Organisations are increasingly investing in digital. However, they are at different stages of their digital maturity. Some companies are in the early transitional stages while others are investing to upgrade capabilities they instituted long ago. An understanding of the digital maturity of a typical organisation in your market/industry can help you benchmark your technology and. digital roadmap.

This ebook presents some key findings for financial services within Indonesia. You will get insights on impact of COVID-19 on transformation journeys, key business priorities for 2021, and the shift in engagement strategies and channels.

Click below to download the eBook

(Clicking on this link will take you to Sitecore website where you can download the eBook)

Digital and IT organisations are going through some dramatic changes as they adopt cloud and as-a-service capabilities. In this post, I want to write about two of these – one that is very much a consequence of the other.

Contract Numbers are Exploding

We’re seeing an explosion in the number of IT suppliers to a typical organisation.

Pre-cloud, the typical organisation probably had five to ten contracts that covered most of the external services that were in use. With suppliers increasingly providing niche functionality and the increased use of credit cards to buy external services, it is often difficult to determine exactly how many contracts are in place. Or, indeed, have a clear understanding of the terms and conditions of each of these contracts.

Where once an organisation might have had contracts for an on-premises ERP and CRM system, a typical organisation will still have those contracts as well as a supply chain forecasting service, a marketing email management tool, not to mention online spreadsheets and task management capabilities.

So with many more contracts in place, the complexity of managing these contracts and understanding the technical, legal and business risks encapsulated in these contracts has become dramatically more difficult.

I’ll return to this point in a later post, as most organisations struggle with this increasing complexity.

What Is Happening to Your People?

The existence of these contracts means that you are increasingly becoming dependent on the people employed by these external organisations. But when you sign up for these contracts, do you investigate how these suppliers develop their talent?

The New Zealand Herald recently carried an interesting article on one organisation that has developed a paid intern program. Something very rare in the industry.

The article prompted me to think through some of the implications of using cloud services. Tech buyer organisations will have less need for technical capabilities as increasingly these are delivered by the cloud suppliers.

But the growth in demand for digital and IT skills just continues to increase as more and more industries digitalise. In the past, tech buyer organisations would have invested (at least the good employers did!) in the development of their people. The cloud suppliers are increasingly doing this talent development.

Most contract negotiations are based on cost, quality and customer service. A significant proportion of cloud contracts are now boilerplate – you pay with a credit card for a monthly service and have little or no ability to negotiate terms and conditions.

The trade-off is required to get a short commitment term and a variable cost profile. No tech vendor can afford to negotiate bespoke contracts for this type of commercial arrangement.

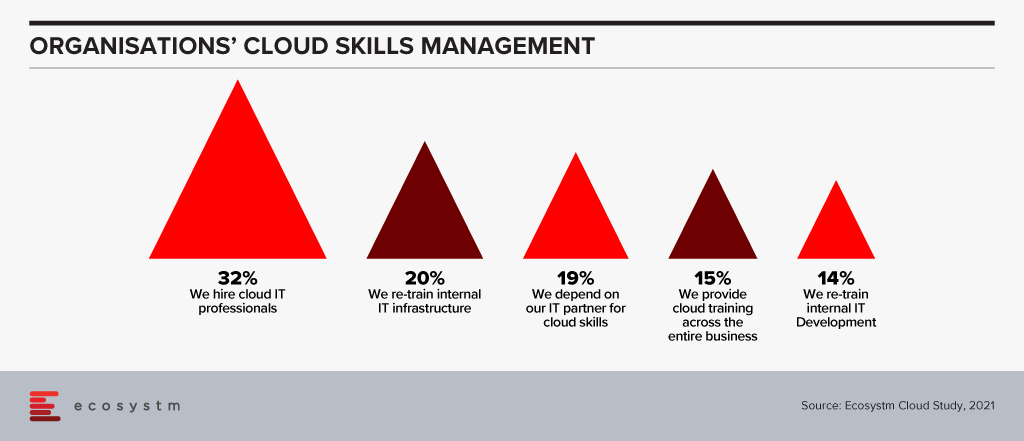

This situation leaves the question of how tech buyers can influence tech vendors to develop their people’s talent appropriately. Some would say that the tech vendors will do this as a matter of course, but the statistics, as highlighted in the Ecosystm research data in Figure 1, show that we are not bringing people in at the rate the industry requires.

Advice for Tech Buyers

I recommend you look closely at using two tactics with the tech vendors that you are working with:

- First, look to consolidate as much workload as practical under a single contract with the supplier. This is not a new recommendation for contracts – but with the increasing use of boilerplate contracts, it is one of the few ways an organisation can increase its value and importance to a tech vendor.

- Second, start finding those tech vendors that are developing new and existing talent in practical ways and favour these organisations in any purchase decision.

Most organisations, individually, do not have the commercial power to dictate terms to the cloud providers. Still, if enough tech buyers adopt this critical criterion, the cloud providers may see the value in investing in the industry’s talent development in meaningful ways.

The downside? Talent development does not come free. Tech buyers may need to pay a higher fee to encourage the suppliers but paying a low-cost provider who does not develop their talent sounds like a recipe for poor quality service.

If you would like to discuss any of these thoughts or issues further, please feel free to reach out and contact me. This is an industry issue and one for our broader society, so I would be interested in hearing how your organisations are addressing this challenge.

2020 was a strange year for retail. Businesses witnessed significant disruption to supply chains, significant swings in demand for products (toilet paper, puzzles, bikes etc!) and then sometimes incredible growth – as disposable income increased as many consumers are no longer taking expensive holidays. Overall, it was a mixed year, with many retailers closing down and others reporting record sales. The grocery sector boomed – with many restaurants and fast-food providers closed, sometimes the supermarkets were some of the few remaining open retailers.

