Ecosystm research shows low GenAI adoption in Indonesia, with 83% of organisations hesitant due to governance or language barriers.

Learn about the key trends transforming the Indonesian technology landscape and watch this space for more data-backed insights on Southeast Asia’s tech markets.

To mitigate the challenges of cloud vendor lock-in, 44% of organisations in Thailand will prioritise data centre consolidation and infrastructure modernisation in 2024.

Explore the key trends impacting Thailand’s technology adoption. Keep an eye out for more data-backed insights on tech markets across Southeast Asia.

ASEAN, poised to become the world’s 4th largest economy by 2030, is experiencing a digital boom. With an estimated 125,000 new internet users joining daily, it is the fastest-growing digital market globally. These users are not just browsing, but are actively engaged in data-intensive activities like gaming, eCommerce, and mobile business. As a result, monthly data usage is projected to soar from 9.2 GB per user in 2020 to 28.9 GB per user by 2025, according to the World Economic Forum. Businesses and governments are further fuelling this transformation by embracing Cloud, AI, and digitisation.

Investments in data centre capacity across Southeast Asia are estimated to grow at a staggering pace to meet this growing demand for data. While large hyperscale facilities are currently handling much of the data needs, edge computing – a distributed model placing data centres closer to users – is fast becoming crucial in supporting tomorrow’s low-latency applications and services.

The Big & the Small: The Evolving Data Centre Landscape

As technology pushes boundaries with applications like augmented reality, telesurgery, and autonomous vehicles, the demand for ultra-low latency response times is skyrocketing. Consider driverless cars, which generate a staggering 5 TB of data per hour and rely heavily on real-time processing for split-second decisions. This is where edge data centres come in. Unlike hyperscale data centres, edge data centres are strategically positioned closer to users and devices, minimising data travel distances and enabling near-instantaneous responses; and are typically smaller with a capacity ranging from 500 KW to 2 MW. In comparison, large data centres have a capacity of more than 80MW.

While edge data centres are gaining traction, cloud-based hyperscalers such as AWS, Microsoft Azure, and Google Cloud remain a dominant force in the Southeast Asian data centre landscape. These facilities require substantial capital investment – for instance, it took almost USD 1 billion to build Meta’s 150 MW hyperscale facility in Singapore – but offer immense processing power and scalability. While hyperscalers have the resources to build their own data centres in edge locations or emerging markets, they often opt for colocation facilities to familiarise themselves with local markets, build out operations, and take a “wait and see” approach before committing significant investments in the new market.

The growth of data centres in Southeast Asia – whether edge, cloud, hyperscale, or colocation – can be attributed to a range of factors. The region’s rapidly expanding digital economy and increasing internet penetration are the prime reasons behind the demand for data storage and processing capabilities. Additionally, stringent data sovereignty regulations in many Southeast Asian countries require the presence of local data centres to ensure compliance with data protection laws. Indonesia’s Personal Data Protection Law, for instance, allows personal data to be transferred outside of the country only where certain stringent security measures are fulfilled. Finally, the rising adoption of cloud services is also fuelling the need for onshore data centres to support cloud infrastructure and services.

Notable Regional Data Centre Hubs

Singapore. Singapore imposed a moratorium on new data centre developments between 2019 to 2022 due to concerns over energy consumption and sustainability. However, the city-state has recently relaxed this ban and announced a pilot scheme allowing companies to bid for permission to develop new facilities.

In 2023, the Singapore Economic Development Board (EDB) and the Infocomm Media Development Authority (IMDA) provisionally awarded around 80 MW of new capacity to four data centre operators: Equinix, GDS, Microsoft, and a consortium of AirTrunk and ByteDance (TikTok’s parent company). Singapore boasts a formidable digital infrastructure with 100 data centres, 1,195 cloud service providers, and 22 network fabrics. Its robust network, supported by 24 submarine cables, has made it a global cloud connectivity leader, hosting major players like AWS, Azure, IBM Softlayer, and Google Cloud.

Aware of the high energy consumption of data centres, Singapore has taken a proactive stance towards green data centre practices. A collaborative effort between the IMDA, government agencies, and industries led to the development of a “Green Data Centre Standard“. This framework guides organisations in improving data centre energy efficiency, leveraging the established ISO 50001 standard with customisations for Singapore’s context. The standard defines key performance metrics for tracking progress and includes best practices for design and operation. By prioritising green data centres, Singapore strives to reconcile its digital ambitions with environmental responsibility, solidifying its position as a leading Asian data centre hub.

Malaysia. Initiatives like MyGovCloud and the Digital Economy Blueprint are driving Malaysia’s public sector towards cloud-based solutions, aiming for 80% use of cloud storage. Tenaga Nasional Berhad also established a “green lane” for data centres, solidifying Malaysia’s commitment to environmentally responsible solutions and streamlined operations. Some of the big companies already operating include NTT Data Centers, Bridge Data Centers and Equinix.

The district of Kulai in Johor has emerged as a hotspot for data centre activity, attracting major players like Nvidia and AirTrunk. Conditional approvals have been granted to industry giants like AWS, Microsoft, Google, and Telekom Malaysia to build hyperscale data centres, aimed at making the country a leading hub for cloud services in the region. AWS also announced a new AWS Region in the country that will meet the high demand for cloud services in Malaysia.

Indonesia. With over 200 million internet users, Indonesia boasts one of the world’s largest online populations. This expanding internet economy is leading to a spike in the demand for data centre services. The Indonesian government has also implemented policies, including tax incentives and a national data centre roadmap, to stimulate growth in this sector.

Microsoft, for instance, is set to open its first regional data centre in Thailand and has also announced plans to invest USD 1.7 billion in cloud and AI infrastructure in Indonesia. The government also plans to operate 40 MW of national data centres across West Java, Batam, East Kalimantan, and East Nusa Tenggara by 2026.

Thailand. Remote work and increasing online services have led to a data centre boom, with major industry players racing to meet Thailand’s soaring data demands.

In 2021, Singapore’s ST Telemedia Global Data Centres launched its first 20 MW hyperscale facility in Bangkok. Soon after, AWS announced a USD 5 billion investment plan to bolster its cloud capacity in Thailand and the region over the next 15 years. Heavyweights like TCC Technology Group, CAT Telecom, and True Internet Data Centre are also fortifying their data centre footprints to capitalise on this explosive growth. Microsoft is also set to open its first regional data centre in the country.

Conclusion

Southeast Asia’s booming data centre market presents a goldmine of opportunity for tech investment and innovation. However, navigating this lucrative landscape requires careful consideration of legal hurdles. Data protection regulations, cross-border data transfer restrictions, and local policies all pose challenges for investors. Beyond legal complexities, infrastructure development needs and investment considerations must also be addressed. Despite these challenges, the potential rewards for companies that can navigate them are substantial.

