserved in the emerging economies and reducing the gender gap when it comes to adoption of financial services – creating greater inclusion overall.”

Fintech Driving Financial Inclusion in Malaysia

Much of Malaysia’s economy is dependent on foreign workers with an estimate of 3-4 million migrants that roughly contribute to about 30% of the country’s labour force. Instapay, regulated by the Bank Negara Malaysia (BNM), caters to the underbanked community of foreign migrant workers, and recently announced a collaboration with Mastercard, to provide e-wallet accounts to Malaysian migrant workers. The app supports 9 languages and aims to have 100,000 users in the first year.

The widespread use of e-wallets by the migrant worker community is meant to bring benefits to both them, as well as their employers. It enables employers to use digital technologies for payroll management, reducing their dependence on cash handling, reducing costs and eliminating downtime as their employees no longer need to queue up on paydays.

The Instapay e-wallet also gives a largely underbanked segment of the society access to affordable financial products and services. The partnership with Mastercard gives Instapay’s customers access to the global network of merchants and ATMs, allowing easier access to financial services.

Ecosystm Principal Advisor, Dheeraj Chowdhry says, “Instapay’s foray into e-wallets furthers and supports the country’s objective of democratising banking and moving to a cashless economy. Collaboration with an international player like Mastercard helps a domestic Fintech to deliver a product that is country agnostic. The migrant worker can not only use the Instapay wallet within Malaysia but also in their home country.”

Malaysia’s Focus on Fintech

The Malaysia Government aims to create a cashless society, lower transaction costs and provide access to the underserved customers. There are two kinds of financial inclusion – for the lower income group as well as for the small and medium enterprises (SMEs) – and Malaysia is committed to both. Digital payments and e-wallets aimed at the lower income group receives an estimated 36% of Fintech funding. The stumbling block is that about a third of the country’s population does not have smartphones, so funds transfer using mobile phone messages is still relevant in the country. Development of the SME sector and eCommerce are twin focus areas for the Digital Economy vision. This provides a ready market for digital payments. Also, while the SME community will still have access to traditional funding, there is expected to be a greater push towards crowdfunding and peer-to-peer financing. It is expected that the share of Fintech funding for alternative funding will grow beyond the estimated 6% that it receives now.

According to a Mastercard Impact Study 2020, Malaysia has the highest e-wallet usage in Southeast Asia. As the country moves towards creating a cashless society, the Government is hoping e-wallet adoption increases. Several initiatives and schemes have been rolled out to promote e-wallets adoption. Last month, Malaysia announced the intention to spend an estimated USD 176 million in 2020 to encourage e-wallet adoption. Earlier this year, the Government announced the e-Tunai Rakyat program to boost the adoption of e-wallets, supported by Grab, Boost and Touch ‘n Go. Chowdhry says, “Instapay e-wallet is yet another manifestation of the amplified focus on e-wallets in Malaysia. BNM has set aside an estimated USD 108 million and has introduced a scheme to give USD $7.25 in credit for every adoption of any of the top 3 e-wallets. This scheme has accelerated e-wallets in the country that has set an adoption target of 15 million i.e. half of its population.”

“This push is backed by a structured approach of increasing the number of small merchants accepting card payments. With BNM’s focus, there are as many as half a million POS terminals out there for both credit cards and QR codes.”

“Malaysia’s regulators have to be applauded for having a well-coordinated, holistic and converging strategy on creating a cashless economy. The issuance, acceptance and regulatory policies have been completely synergised to deliver.”

India has clearly been a target market for Facebook due to the size of the country’s untapped market and the proportion of its younger population. It is estimated that nearly 45% of the population is below 25 years – a prime target for social media and eCommerce platforms. Facebook’s Free Basic program, launched in 2016 to introduce the potential of the Internet to the underprivileged and digitally unskilled, failed primarily because it did not have knowledge of the telecommunications market in India. Facebook returned to the India market the following year, this time in collaboration with Airtel, to launch Express WiFi, aimed at setting up WiFi hotspots to provide internet in public places – again aimed at India’s connectivity issues.

Making its largest foray into the Indian market yet, last week Facebook announced that it is investing US$5.7 billion in Jio Platforms – India’s largest telecom operator – for a 9.9% minority stake. Facebook makes its intentions very clear and is targeting the 60 million small and medium enterprises (SMEs) who can be the backbone of India’s growing digital economy. This includes a rather unorganised retail sector, which has had to adopt digital at breakneck speed following the Government’s earlier financial reforms, which impacted the smaller retailers, dependent primarily on cash transactions. Facebook is by no means the only global giant with an interest in India’s retail business – with Amazon and Walmart leading the way.

The JioMart and WhatsApp Pilot

Just days after the announcement, JioMart – an eCommerce venture also a wholly-owned subsidiary of Reliance Industries, like Jio Platforms – has launched a pilot in Mumbai which allows users to order groceries through WhatsApp. Customers can now place grocery orders through WhatsApp Business with JioMart reaching out to small-scale retailers and brick and mortar stores – or “Kirana stores” as they are referred to in India – to fulfil the order. More than 1,200 local stores have been engaged for this pilot. It currently does not include a digital payment option and invoices and alerts are sent through WhatsApp. Mukesh Ambani, Chairman and MD of Reliance Industries, says that the JioMart and WhatsApp collaboration has the potential to make it possible for around 30 million neighbourhood stores to transact digitally.