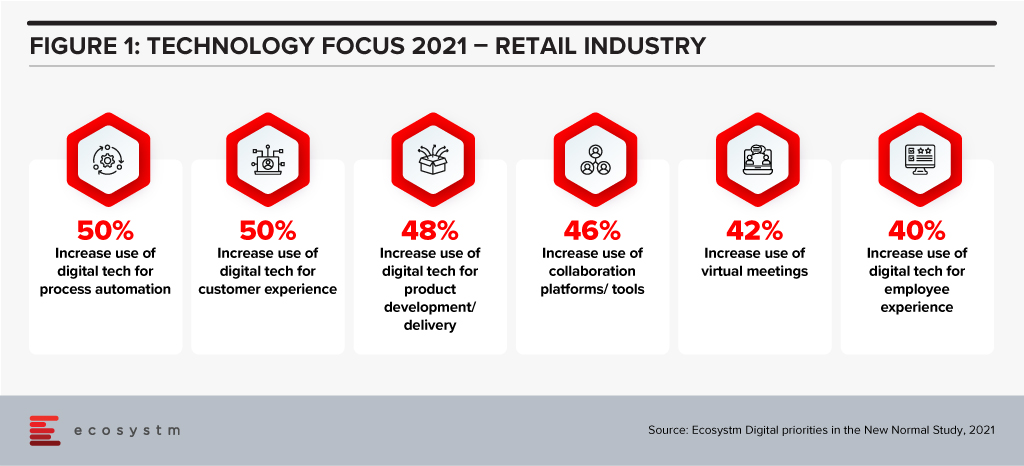

For many retailers, technology has become a key enabler to their transformation, survival and success (Figure 1).

Woolworths, Australia’s largest retailer, operates across the grocery, department store, drinks, and hospitality sectors. They hold a significant market share in most markets that they operate in. The company had a strong 2019/20 (financial year runs from July 2019 to June 2020) with sales up 8% – and in the first half of the 2020/21 financial year, sales were up nearly 11%. But the company is not resting on its laurels – one of its 6 key priorities is to “Accelerate Digital, eCom and convenience for our increasingly connected customers”. This requires more than just a deep technology investment, but a new culture, new skills, and new ways of working.

Woolworths’ Employee Focus

Woolworths has committed to invest AUD 50 million in upskilling and reskilling their employees in areas such as digital, data analytics, machine learning and robotics over the next three years. The move comes as a response to the way the Retail industry has been disrupted and the need to futureproof to stay relevant and successful. The training will be provided through online platforms and through collaborations with key learning institutions.

The supermarket giant is one of Australia’s largest private employers with more than 200,000 employees. Under Woolworths’ ‘Future of Work Fund’ their staff will be trained across supply chain, store operations, and support functions to enhance delivery and decision-making processes. The retailer will also create an online learning platform that will be accessible by Woolworths employees as well as by other retail and service companies to support the ecosystem. Woolworths has plans to upskill their staff in customer service abilities, leadership skills and agile ways of working.

Woolworths’ upskilling program will also support employees who were impacted by Woolworths planned closures of Minchinbury, Yennora, and Mulgrave distribution centres due in 2025.

Woolworths’ Tech Focus

Woolworths has been ramping up their technology investments and having tech-savvy employees will be key to their future success. In October 2020, Woolworths deployed micro automation technology to revamp their eCommerce facility in Melbourne to speed up the fulfilment of online grocery orders, and front and back-end operations. Woolworths also partnered with Dell Technologies in November 2020 to bring together their private and public cloud onto a single platform to improve mission-critical processes, applications and support inventory management operations across its retail stores.

Future of Work

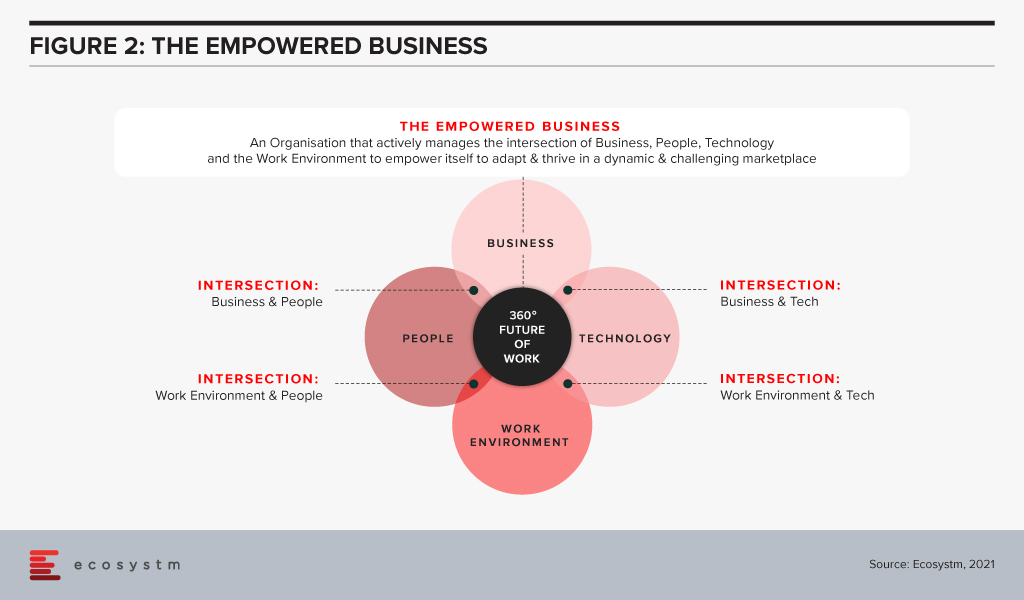

For many years, Ecosystm has been advising our clients to invest more in the skills of the business. Every business will be using more cloud next year than they are this year; they will suffer more cybersecurity incidents; they will use more AI and machine learning; they will automate more processes than are automated today. More of their customer engagements will be digital, and more insight will be required to drive better outcomes for customers and employees. This all needs new skills – or more people trained on skills that some in the business already understand. But too many businesses don’t train in advance – instead waiting for the need and paying external consultants or expensive new hires for their skills. Empowered businesses – ones that are creating a future-ready, agile business – invest in their people, work environment, business processes and technology to create an environment where innovation, transformation and business change are accepted and encouraged (Figure 2).