In today’s competitive business landscape, delivering exceptional customer experiences is crucial to winning new clients and fostering long-lasting customer loyalty. Research has shown that poor customer service can cost businesses around USD 75 billion in a year and that 1 in 3 customers is likely to abandon a brand after a single negative experience. Organisations excelling at personalised customer interactions across channels have a significant market edge.

In a recent webinar with Shivram Chandrasekhar, Solutions Architect at Twilio, we delved into strategies for creating this edge. How can contact centres optimise interactions to boost cost efficiency and customer satisfaction? We discussed the pivotal role of voice in providing personalised customer experiences, the importance of balancing AI and human interaction for enhanced satisfaction, and the operational advantages of voice intelligence in streamlining operations and improving agent efficiency.

The Voice Advantage

Despite the rise of digital channels, voice interactions remain crucial for organisations seeking to deliver exceptional customer experiences. Voice calls offer nuanced insights and strategic advantages, allowing businesses to address issues effectively and proactively meet customer needs, fostering loyalty and driving growth.

There are multiple reasons why voice will remain relevant including:

- In many countries it is mandatory in several industries such as Financial Services, Healthcare, & Government & Emergency Services.

- There are customers who simply favour it over other channels – the human touch is important to them.

- It proves to be the most effective when it comes to handling complex and recurrent issues, including facilitating effective negotiations and better sales closures; Digital and AI channels cannot do it alone yet.

- Analysing voice data reveals valuable patterns and customer sentiments, aiding in pinpointing areas for improvement. Unlike static metrics, voice data offers dynamic feedback, helping in proactive strategies and personalised opportunities.

AI vs the Human Agent

There has been a growing trend towards ‘agentless contact centres’, where businesses aim to pivot away from human agents – but there has also been increasing customer dissatisfaction with purely automated interactions. A balanced approach that empowers human agents with AI-driven insights and conversational AI can yield better results. In fact, the conversation should not be about one or the other, but rather about a combination of an AI + Human Agent.

Where organisations rely on conversational AI, there must be a seamless transitioning between automated and live agent interactions, maintaining a cohesive customer experience. Ultimately, the goal should be to avoid disruptions to customer journeys and ensure a smooth, integrated approach to customer engagement across different channels.

Exploring AI Opportunities in Voice Interactions

Contact centres in Asia Pacific are looking to deploy AI capabilities to enhance both employee and customer experiences.

Using predictive AI algorithms on customer data helps organisations forecast market trends and optimise resource allocation. Additionally, AI-driven identity validation swiftly confirms customer identities, mitigating fraud risks. By automating transactional tasks, particularly FAQs, contact centre operations are streamlined, ensuring that critical calls receive prompt attention. AI-powered quality assurance processes provide insights into all voice calls, facilitating continuous improvement, while AI-driven IVR systems enhance the customer experience by simplifying menu navigation.

Agent Assist solutions, integrated with GenAI, offer real-time insights before customer interactions, streamlining service delivery and saving valuable time. These solutions automate mundane tasks like call summaries, enabling agents to focus on high-value activities such as sales collaboration, proactive feedback management, and personalised outbound calls.

Actionable Data

Organisations possess a wealth of customer data from various touchpoints, including voice interactions. Accessing real-time, accurate data is essential for effective customer and agent engagement. Advanced analytics techniques can uncover hidden patterns and correlations, informing product development, marketing strategies, and operational improvements. However, organisations often face challenges with data silos and lack of interconnected data, hindering omnichannel experiences.

Integrating customer data with other organisational sources provides a holistic view of the customer journey, enabling personalised experiences and proactive problem-solving. A Customer Data Platform (CDP) breaks down data silos, providing insights to personalise interactions, address real-time issues, identify compliance gaps, and exceed customer expectations throughout their journeys.

Considerations for AI Transformation in Contact Centres

- Prioritise the availability of live agents and voice channels within Conversational AI deployments to prevent potential issues and ensure immediate human assistance when needed.

- Listen extensively to call recordings to ensure AI solutions sound authentic and emulate human conversations to enhance user adoption.

- Start with data you can trust – the quality of data fed into AI systems significantly impacts their effectiveness.

- Test continually during the solution testing phase for seamless orchestration across all communication channels and to ensure the right guardrails to manage risks effectively.

- Above all, re-think every aspect of your CX strategy – the engagement channels, agent roles, and contact centres – through an AI lens.

Ecosystm research shows that customer engagement is emerging as the main beneficiary of AI implementations in Malaysia with 44% of AI investments being led by CX/Marketing/Sales teams.

Explore the key trends that are transforming the Malaysian technology landscape and stay tuned for more data-backed insights on Southeast Asia’s tech markets.

In my last Ecosystm Insight, I spoke about the importance of data architecture in defining the data flow, data management systems required, the data processing operations, and AI applications. Data Mesh and Data Fabric are both modern architectural approaches designed to address the complexities of managing and accessing data across a large organisation. While they share some commonalities, such as improving data accessibility and governance, they differ significantly in their methodologies and focal points.

Data Mesh

- Philosophy and Focus. Data Mesh is primarily focused on the organisational and architectural approach to decentralise data ownership and governance. It treats data as a product, emphasising the importance of domain-oriented decentralised data ownership and architecture. The core principles of Data Mesh include domain-oriented decentralised data ownership, data as a product, self-serve data infrastructure as a platform, and federated computational governance.

- Implementation. In a Data Mesh, data is managed and owned by domain-specific teams who are responsible for their data products from end to end. This includes ensuring data quality, accessibility, and security. The aim is to enable these teams to provide and consume data as products, improving agility and innovation.

- Use Cases. Data Mesh is particularly effective in large, complex organisations with many independent teams and departments. It’s beneficial when there’s a need for agility and rapid innovation within specific domains or when the centralisation of data management has become a bottleneck.

Data Fabric

- Philosophy and Focus. Data Fabric focuses on creating a unified, integrated layer of data and connectivity across an organisation. It leverages metadata, advanced analytics, and AI to improve data discovery, governance, and integration. Data Fabric aims to provide a comprehensive and coherent data environment that supports a wide range of data management tasks across various platforms and locations.

- Implementation. Data Fabric typically uses advanced tools to automate data discovery, governance, and integration tasks. It creates a seamless environment where data can be easily accessed and shared, regardless of where it resides or what format it is in. This approach relies heavily on metadata to enable intelligent and automated data management practices.

- Use Cases. Data Fabric is ideal for organisations that need to manage large volumes of data across multiple systems and platforms. It is particularly useful for enhancing data accessibility, reducing integration complexity, and supporting data governance at scale. Data Fabric can benefit environments where there’s a need for real-time data access and analysis across diverse data sources.

Both approaches aim to overcome the challenges of data silos and improve data accessibility, but they do so through different methodologies and with different priorities.