India Emerging as the New Battlefield

India is an important eCommerce market for global giants such as Facebook and Amazon, who have struggled with establishing a presence in China. Walmart has also set it its sights on India, with its recent acquisition of Flipkart. Ecosystm Principal Advisor, Kaushik Ghatak says. “India represents the final frontier, where the battle lines are being drawn, and the three are heading towards a collision path. Facebook’s recent move has just upped the game for Amazon and Walmart, as well as for the eCommerce and Fintech start-ups who have been eyeing this market.”

Amazon has been the early mover, establishing its eCommerce presence in India way back in 2013. Ghatak says, “From its initial marketplace approach of curating suppliers to start selling on its platform, Amazon graduated to offering its own delivery and fulfilment services, by establishing dozens of warehouses across India. This was to ensure the quality and timeliness of deliveries, upholding its ‘Fulfilment by Amazon’ (FBA) brand promise. There was a considerable cost though, in terms of time to ramp up and investments – with the associated asset risks. Also, reaching out to the diffused retail sector, with their non-existent or very low level of digitalisation, has been difficult for all the major eCommerce players such as Amazon and Flipkart. Jeff Bezos’ announcement of an additional investment of $ 1 billion, earlier this year, to digitise SMEs, allowing them to sell and operate online, is a step to extend its reach into this diffused retail market.”

JioMart’s model, according to Ghatak is in stark contrast to Amazon’s. “JioMart’s currently ongoing pilot in Mumbai is a classic B2C marketplace model, with little or no asset risk. The orders placed by the customers are routed to the nearest Kirana store based on stock availability, with the customers going to pick up the ordered items themselves at times.”

Ecosystm Principal Advisor, Niloy Mukherjee says, “Jio has unparalleled market access in India with reports showing north of 370 million subscribers. Even at a $1.7 per month revenue from such a huge number, one can get to a $7.5 billion-dollar annual business. But even this is dwarfed by what that subscriber base itself is worth – through the data it provides, the products that can be sold and so on. Similarly, WhatsApp will prove to be more important than Facebook in India, with more than 400 million users. Using WhatsApp to get Kirana stores to do delivery can be a true game-changer.”

Talking about how this competes with Amazon, Mukherjee says, “This can eat into the business of an Amazon and my guess is, it will be far more efficient. The proximity to the customer will allow multiple deliveries per day at short notice, and fresh produce guarantees – maybe even door returns if not satisfied – that would be hard to match. Given the traffic situation in large Indian cities, delivery logistics from a more distant source will always struggle to compete. This is one tip of a multi-pronged spear – there are obviously other products that can be contemplated, leading to additional revenues.”

The Possibilities Ahead

Mukherjee explains why he thinks Facebook invested in Jio Platforms, rather than just forging a collaboration model. “Clearly both parties want to tie the other down and make sure that this alliance is long term. And this possibly means revenue will be shared instead of the usual commission model. Also, the go-to-market implications can run to more than just the Indian market. WeChat Pay is huge in China but not really elsewhere. If this works, there could be a potential “WhatsApp Pay” in the rest of the world. For Jio who already dominates the telecom landscape in India, this deal is a step towards taking their earnings to a new level, above the top end of the telecom category – they can access profit pools available to hardly any telecom provider worldwide.”

At a time when a market entry for foreign players in India is getting tougher with increasing regulatory pressures, a tie-up with the biggest player in India is indeed a very promising step – for both Facebook and Reliance. “For Facebook, this is a great opportunity to take its dependence away from a primarily ad-driven revenue model. The digitalisation of the diffused retail sector in India will open up new revenue opportunities from its WhatsApp Business App, WhatsApp Business API, and WhatsApp Pay-UPI gateway (pending regulatory approval). There is a potential of revenues from a variety of marketing services, membership fees, customer management services, product sales, commissions on transactions, and software service fees,” says Ghatak.

Talking about the potential for Reliance Industries, Ghatak says, “The technology horsepower of Facebook will help propel them ahead of Fintech and eCommerce companies in India – challenging already established players such as Amazon and Flipkart, and the newbie start-ups. Ability to drive transactions and digital payments in the diffused retail sector will open up huge revenue opportunities that were largely untapped until now, with low asset risks. Also, this sector has traditionally operated on a cash-based model and the recent COVID-19 crisis has exposed how vulnerable the sector is with a limited view of the supply chain, and limited funding for working capital. Developing relationships with the millions of Kirana stores spread across India also gives the opportunity of revenue generation through supply chain financing – a largely ignored sub-sector until now.”

Mukherjee thinks that this alliance will challenge players such as Amazon and Amazon Pay, Google Pay and PayTM. Ghatak also thinks that eventually, Jio Platform will have to either choose between or integrate the best features of WhatsApp Pay and the Jio Money Merchant payment gateways.

However, Ghatak offers a word of caution on the downside risks as well. “Partnering with Facebook is a hugely ambitious game plan for Reliance Industries. The success of its plans will also depend on how well it is able to curate the suppliers who are responsible for the actual delivery. In a consumer-driven business model, trust and customer experience cannot be compromised. The low asset, high leverage and high reach model can unravel itself if the customer gets the short end of the stick, in this rush for eCommerce domination.”