Empowered businesses can adapt to new challenges, new market conditions and respond to new competitive threats. By taking these steps to upskill and empower their employees, Woolworths is building towards empowering their own business for long term success.

Transform and be better prepared for future disruption, and the ever-changing competitive environment and customer, employee or partner demands in 2021. Download Ecosystm Predicts: The top 5 Future of Work Trends For 2021.

Over the next few months, we’re going to be focusing on the five stages of the Digital Value Journey and how an organisation and a leadership team can progress through these stages.

The Journey starts with baselining and then improving your execution capability.

Your Foundation

The quality of your execution needs to be consistently improved as you and your organisation make progress through your Journey. At the start, it is about developing the foundation on which you can build more complex and valuable business capabilities. You need that reliable, performing foundation that delivers what your customers and employees need every day.

For any Digital or IT organisation to succeed, it needs two critical things: a record of consistent success, and the trust from your organisation that past performance is a reliable predictor of the future.

Every day your customers and employees will be evaluating those two things. It’s like sitting a difficult exam every day. Failing one will be remembered – much more so than all the other exams that you successfully passed. To pass that exam you need to clearly understand what people are testing you on every day.

Understanding how the quality of your work will be evaluated is essential to creating and maintaining this firm foundation. Everything you do later in the Journey will depend on the foundation you establish at the start.

Evaluating your Foundation

And you don’t have the freedom to choose how that foundation is going to be evaluated. There is a universe – or perhaps that should be a multiverse – of metrics that you could use. Selecting the small set of metrics that your stakeholders believe demonstrate your performance is essential.

Too many metrics is just as bad as too few – you won’t know which ones to focus on so you will end up spreading yourself too thinly. Your stakeholders are the best people to tell you how to measure your performance. Work with them to determine the one or two indicators that they really care about.

Schools and universities have improved dramatically in explaining how they are going to evaluate a student’s performance since I attended! As part of almost every assignment, educators include an evaluation rubric to guide each student. This sets out what how the educator will assess the students work. So, getting great grades is dependent on understanding this rubric.

What is your rubric? Without one how will you know what outcomes your stakeholders value and how they will evaluate your work? Spending time to talk with your stakeholders about what they value, is a habit that is worth developing early and maintaining throughout the Journey.

Your Next Best Steps

Getting this execution foundation right is the basis for everything that follows.

In the first of a series of webinars on 22 April, we will be introducing the concepts and ideas that we will expand on over the series.

Getting a quality education is a long hard slog – and I can’t promise that starting this Digital Journey will be any different. At each stage of the Journey different levels of capability will be required, but, as with an education, these higher levels of capability will only be possible if the right foundation is in place. So, join us to see how you can use the Digital Value Journey to lift the performance of your organisation and its Digital or IT Team.

How do digital leaders shift from providing a cost-focused to a value-focused service? At the CXO Digital Leaders Dialogue series, together with Best Case Scenario, we will be in discussion with leaders who will share their experiences with navigating these challenges.

To learn more, or to register to attend, visit here

In 2009 one of the foremost Financial Services industry experts was giving my team a deep dive into the Global Financial Crisis (GFS) and its ramifications. According to him, one of the key reasons why it happened was that most people in key positions in both industry and government had probably never seen a full downturn in their careers. There was a bit of a hiccup during the dot com bust but nothing that seriously interrupted the long boom that began somewhere in 1988. They had never experienced anything quite like 2008; so they never imagined that such a crisis could actually happen.

Similarly, 2020 was an unprecedented year – in our lives and certainly for the tech industry. The GFC (as the name suggests) was a financial crisis. A lot of people lost their jobs, but after the bailouts things went largely back to normal. COVID-19 is something different altogether – the impact will be felt for years and we don’t yet know the full implications of the crisis.

While we would like to start 2021 with a clean slate and never talk about the pandemic again, the reality is that COVID-19 will shape what we will see this year. In the first place it looks like the disease will still be around for a substantial part of the year. Secondly, all the changes it has brought in 2020 with entire workforces suddenly moving to operating from home will have profound implications for technology and customer experience this year.

As we ease into 2021, I look at some of the organisational and technology trends that are likely to impact customer experience (CX) in 2021.

#1 All Business is Now eBusiness

COVID-19 has ensured that the few businesses which did not have an online presence became acutely aware that they needed one. It created a need for many businesses to quickly initiate eCommerce. Forbes reported a 77% increase in eCommerce infrastructure spending YoY. This represents about 4 years of growth squeezed into the first 6 months of 2020!

From a CX point of view there is going to be far more interaction with brands and products through online channels. This is not just about eCommerce and buying from a portal. It is also about using tools like Instagram, Facebook and other social media platforms more widely. It is about learning to interact with the customer in multiple ways and touching their journeys at multiple points, all virtually using the web – mostly the mobile web.