Data Mesh and Data Fabric Vendors

The concepts of Data Mesh and Data Fabric are supported by various vendors, each offering tools and platforms designed to facilitate the implementation of these architectures. Here’s an overview of some key players in both spaces:

Data Mesh Vendors

Data Mesh is more of a conceptual approach than a product-specific solution, focusing on organisational structure and data decentralisation. However, several vendors offer tools and platforms that support the principles of Data Mesh, such as domain-driven design, product thinking for data, and self-serve data infrastructure:

- Thoughtworks. As the originator of the Data Mesh concept, Thoughtworks provides consultancy and implementation services to help organisations adopt Data Mesh principles.

- Starburst. Starburst offers a distributed SQL query engine (Starburst Galaxy) that allows querying data across various sources, aligning with the Data Mesh principle of domain-oriented, decentralised data ownership.

- Databricks. Databricks provides a unified analytics platform that supports collaborative data science and analytics, which can be leveraged to build domain-oriented data products in a Data Mesh architecture.

- Snowflake. With its Data Cloud, Snowflake facilitates data sharing and collaboration across organisational boundaries, supporting the Data Mesh approach to data product thinking.

- Collibra. Collibra provides a data intelligence cloud that offers data governance, cataloguing, and privacy management tools essential for the Data Mesh approach. By enabling better data discovery, quality, and policy management, Collibra supports the governance aspect of Data Mesh.

Data Fabric Vendors

Data Fabric solutions often come as more integrated products or platforms, focusing on data integration, management, and governance across a diverse set of systems and environments:

- Informatica. The Informatica Intelligent Data Management Cloud includes features for data integration, quality, governance, and metadata management that are core to a Data Fabric strategy.

- Talend. Talend provides data integration and integrity solutions with strong capabilities in real-time data collection and governance, supporting the automated and comprehensive approach of Data Fabric.

- IBM. IBM’s watsonx.data is a fully integrated data and AI platform that automates the lifecycle of data across multiple clouds and systems, embodying the Data Fabric approach to making data easily accessible and governed.

- TIBCO. TIBCO offers a range of products, including TIBCO Data Virtualization and TIBCO EBX, that support the creation of a Data Fabric by enabling comprehensive data management, integration, and governance.

- NetApp. NetApp has a suite of cloud data services that provide a simple and consistent way to integrate and deliver data across cloud and on-premises environments. NetApp’s Data Fabric is designed to enhance data control, protection, and freedom.

The choice of vendor or tool for either Data Mesh or Data Fabric should be guided by the specific needs, existing technology stack, and strategic goals of the organisation. Many vendors provide a range of capabilities that can support different aspects of both architectures, and the best solution often involves a combination of tools and platforms. Additionally, the technology landscape is rapidly evolving, so it’s wise to stay updated on the latest offerings and how they align with the organisation’s data strategy.

CX leaders in Australia are actively refining their customer and employee strategies. Due to high contact centre operational costs, outsourcing to countries like the Philippines, Fiji, and South Africa has gained popularity. However, compliance issues restrict some organisations from outsourcing. Despite cost constraints, elevating customer experience (CX) through AI, self-service, and digital channels remains crucial. High agent attrition also highlights the need to enhance employee experience (EX).

Meeting these challenges has prompted organisations to assess AI and automation solutions to enhance efficiency, cut costs, and improve EX. Australian CX teams hold extensive data from diverse applications, underscoring the need for a robust data strategy – that can provide deeper insights into customer journeys, proactive service, improved self-service options, and innovative customer engagement.

Here are 5 ways organisations in Australia can achieve their CX objectives.

Download ‘Australian CX Dynamics: Balancing Cost, Compliance, and Employee Experience‘ as a PDF.

#1 Prioritise Omnichannel Orcheshtration

Customers want the flexibility to select a channel that aligns with their preferences – often switching between channels – prompting organisations to offer more engagement channels.

Aim for unified customer context across channels for deeper customer engagement.

Coordinating all channels ensures consistent experiences for customers, with CX teams and agents accessing real-time information across channels. This boosts key metrics like First Call Resolution (FCR) and reduces Average Handle Time (AHT).

It is important not to overlook voice when crafting an omnichannel strategy. Despite digital growth, human interaction remains crucial for complex inquiries and persistent challenges. Context is vital for understanding customer needs, and without it, experiences suffer. This contributes to long waiting times, a common customer complaint in Australia.

#2 Eliminate Data Silos

Despite having access to customer information from multiple interactions, organisations often struggle to construct a comprehensive customer data profile capable of transforming all available data into actionable intelligence.

A Customer Data Platform (CDP) can eliminate data silos and provide actionable insights.

- Identify behavioural trends by understanding patterns to personalise interactions.

- Spot real-time customer issues across channels.

- Uncover compliance gaps and missed sales opportunities from unstructured data.

- Look at customer journeys to proactively address their needs and exceed expectations.

#3 Embed AI into CX Strategies

The emergence of GenAI and Large Language Models (LLMs) has thrust AI into the spotlight, promising to humanise its capabilities. However, there’s untapped potential for AI and automation beyond this.

Australian organisations are primarily considering AI to address key CX priorities: enhancing efficiency, cutting costs, and improving EX.

Agent Assist solutions offer real-time insights before customer interactions, improving CX and saving time. Integrated with GenAI, these solutions automate tasks like call summaries, freeing agents to focus on high-value activities such as sales collaboration, proactive feedback management, personalised outbound calls, and skill development. Predictive AI algorithms go beyond chatbots and Agent Assist solutions, leveraging customer data to forecast trends and optimise resource allocation.

#4 Keep a Firm Eye on Compliance

Compliance in contact centres is more than just a legal requirement; it is core to maintaining customer trust and safeguarding brand’s reputation.

Maintaining compliance in contact centres is challenging due to factors such as the need to follow different industry guidelines, constantly changing regulatory environment, and the shift to hybrid work.

Organisations should focus on:

- Limiting individual stored data

- Segregating data from core business applications

- Encrypting sensitive customer data

- Employing access controls

- Using multi-factor authentication and single sign-on systems

- Updating security protocols consistently

- Providing ongoing training to agents

#5 Implement New Technologies with Ease

Organisations often struggle to modernise legacy systems and integrate newer technologies, hindering CX transformation.

Delivering CX transformation while managing multiple disparate systems requires a platform that can integrate desired capabilities for holistic CX and EX experiences.

A unified platform streamlines application management, ensuring cohesion, unified KPIs, enhanced security, simplified maintenance, and single sign-on for agents. This approach offers consistent experiences across channels and early issue detection, eliminating the need to navigate multiple applications or projects.

Capabilities that a platform should have:

- Programmable APIs to deliver messages across preferred social and messaging channels.

- Modernisation of outdated IVRs with self-service automation.

- Transformation of static mobile apps into engaging experience tools.

- Fraud prevention across channels through immediate phone number verification APIs.

Ecosystm Opinion

Organisations in Australia must pivot to meet customers on their terms, and it will require a comprehensive re-evaluation of their CX strategy.