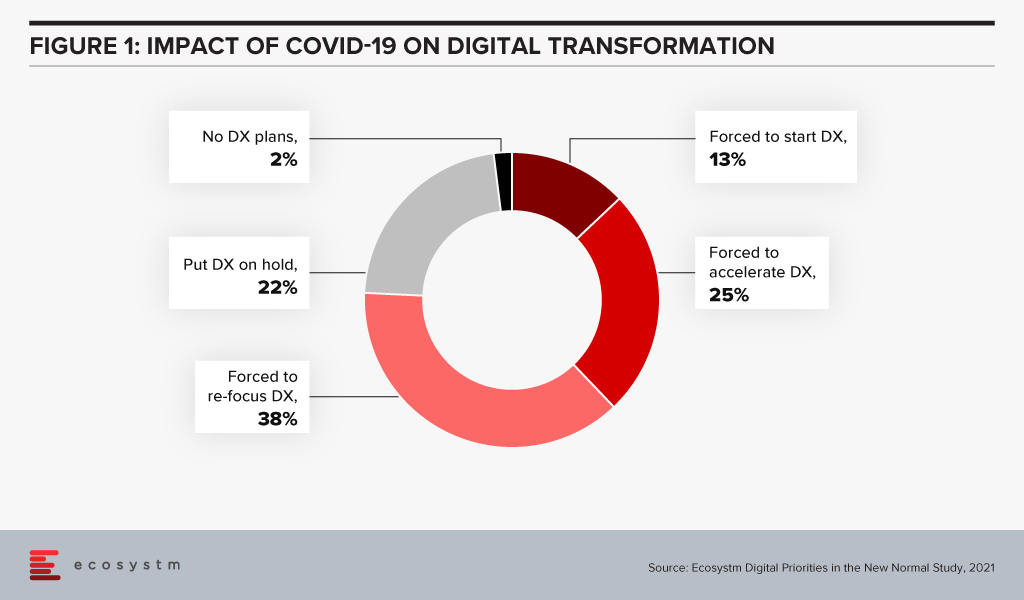

Ecosystm research shows that almost three out of four companies have decided on accelerating or modifying the digitalisation they were undergoing (Figure 1). It is fair to expect that this gives a further boost to moving to the cloud. For the customer it will mean being able to access information in many new ways and connect with products, services, brands at multiple points on the web.

Since interacting with the customer at multiple points is new for most services, I foresee a lot of missed opportunities as companies learn to navigate a completely different landscape. Customers pampered by digitally native organisations often react harshly to even a small mistake. It will become critical for companies to not just become a bigger presence online but also to manage their customers well.

New solutions such as Customer Data Platforms (CDP), as opposed to CRM will become common. Players who are into Customer Experience management are likely to see huge business growth and new players will rapidly enter this space. They will promise to affordably manage CX across the globe, leveraging the cloud.

#2 Virtual Merges with Real

Virtual and Augmented Reality are not new. They have been around for a while. This will now cross the early adoption stage and is likely to proliferate in terms of use cases and importance.

AR/VR has so far been seen mainly in games where one wears an unwieldy – though ever-improving – headset to transport oneself into a 3D virtual world. Or in certain industrial applications e.g., using a mobile device to look at some machinery; the device captures what the eye can see while providing graphical overlays with information. In 2021 I expect to see almost all industrial applications adopting some form of this technology. This will have an impact on how products are serviced and repaired.

For the mainstream, 2020 was the year of videoconferencing – as iconic as the shift to virtual meetings has been, there is much more to come. Meetings, conferences, events, classrooms have all gone virtual. Video interaction with multiple people and sharing information via shared applications is commonplace. Virtual backgrounds which hide where you are actually speaking from are also widely used and getting more creative by the day.

Imagine then a future where you get on one of these calls wearing a headset and are transported into a room where your colleagues who are joining the call also are. You see them as full 3D people, you see the furniture, and the room decor. You speak and everyone sees your 3D avatar speak, gesture (as you gesture from the comfort of your home office) and move around. It will seem like you are really in the conference room together! If this feels futuristic or unreal try this or look at how the virtual office can look in the very near future.

While the solutions may not look very sophisticated, they will rapidly improve. AR/VR will start to really make its presence felt in the lives of consumers. From being able to virtually “try” on clothes from a boutique to product launches going virtual, these technologies will deeply impact customer experience in 2021 and beyond

In the immortal words of Captain Kirk, we will be going where no man has gone before – enabled by AR / VR.

#3 Digital CX will involve Multiple Technologies

AI, IoT and 5G will continue to support wider CX initiatives.

The advances that I have mentioned will gain impetus from 5G networking, which will enable unprecedented bandwidth availability. To deliver an AR experience over the cloud, riding on a 5G network, will literally be a game changer compared to the capabilities of older networks.

Similarly, IoT will lead to massive changes in terms of product availability, customisation and so on. 5G-enabled IoT will allow a lot more data to be carried a lot faster; and more processing at the edge. IoT will have some initial use cases in Retail, Services and other non-manufacturing sectors – but perhaps not as strongly as some commentators seem to indicate.

AI continues to drive change. While AI may not transform CX in 2021, this is a technology which will be a component of most other CX offerings, and so will impact customer experience in the next few years. In fact, thinking of businesses in 2025 I cannot believe that there will be a single business to customer (B2C) interaction which will not feature some form of AI technology.

I’d be interested to hear your thoughts on the technologies which will impact CX in 2021 – Connect with me on the Ecosystm platform.

In 2020, much of the focus for organisations were on business continuity, and on empowering their employees to work remotely. Their primary focus in managing customer experience was on re-inventing their product and service delivery to their customers as regular modes were disrupted. As they emerge from the crisis, organisations will realise that it is not only their customer experience delivery models that have changed – but customer expectations have also evolved in the last few months. They are more open to digital interactions and in many cases the concept of brand loyalty has been diluted. This will change everything for organisations’ customer strategies. And digital technology will play a significant role as they continue to pivot to succeed in 2021 – across regions, industries and organisations.

Ecosystm Advisors Audrey William, Niloy Mukherjee and Tim Sheedy present the top 5 Ecosystm predictions for Customer Experience in 2021. This is a summary of the predictions – the full report (including the implications) is available to download for free on the Ecosystm platform.

The Top 5 Customer Experience Trends for 2021

- Customer Experience Will Go Truly Digital

COVID-19 made the few businesses that did not have an online presence acutely aware that they need one – yesterday! We have seen at least 4 years of digital growth squeezed into six months of 2020. And this is only the beginning. While in 2020, the focus was primarily on eCommerce and digital payments, there will now be a huge demand for new platforms to be able to interact digitally with the customer, not just to be able to sell something online.

Digital customer interactions with brands and products – through social media, online influencers, interactive AI-driven apps, online marketplaces and the like will accelerate dramatically in 2021. The organisations that will be successful will be the ones that are able to interact with their customers and connect with them at multiple touchpoints across the customer journey. Companies unable to do that will struggle.

- Digital Engagement Will Expand Beyond the Traditional Customer-focused Industries

One of the biggest changes in 2020 has been the increase in digital engagement by industries that have not traditionally had a strong eye on CX. This trend is likely to accelerate and be further enhanced in 2021.

Healthcare has traditionally been focused on improving clinical outcomes – and patient experience has been a byproduct of that focus. Many remote care initiatives have the core objective of keeping patients out of the already over-crowded healthcare provider organisations. These initiatives will now have a strong CX element to them. The need to disseminate information to citizens has also heightened expectations on how people want their healthcare organisations and Public Health to interact with them. The public sector will dramatically increase digital interactions with citizens, having been forced to look at digital solutions during the pandemic.

Other industries that have not had a traditional focus on CX will not be far behind. The Primary & Resources industries are showing an interest in Digital CX almost for the first time. Most of these businesses are looking to transform how they manage their supply chains from mine/farm to the end customer. Energy and Utilities and Manufacturing industries will also begin to benefit from a customer focus – primarily looking at technology – including 3D printing – to customise their products and services for better CX and a larger share of the market.

- Brands that Establish a Trusted Relationship Can Start Having Fun Again

Building trust was at the core of most businesses’ CX strategies in 2020 as they attempted to provide certainty in a world generally devoid of it. But in the struggle to build a trusted experience and brand, most businesses lost the “fun”. In fact, for many businesses, fun was off the agenda entirely. Soft drink brands, travel providers, clothing retailers and many other brands typically known for their fun or cheeky experiences moved the needle to “trust” and dialed it up to 11. But with a number of vaccines on the horizon, many CX professionals will look to return to pre-pandemic experiences, that look to delight and sometimes even surprise customers.

However, many companies will get this wrong. Customers will not be looking for just fun or just great experiences. Trust still needs to be at the core of the experience. Customers will not return to pre-pandemic thinking – not immediately anyway. You can create a fun experience only if you have earned their trust first. And trust is earned by not only providing easy and effective experiences, but by being authentic.

- Customer Data Platforms Will See Increased Adoption

Enterprises continue to struggle to have a single view of the customer. There is an immense interest in making better sense of data across every touchpoint – from mobile apps, websites, social media, in-store interactions and the calls to the contact centre – to be able to create deeper customer profiles. CRM systems have been the traditional repositories of customer data, helping build a sales pipeline, and providing Marketing teams with the information they need for lead generation and marketing campaigns. However, CRM systems have an incomplete view of the customer journey. They often collect and store the same data from limited touchpoints – getting richer insights and targeted action recommendations from the same datasets is not possible in today’s world. And organisations struggled to pivot their customer strategies during COVID-19. Data residing in silos was an obstacle to driving better customer experience.

We are living in an age where customer journeys and preferences are becoming complex to decipher. An API-based CDP can ingest data from any channel of interaction across multiple journeys and create unique and detailed customer profiles. A complete overhaul of how data can be segregated based on a more accurate and targeted profile of the customer from multiple sources will be the way forward in order to drive a more proactive CX engagement.

- Voice of the Customer Programs Will be Transformed

Designing surveys and Voice of Customer programs can be time-consuming and many organisations that have a routine of running these surveys use a fixed pattern for the data they collect and analyse. However, some organisations understand that just analysing results from a survey or CSAT score does not say much about what customers’ next plan of action will be. While it may give an idea of whether particular interactions were satisfactory, it gives no indication of whether they are likely to move to another brand; if they needed more assistance; if there was an opportunity to upsell or cross sell; or even what new products and services need to be introduced. Some customers will just tick the box as a way of closing off a feedback form or survey. Leading organisations realise that this may not be a good enough indication of a brand’s health.

Organisations will look beyond CSAT to other parameters and attributes. It is the time to pay greater attention to the Voice of the Customer – and old methods alone will not suffice. They want a 360-degree view of their customers’ opinions.

2020 saw a shutdown in both supply and demand which has effectively put the brakes on many economic activities and forced a complete rethink on how to continue doing business and maintain social interactions. The COVID-19 pandemic has accelerated digitalisation of consumers and enterprises, and the telecommunications industry has been the pillar which has kept the world ticking over. The rise in data use coupled with the fervent growth of the digital economy augurs well for the telecom sector in 2021.

Ecosystm Advisors Claus Mortensen, Rahul Gupta, and Shamir Amanullah present the top 5 Ecosystm predictions for Telecommunications & Mobility trends for 2021. This is a summary of the predictions – the full report (including the implications) is available to download for free on the Ecosystm platform.

The Top 5 Telecommunications & Mobility Trends for 2021

- The 5G Divide – Reality for Some and Hype for Others

Despite the economic challenges in 2020, GSMA reports that the global 5G subscriptions doubled QoQ in Q2 2020 to hit at least 137.7 million subscribers. This accounts for 1.5% of total subscribers – and is expected to rise to 30% by 2025.

The value of 5G will become increasingly mainstream in the next few years. 5G offers a tailored user-centric approach to network services, low latency and significantly higher number of connections which will power a new era of mobile Internet of Everything (IoE).

However, there are many operators who are still sceptical about 5G. In the US, many operators failed to get any tangible positives from 5G. In the near term, many operators will continue to evolve their 5G capabilities – a full grown standalone 5G technology implementation in some verticals might take longer.

The unsuccessful launch of 5G by the US operators does not mean that 5G is a failure, however. It also implies that we need to look at other geographies to lead us into 5G – and Asia Pacific may well emerge as a leader in this space. China, for example, leads the drive in 5G adoption; and 5G smartphones account for more than half of global sales in recent months.

- Telecom Operators Will Accelerate Digital Transformation

Telecom operators are facing increasing demands for cutting-edge services and top-notch customer experience (CX). The global pandemic has caused revenue loss, due to struggling economies and many operators will aim to reduce OpEX to circumvent these financial pressures, raise the quality of CX and retain existing customers. To realise this, there will be much focus on improvement in efficiencies, better operations management as well as improving the IT stack. These digital transformation efforts will enable rapid and flexible services provisioning, which will be better prepared for the tailored services customers now demand.