This includes transforming the contact centre into an “Intelligent” Data Hub, leveraging intelligent APIs for seamless customer interaction management; evolving agents into AI-powered brand ambassadors, armed with real-time insights and decision-making capabilities; and redesigning channels and brand experiences for consistency and personalisation, using innovative technologies.

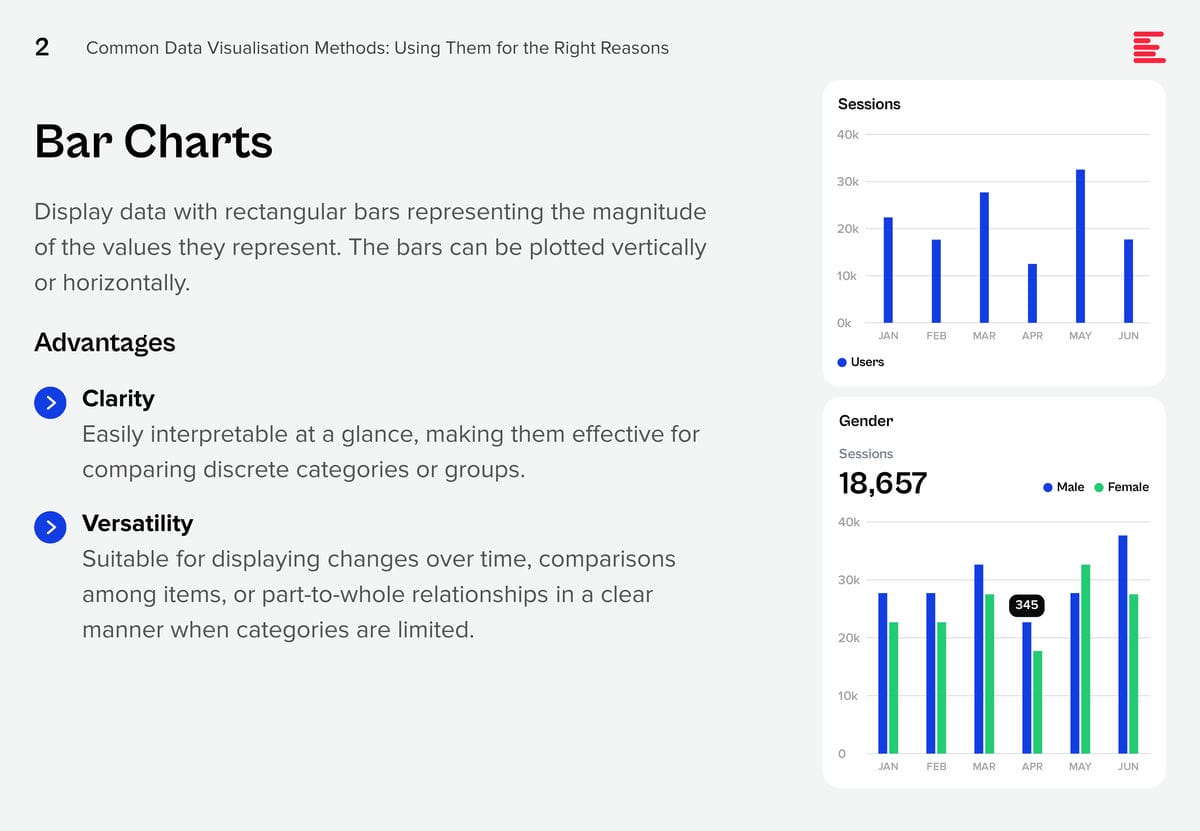

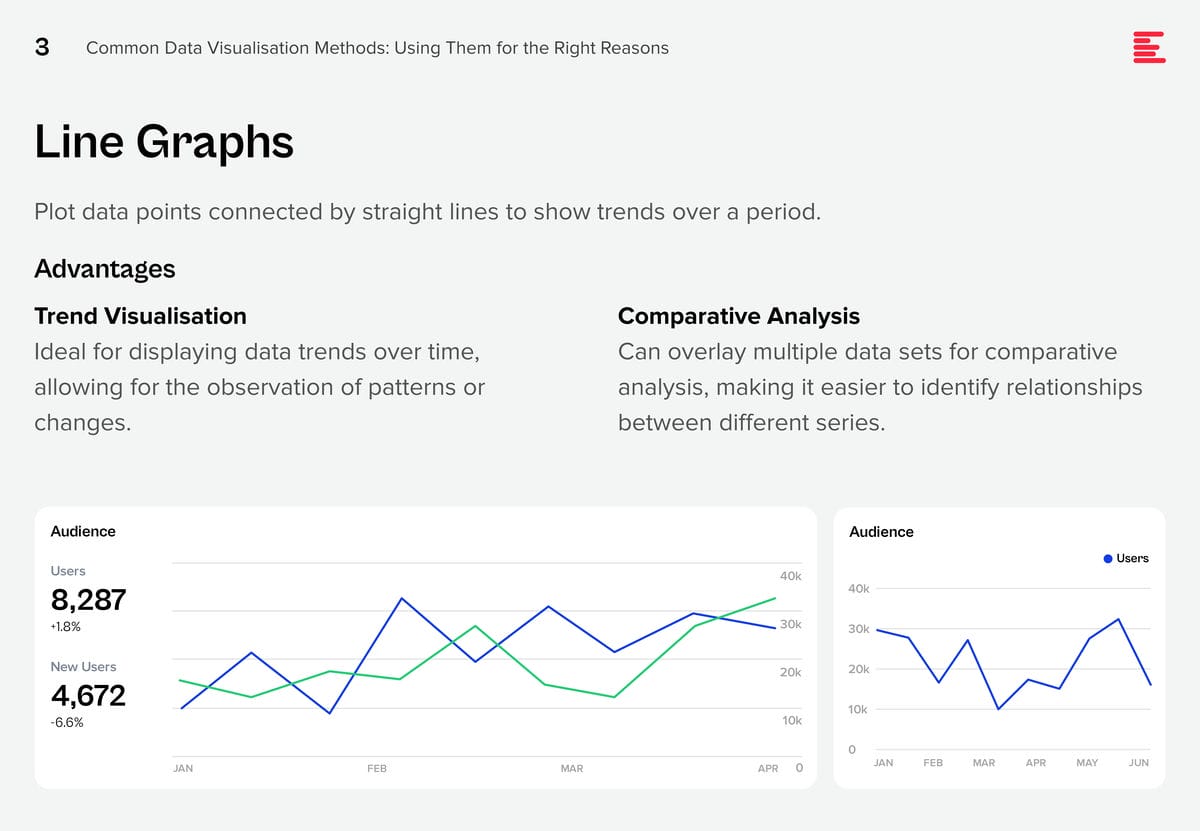

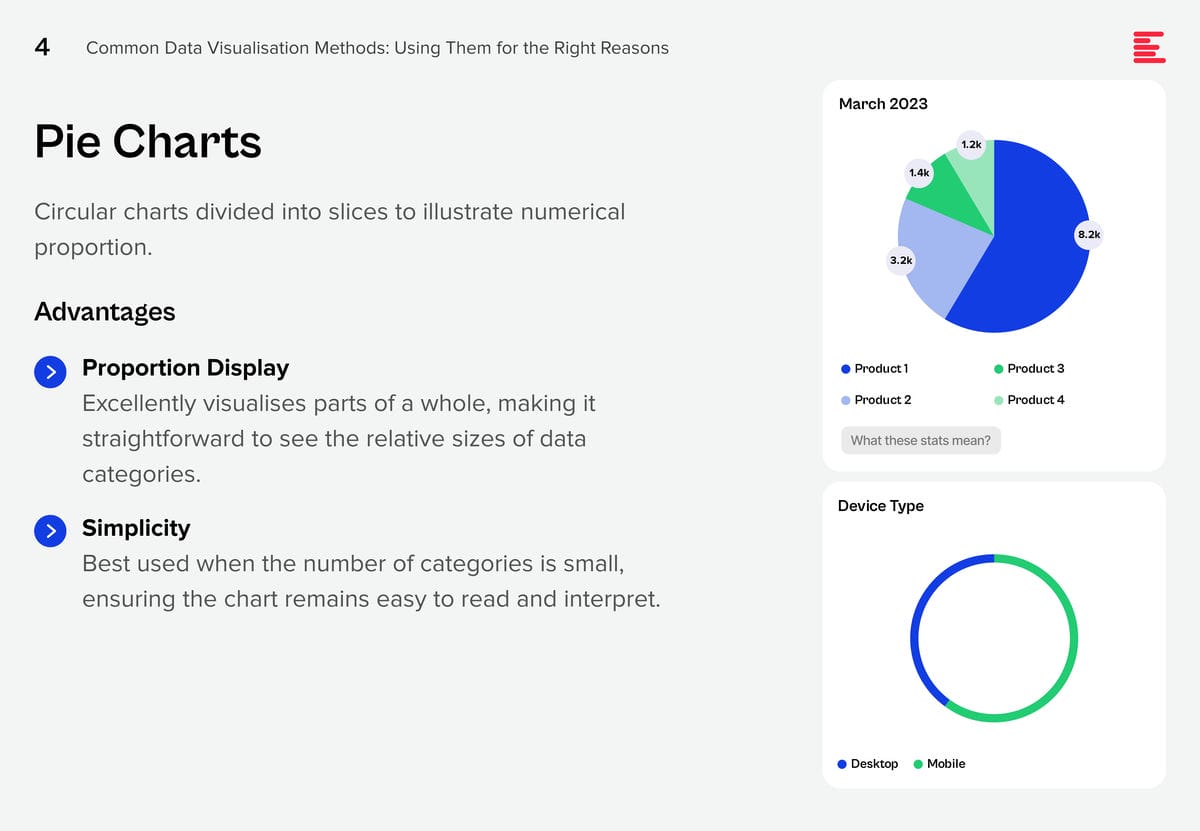

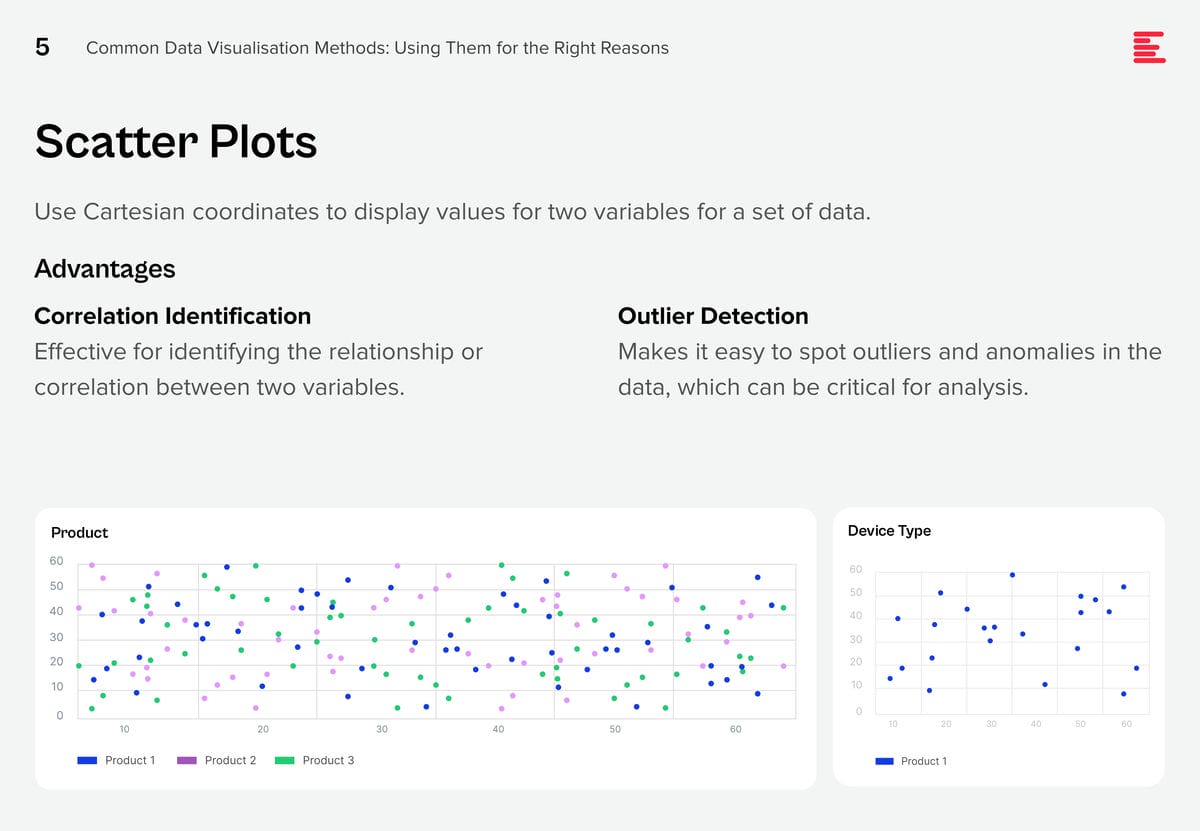

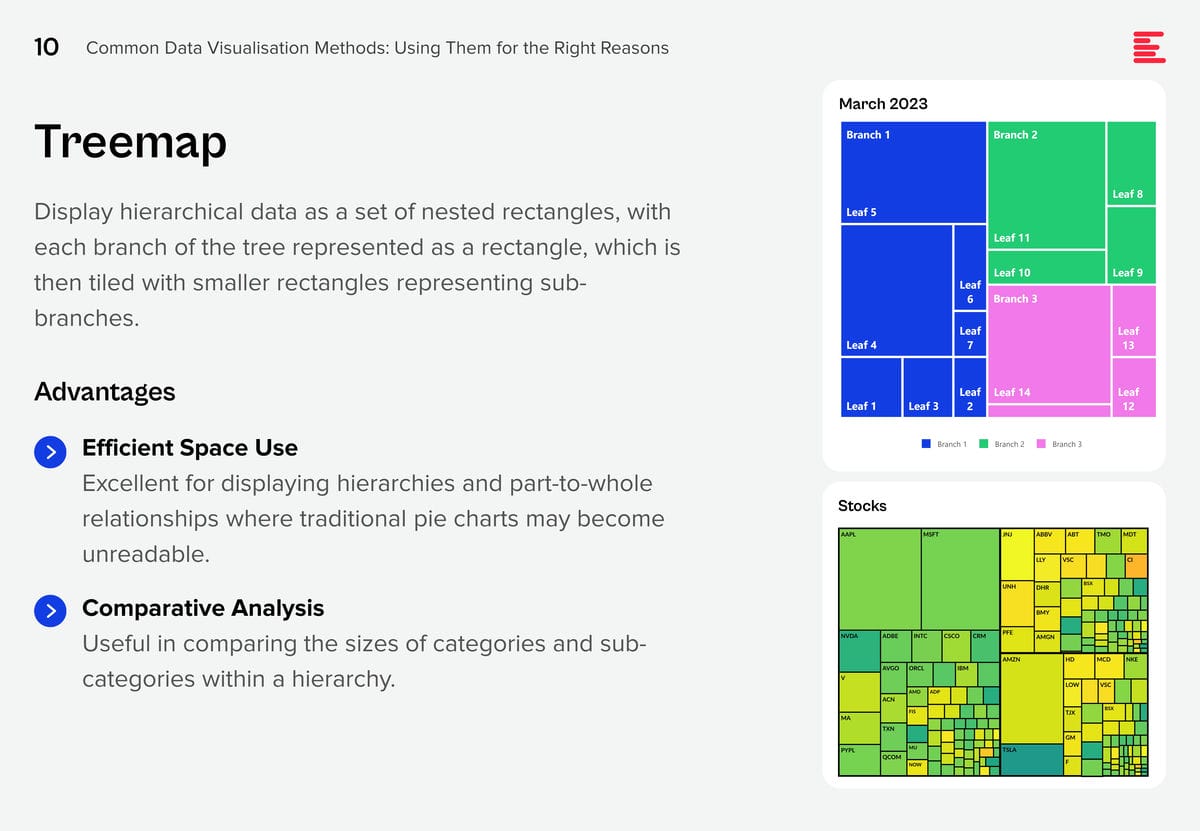

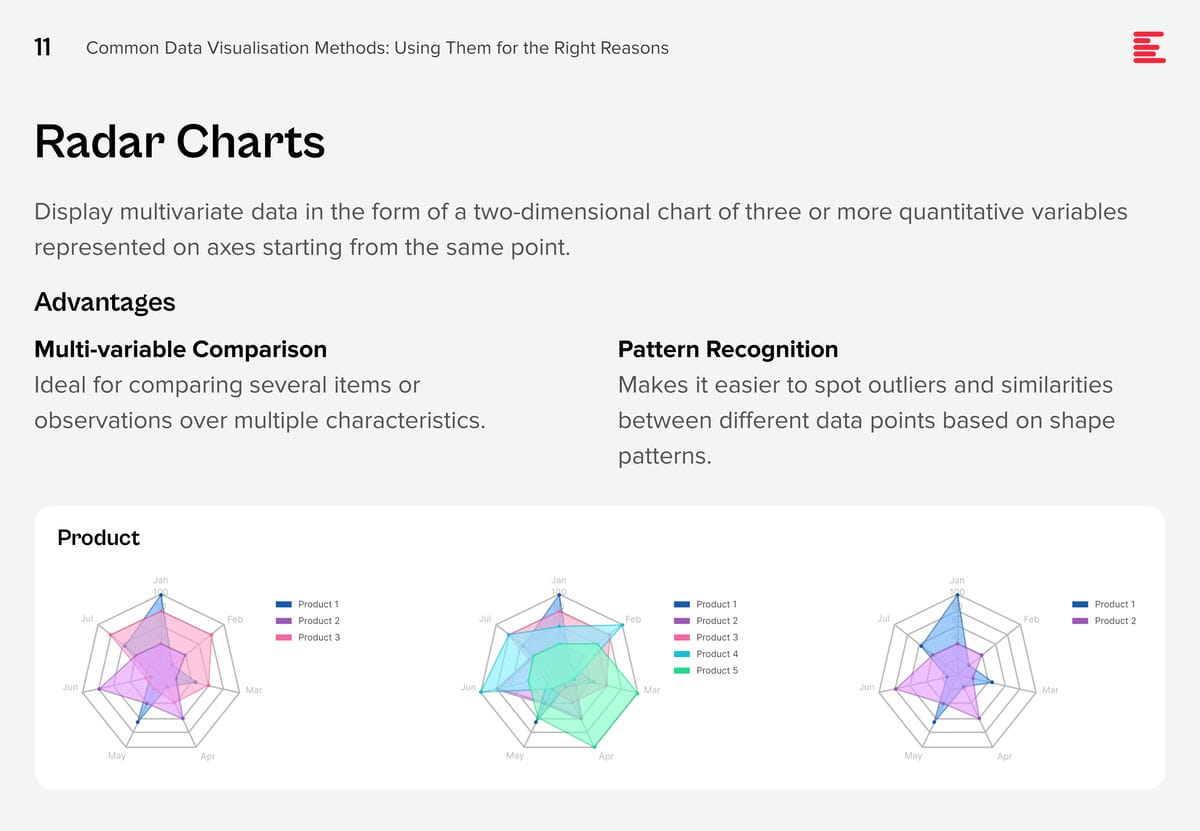

AI systems are creating huge amounts of data at a rapid rate. While this flood of information is extremely valuable, it is also difficult to analyse and understand. Organisations need to make sense of these large data sets to derive useful insights and make better decisions. Data visualisation plays a pivotal role in the interpretation of complex data, making it accessible, understandable, and actionable. Well-designed visualisation can translate complex, high-dimensional data into intuitive, visually appealing representations, helping stakeholders to understand patterns, trends, and anomalies that would otherwise be challenging to recognise.

There are some data visualisation methods that you are using already; and some that you definitely should master as data complexity increases and there is more demand from business teams for better data visualisation.

Download Common Data Visualisation Methods as a PDF

Add These to Your Data Visualisation Repertoire

There are additional visualisation tools that you should be using to tell a better data story. Each of these visualisation techniques serves specific purposes in data analysis, offering unique advantages for representing data insights.