Many operators are increasingly incorporating cloudification alongside the 5G network deployment. Operators are moving towards transforming their operations and business support systems to a more virtualised and software-defined infrastructure. 5G will operate across a range of frequencies and bands – with significantly more devices and connections becoming software-defined with computing power at the Edge. Operators will also harness the power of AI to analyse massive volumes of data from the networks accessed by millions of devices in order to improve CX, ramp up operational efficiencies as well as introduce new services tailored to customer needs to increase revenue.

- Remote Working Will Transform Telecommunications Networks

The changing patterns in peak network traffic and the substantial movement of traffic from central business districts to residential areas require a fundamental rethink in network traffic management. In addition, many businesses continue to ramp up digital transformation efforts to conduct business online as physical channels will remain limited. Consumer onboarding will also be fervent, as organisations look at business recovery – resulting in increase in bandwidth requirements.

The increasing remote working trend is amplifying the need for greater cybersecurity. Cybersecurity has catapulted in importance as the pandemic has seen a worrying increase in attacks on banks, cloud servers and mobile devices, among others. Cyber-attack incidents specifically due to remote working, has seen a rise. A telecom operator’s compromised security can have country-wide, and even global consequences.

- SASE Will Grow – and Sprawl

Although it was perhaps originally seen as an Over-The-Top (OTT) provisioned competitive service to operators’ MPLS services, many telecom service providers have been embracing SD-WAN over the years as part of their managed services portfolio. “Traditional” SD-WAN offers some of the flexibility needed to address the change towards a more distributed access and the workload requirements that the pandemic has accelerated – the technology does not address all of the issues related to this transformed workspace.

Employees are now working from a variety of locations and workloads are becoming increasingly distributed. To address this change, organisations are challenged to move workloads and applications between platforms, potentially compromising security. Despite all the challenges that the pandemic brought with it – both human and technical – it has also provided organisations with an opportunity to rethink their IT and WAN architectures and to adopt an approach that has security at its core.

We believe that secure access service edge (SASE), which is a model for combining SD-WAN and security in a cloud-based environment, will see a drastic rise in adoption in 2021 and beyond.

- OTT Players Will Continue their Expansion in the Telecommunications Space

Facebook, Google, Amazon are no longer considered as web companies as they moved from standalone ‘web’ companies to become OTT providers and are now significant players in telecom space. With the Facebook-Jio deal in India earlier this year, and with Google and Amazon actively eyeing the telecom space, these players will continue to explore this space especially in the emerging markets of Asia and Africa. There are telecom providers in these countries which will be prime targets for partnerships. These operators could be those that have a large customer base, are struggling with their bottom lines or are already looking at exit routes. OTT players were already offering services like voice, messaging, video calling and so on which have been the domain expertise of mobile operators for a long time. The market will see instances where telecom providers will sell small stakes to OTT players at a premium and get access to the vast array of services that these OTT providers offer.

Public sector organisations are looking at 2021 as the year where they either hobble back to normalcy or implement their successful pilots (that were honed under tremendous pressure). Ecosystm research finds that 60% of government agencies are looking at 2021 as the year they make a recovery to normal – or the normal that finally emerges. The path to recovery will be technology-driven, and this time they will look at scalability and data-driven intelligence.

Ecosystm Advisors Alan Hesketh, Mike Zamora and Sash Mukherjee present the top 5 Ecosystm predictions for Cities of the Future in 2021. This is a summary of our Cities of the Future predictions – the full report (including the implications) is available to download for free on the Ecosystm platform here.

The Top 5 Cities of the Future Trends for 2021

#1 Cities Will Re-start Their Transformation Journey by Taking Stock

In 2021 the first thing that cities will do is introspect and reassess. There have been a lot of abrupt policy shifts, people changes, and technology deployments. Most have been ad-hoc, without the benefit of strategy planning, but many of the services that cities provide have been transformed completely. Government agencies in cities have seen rapid tech adoption, changes in their business processes and in the mindset of how their employees – many who were at the frontline of the crisis – provide citizen services.

Technology investments, in most cases, took on an unexpected trajectory and agencies will find that they have digressed from their technology and transformation roadmap. This also provides an opportunity, as many solutions would have gone through an initial ‘proof-of-concept’ without the formal rigours and protocols. Many of these will be adopted for longer term applications. In 2021, they will retain the same technology priorities as 2020, but consolidate and strengthen on their spend.

#2 Cities Will be Instrumented Using Intelligent Edge Devices

The capabilities of edge devices continue to increase dramatically, while costs decline. This reduces the barriers to entry for cities to collect and analyse significantly more data about the city and its people. Edge devices move computational power and data storage as close to the point of usage as possible to provide good performance. Devices range from battery powered IoT devices for data collection through to devices such as smart CCTV cameras with embedded pattern recognition software.

Cities will develop many use cases for intelligent edge devices. These uses will range from enhancing old assets using newer approaches to data collection – through to accelerating the speed and quality of the build of a new asset. The move to data-driven maintenance and decision-making will improve outcomes.

#3 COVID-19 Will Impact City Design

The world has received a powerful reminder of the vulnerability of densely populated cities, and the importance of planning and regulating public health. COVID-19 will continue to have an impact on city design in 2021.

A critical activity in controlling the pandemic in this environment is the test-and-trace capabilities of the local public health authorities. Technology to provide automated, accurate, contact tracing to replace manual efforts is now available. Scanning of QR codes at locations visited is proving to be the most widely adopted approach. The willingness of citizens to track their travels will be a crucial aid in managing the spread of COVID-19.

Early detection of new disease outbreaks, or other high-risk environmental events, is essential to minimise harm. Intelligent edge devices that detect the presence of viruses will become crucial tools in a city’s defence.

Intelligent edge devices will also play a role in managing building ventilation. Well-ventilated spaces are an important factor in controlling virus transmission. But a limited number of buildings have ventilation systems that are capable of meeting those requirements. Property owners will begin to refit their facilities to provide better air movement.