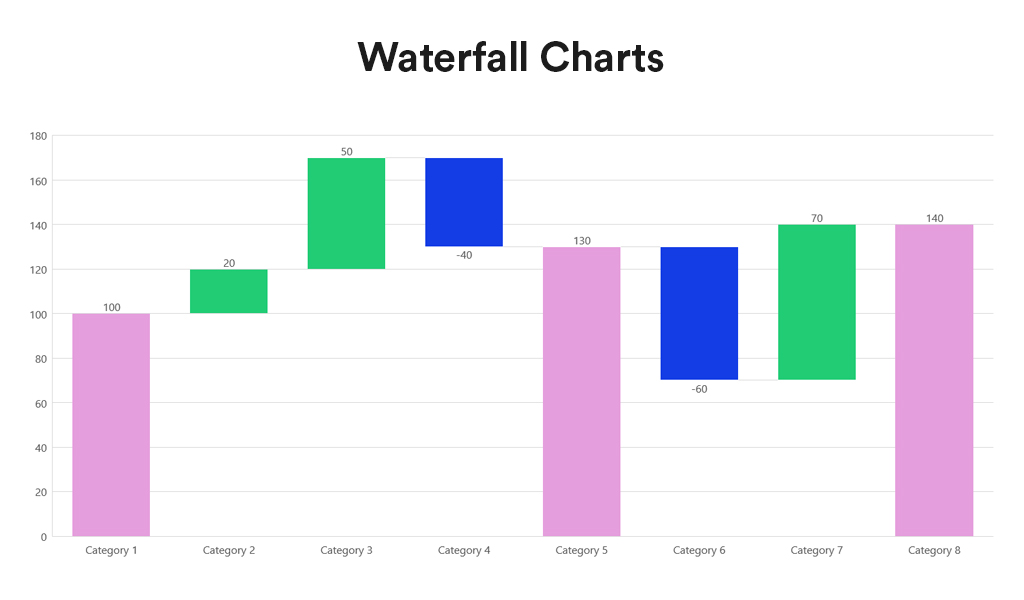

Waterfall charts depict the impact of intermediate positive and negative values on an initial value, often resulting in a final value. They are commonly employed in financial analysis to illustrate the contribution of various factors to a total, making them ideal for visualising step-by-step financial contributions or tracking the cumulative effect of sequentially introduced factors.

Advantages:

- Sequential Analysis. Ideal for understanding the cumulative effect of sequentially introduced positive or negative values.

- Financial Reporting. Commonly used for financial statements to break down the contributions of various elements to a net result, such as revenues, costs, and profits over time.

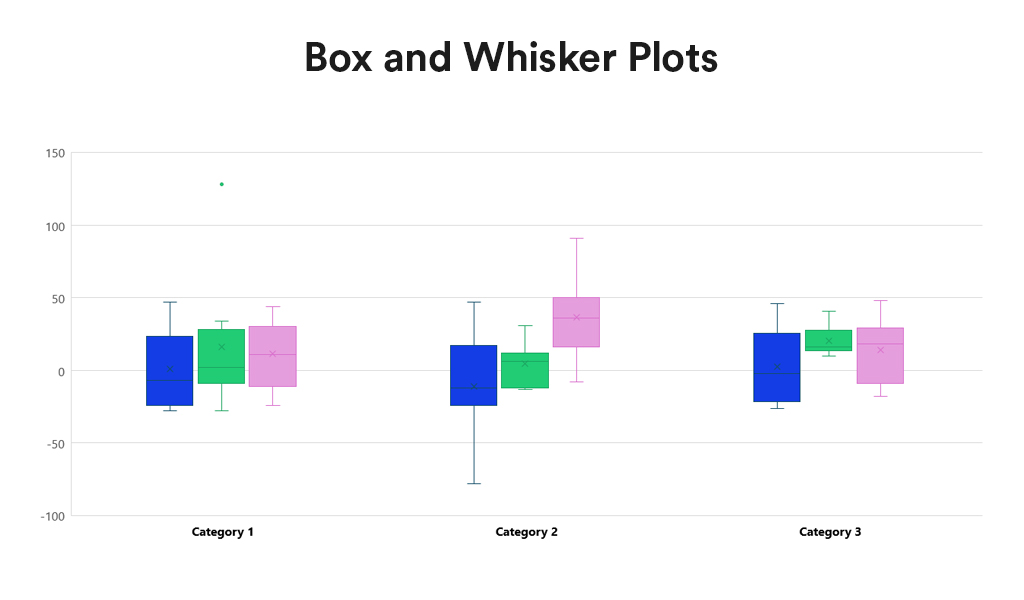

Box and Whisker Plots summarise data distribution using a five-number summary: minimum, first quartile (Q1), median, third quartile (Q3), and maximum. They are valuable for showcasing data sample variations without relying on specific statistical assumptions. Box and Whisker Plots excel in comparing distributions across multiple groups or datasets, providing a concise overview of various statistics.

Advantages:

- Distribution Clarity. Provide a clear view of the data distribution, including its central tendency, variability, and skewness.

- Outlier Identification. Easily identify outliers, offering insights into the spread and symmetry of the data.

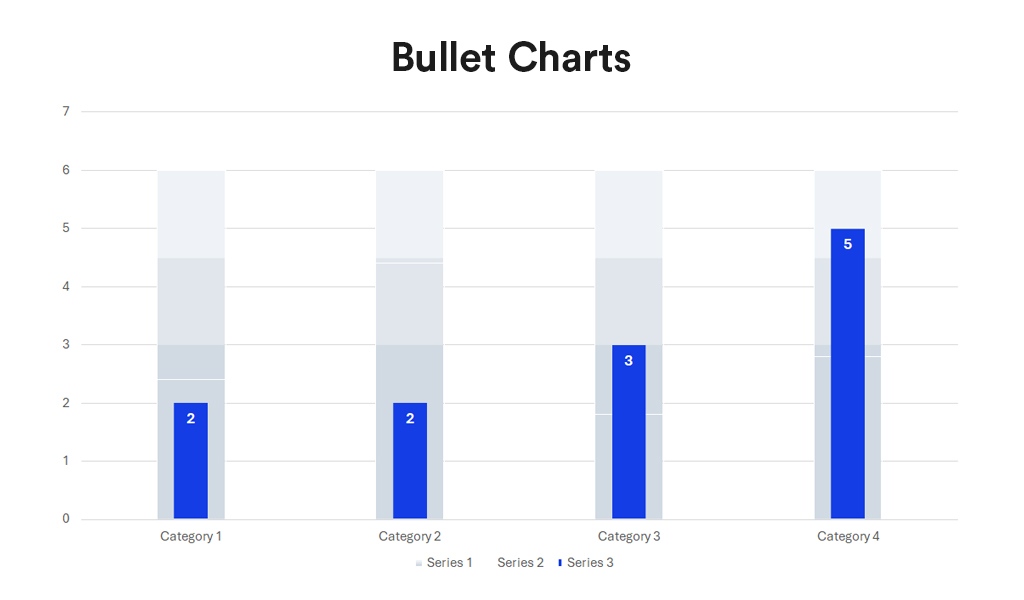

Bullet charts, a bar graph variant, serve as a replacement for dashboard gauges and meters. They showcase a primary measure alongside one or more other measures for context, such as a target or previous period’s performance, often incorporating qualitative ranges like poor, satisfactory, and good. Ideal for performance dashboards with limited space, bullet charts efficiently demonstrate progress towards goals.

Advantages:

- Compactness. Offer a compact and straightforward way to monitor performance against a target.

- Efficiency. More efficient than gauges and meters in dashboard design, as they take up less space and can display more information, making them ideal for comparing multiple measures.

Conclusion

Each data visualisation type has its unique strengths, making it better suited for certain types of data and analysis than others. The key to effective data visualisation lies in matching the visualisation type to your data’s specific needs, considering the story you want, to tell or the insights you aim to glean. Choosing the right data representation helps you to make informed decisions that enhance your data analysis and communication efforts.

Incorporating Waterfall Charts, Box and Whisker Plots, and Bullet Charts into the data visualisation toolkit allows for a broader range of insights to be derived from your data. From analysing financial data, comparing distributions, to tracking performance metrics, these additional types of visualisation can communicate complex data stories clearly and effectively. As with all data visualisation, the key is to choose the type that best matches the organisation’s data story, making it accessible and understandable to the audience.

The White House has mandated federal agencies to conduct risk assessments on AI tools and appoint officers, including Chief Artificial Intelligence Officers (CAIOs), for oversight. This directive, led by the Office of Management and Budget (OMB), aims to modernise government AI adoption and promote responsible use. Agencies must integrate AI oversight into their core functions, ensuring safety, security, and ethical use. CAIOs will be tasked with assessing AI’s impact on civil rights and market competition. Agencies have until December 1, 2024, to address non-compliant AI uses, emphasising swift implementation.

How will this impact global AI adoption? Ecosystm analysts share their views.

Click here to download ‘Ensuring Ethical AI: US Federal Agencies’ New Mandate’ as a PDF.

The Larger Impact: Setting a Global Benchmark

This sets a potential global benchmark for AI governance, with the U.S. leading the way in responsible AI use, inspiring other nations to follow suit. The emphasis on transparency and accountability could boost public trust in AI applications worldwide.

The appointment of CAIOs across U.S. federal agencies marks a significant shift towards ethical AI development and application. Through mandated risk management practices, such as independent evaluations and real-world testing, the government recognises AI’s profound impact on rights, safety, and societal norms.

This isn’t merely a regulatory action; it’s a foundational shift towards embedding ethical and responsible AI at the heart of government operations. The balance struck between fostering innovation and ensuring public safety and rights protection is particularly noteworthy.

This initiative reflects a deep understanding of AI’s dual-edged nature – the potential to significantly benefit society, countered by its risks.

The Larger Impact: Blueprint for Risk Management

In what is likely a world first, AI brings together technology, legal, and policy leaders in a concerted effort to put guardrails around a new technology before a major disaster materialises. These efforts span from technology firms providing a form of legal assurance for use of their products (for example Microsoft’s Customer Copyright Commitment) to parliaments ratifying AI regulatory laws (such as the EU AI Act) to the current directive of installing AI accountability in US federal agencies just in the past few months.

It is universally accepted that AI needs risk management to be responsible and acceptable – installing an accountable C-suite role is another major step of AI risk mitigation.

This is an interesting move for three reasons:

- The balance of innovation versus governance and risk management.

- Accountability mandates for each agency’s use of AI in a public and transparent manner.

- Transparency mandates regarding AI use cases and technologies, including those that may impact safety or rights.

Impact on the Private Sector: Greater Accountability

AI Governance is one of the rare occasions where government action moves faster than private sector. While the immediate pressure is now on US federal agencies (and there are 438 of them) to identify and appoint CAIOs, the announcement sends a clear signal to the private sector.

Following hot on the heels of recent AI legislation steps, it puts AI governance straight into the Boardroom. The air is getting very thin for enterprises still in denial that AI governance has advanced to strategic importance. And unlike the CFC ban in the Eighties (the Montreal protocol likely set the record for concerted global action) this time the technology providers are fully onboard.

There’s no excuse for delaying the acceleration of AI governance and establishing accountability for AI within organisations.

Impact on Tech Providers: More Engagement Opportunities

Technology vendors are poised to benefit from the medium to long-term acceleration of AI investment, especially those based in the U.S., given government agencies’ preferences for local sourcing.

In the short term, our advice to technology vendors and service partners is to actively engage with CAIOs in client agencies to identify existing AI usage in their tools and platforms, as well as algorithms implemented by consultants and service partners.

Once AI guardrails are established within agencies, tech providers and service partners can expedite investments by determining which of their platforms, tools, or capabilities comply with specific guardrails and which do not.

Impact on SE Asia: Promoting a Digital Innovation Hub

By 2030, Southeast Asia is poised to emerge as the world’s fourth-largest economy – much of that growth will be propelled by the adoption of AI and other emerging technologies.

The projected economic growth presents both challenges and opportunities, emphasizing the urgency for regional nations to enhance their AI governance frameworks and stay competitive with international standards. This initiative highlights the critical role of AI integration for private sector businesses in Southeast Asia, urging organizations to proactively address AI’s regulatory and ethical complexities. Furthermore, it has the potential to stimulate cross-border collaborations in AI governance and innovation, bridging the U.S., Southeast Asian nations, and the private sector.

It underscores the global interconnectedness of AI policy and its impact on regional economies and business practices.

By leading with a strategic approach to AI, the U.S. sets an example for Southeast Asia and the global business community to reevaluate their AI strategies, fostering a more unified and responsible global AI ecosystem.

The Risks

U.S. government agencies face the challenge of sourcing experts in technology, legal frameworks, risk management, privacy regulations, civil rights, and security, while also identifying ongoing AI initiatives. Establishing a unified definition of AI and cataloguing processes involving ML, algorithms, or GenAI is essential, given AI’s integral role in organisational processes over the past two decades.

However, there’s a risk that focusing on AI governance may hinder adoption.

The role should prioritise establishing AI guardrails to expedite compliant initiatives while flagging those needing oversight. While these guardrails will facilitate “safe AI” investments, the documentation process could potentially delay progress.

The initiative also echoes a 20th-century mindset for a 21st-century dilemma. Hiring leaders and forming teams feel like a traditional approach. Today, organisations can increase productivity by considering AI and automation as initial solutions. Investing more time upfront to discover initiatives, set guardrails, and implement AI decision-making processes could significantly improve CAIO effectiveness from the outset.