#4 Technology Vendors Will Emerge as the Conductors of Cities of the Future

The built environment comprises not only of the physical building, but also the space around the buildings and building operations. The real estate developer/investor owns the building – the urban fabric, the relationship of buildings to each other, the common space and the common services provided to the city, is owned by the City. The question is who will coordinate the players, e.g. business, citizens, government and the built environment. Ideally the government should be the conductor. However, they may not have sufficient experience or knowledge to properly implement this role. This means a capable and knowledgeable neutral consultant will at least initially fill this role. There is an opportunity for a technology vendor to fill that consulting role and impact the city fabric. This enhanced city environment will be requested by the Citizen, driven by the City, and guided by Technology Vendors. 2021 will see leading technology vendors working very closely with cities.

#5 Compliance Will be at the Core of Citizen Engagement Initiatives

Many Smart Cities have long focused on online services – over the last couple of years mobile apps have further improved citizen services. In 2020, the pandemic challenged government agencies to continue to provide services to citizens who were housebound and had become more digital savvy almost overnight. And many cities were able to scale up to fulfill citizen expectations.

However, in 2021 there will be a need to re-evaluate measures that were implemented this year – and one area that will be top priority for public sector agencies is compliance, security and privacy.

The key drivers for this renewed focus on security and privacy are:

- The need to temper the focus of ‘service delivery at any cost’ and further remind agencies and employees that security and privacy must comply with standard to allow the use of government data.

- The rise of cyberattacks that target not only essential infrastructure, but also individual citizens and small and medium enterprises (SMEs).

- The rise of app adoption by city agencies – many that have been developed by third parties. It will become essential to evaluate their compliance to security and privacy requirements.

Artificial Intelligence (AI) is becoming embedded in financial services across consumer interactions and core business processes, including the use of chatbots and natural language processing (NLP) for KYC/AML risk assessment.

But what does AI mean for financial regulators? They are also consuming increasing amounts of data and are now using AI to gain new insights and inform policy decisions.

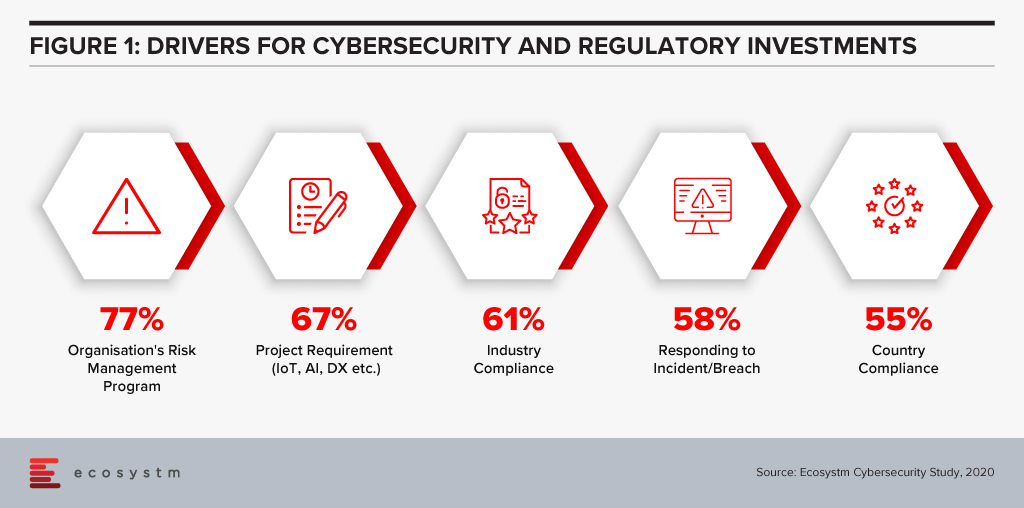

The efficiencies that AI offers can be harnessed in support of compliance within both financial regulation (RegTech) and financial supervision (SupTech). Authorities and regulated institutions have both turned to AI to help them manage the increased regulatory requirements that were put in place after the 2008 financial crisis. Ecosystm research finds that compliance is key to financial institutions (Figure 1).

SupTech is maturing with more robust safeguards and frameworks, enabling the necessary advancements in technology implementation for AI and Machine Learning (ML) to be used for regulatory supervision. The Bank of England and the UK Financial Conduct Authority surveyed the industry in March 2019 to understand how and where AI and ML are being used, and their results indicated 80% of survey respondents were using ML. The most common application of SupTech is ML techniques, and more specifically NLP to create more efficient and effective supervisory processes.

Let us focus on the use of NLP, specifically on how it has been used by banking authorities for policy decision making during the COVID-19 crisis. AI has the potential to read and comprehend significant details from text. NLP, which is an important subset of AI, can be seen to have supported operations to stay updated with the compliance and regulatory policy shifts during this challenging period.

Use of NLP in Policy Making During COVID-19

The Financial Stability Board (FSB) coordinates at the international level, the work of national financial authorities and international standard-setting bodies in order to develop and promote the implementation of effective regulatory, supervisory and other financial sector policies. A recent FSB report delivered to G20 Finance Ministers and Central Bank Governors for their virtual meeting in October 2020 highlighted a number of AI use cases in national institutions.

We illustrate several use cases from their October report to show how NLP has been deployed specifically for the COVID-19 situation. These cases demonstrate AI aiding supervisory team in banks and in automating information extraction from regulatory documents using NLP.

De Nederlandsche Bank (DNB)

The DNB is developing an interactive reporting dashboard to provide insight for supervisors on COVID-19 related risks. The dashboard that is in development, enables supervisors to have different data views as needed (e.g. over time, by bank). Planned SupTech improvements include incorporating public COVID-19 information and/or analysing comment fields with text analysis.

Monetary Authority of Singapore (MAS)

MAS deployed automation tools using NLP to gather international news and stay abreast of COVID-19 related developments. MAS also used NLP to analyse consumer feedback on COVID-19 issues, and monitor vulnerabilities in the different customer and product segments. MAS also collected weekly data from regulated institutions to track the take-up of credit relief measures as the pandemic unfolded. Data aggregation and transformation were automated and visualised for monitoring.

US Federal Reserve Bank Board of Governors

One of the Federal Reserve Banks in the US is currently working on a project to develop an NLP tool used to analyse public websites of supervised regulated institutions to identify information on “work with your customer” programs, in response to the COVID-19 crisis.

Bank of England

The Bank developed a Policy Response Tracker using web scraping (targeted at the English versions of each authority/government website) and NLP for the extraction of key words, topics and actions taken in each jurisdiction. The tracker pulls information daily from the official COVID-19 response pages then runs it through specific criteria (e.g. user-defined keywords, metrics and risks) to sift and present a summary of the information to supervisors.

Market Implications

Even with its enhanced efficiencies, NLP in SupTech is still an aid to decision making and cannot replace the need for human judgement. NLP in policy decision is performing clearly defined information gathering tasks with greater efficiency and speed. But NLP cannot change the quality of the data provided, so data selection and choice are still critical to effective policy making.

For authorities, the use of SupTech could improve oversight, surveillance, and analytical capabilities. These efficiency gains and possible improvement in quality arising from automation of previously manual processes could be consideration for adoption.

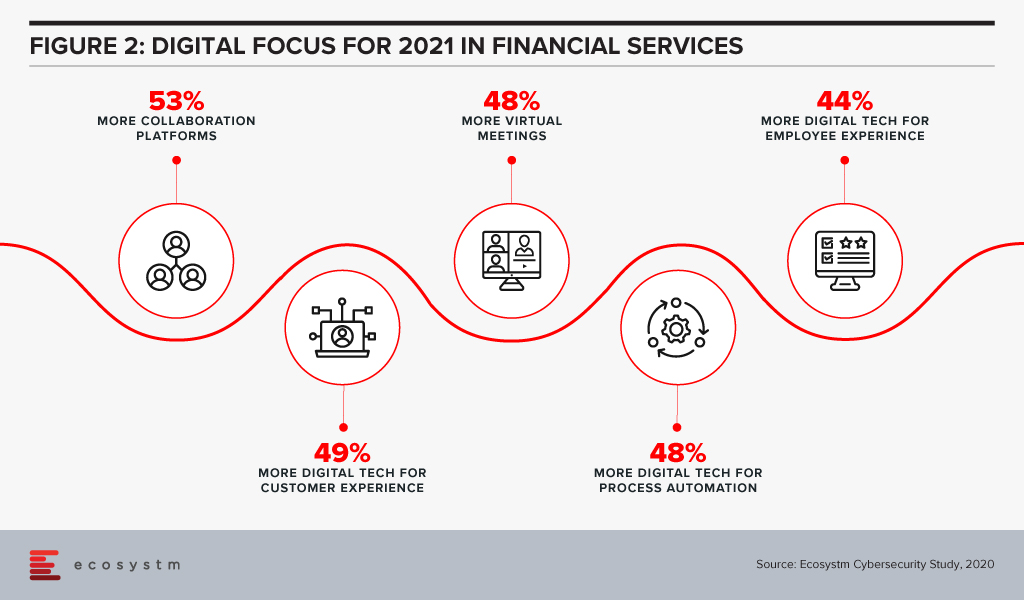

Attention will be paid in 2021 to focusing on automation of processes using AI (Figure 2).

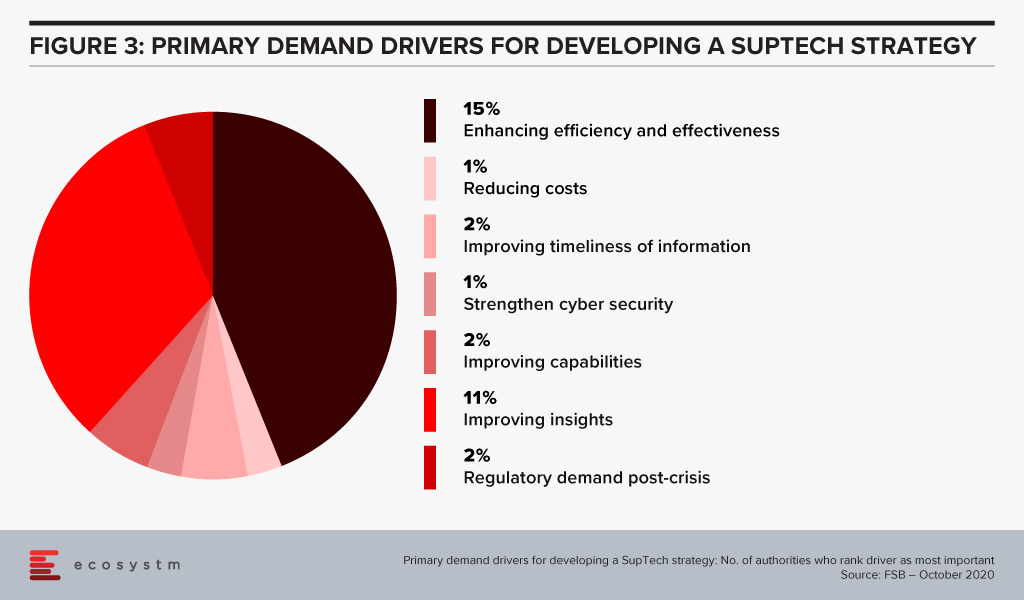

Based on a survey done by the FSB of its members (Figure 3), the majority of their respondents had a SupTech innovation or data strategy in place, with the use of such strategies growing significantly since 2016.

Summary

For more mainstream adoption, data standards and use of effective governance frameworks will be important. As seen from the FSB survey, SupTech applications are now used in reporting, data management and virtual assistance. But institutions still send the transaction data history in different reporting formats which results in a slower process of data analysing and data gathering. AI, using NLP, can help with this by streamlining data collection and data analytics. While time and cost savings are obvious benefits, the ability to identify key information (the proverbial needle in the haystack) can be a significant efficiency advantage.

Singapore FinTech Festival 2020: Infrastructure Summit

For more insights, attend the Singapore FinTech Festival 2020: Infrastructure Summit which will cover topics tied to creating infrastructure for a digital economy; and RegTech and SupTech policies to drive innovation and efficiencies in a co-Covid-19 world.