Thailand’s digital transformation has shifted from an ambitious policy agenda to a national necessity. As the country accelerates its Thailand 4.0 strategy, digital platforms are becoming central to boosting competitiveness, enhancing public services, and building economic resilience. From logistics and healthcare to finance and manufacturing, digital tools now underpin how Thailand moves, heals, pays, and grows.

Recent reforms, including the National AI Strategy, Smart City Masterplan, and National Digital ID framework, have been paired with efforts to strengthen digital infrastructure nationwide. Yet challenges remain: integrating platforms across government, closing the generational digital divide, and safeguarding vulnerable users in a rapidly evolving fintech and gig economy.

Through multiple roundtables and stakeholder dialogues, Ecosystm has uncovered five core themes that highlight both the momentum and the friction points in Thailand’s digital journey.

Theme 1: Bridging the Regional Divide

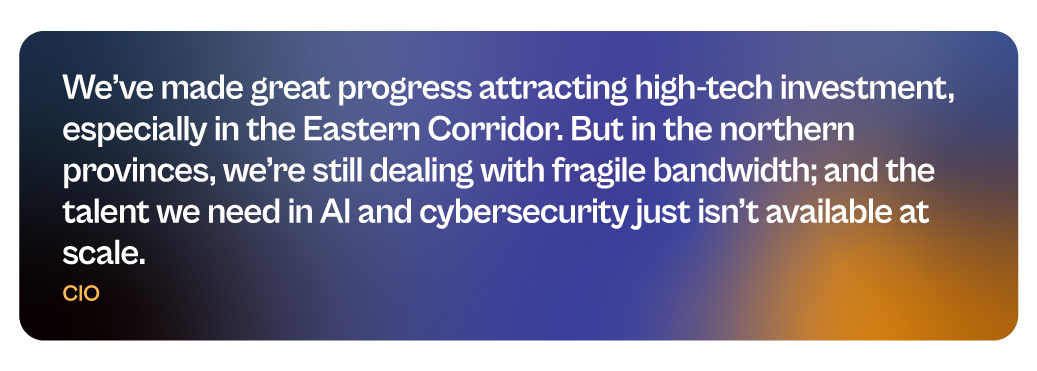

Thailand’s digital transformation is accelerating in urban centres like Bangkok, Chonburi, and Rayong, but rural and low-income regions, especially in the North and Deep South, continue to lag. Gaps in connectivity, digital skills, and modern technical education are limiting access to online learning, mobile banking, and digital public services, while also holding back the growth of tech-driven industries.

Initiatives like Net Pracharat have brought broadband to over 75,000 villages, and new investments in regional data centres and telecom infrastructure show promise. Still, last-mile gaps and fragile networks persist, particularly in conflict-affected or underserved areas. Even where fibre is available, unstable connections often block meaningful digital adoption.

At the same time, Thailand’s push into future-focused industries such as EVs, semiconductors, AI, and smart logistics, is straining its talent pipeline. The Eastern Economic Corridor (EEC) is attracting major investment, but the demand for skilled workers in data science, cybersecurity, and industrial AI far exceeds supply. Many regional technical education systems have not kept pace, widening the skills gap.

To ensure inclusive growth, Thailand needs to pair infrastructure investment with targeted reskilling and education reform. Programs like the Digital Skill Development Academy and revamped TVET initiatives are important first steps; but broader progress will require stronger industry-academia partnerships, faster certification pathways, and universal access to digital learning.

Theme 2: Unifying Government Services for a Seamless Citizen Journey

From PromptPay-linked welfare payments and Mor Prom for health services, to the rollout of the NDID (National Digital ID), Thailand has made considerable progress in digitalising public services. Citizens can now access more services online than ever before.

However, many of these systems still operate in silos, with duplicated citizen data, separate logins, and limited backend integration between agencies. Ministries and local governments often lack the interoperability standards and cloud infrastructure needed to provide seamless, real-time services.

The next phase of government digitalisation must focus on platform-level integration, supported by secure data sharing frameworks, API-first design, and privacy-by-default policies. The goal is to move from digitising transactions to building a citizen-centric, connected state, where services are proactive, mobile-friendly, and unified across domains.

Theme 3: Strengthening Public Trust Through Proactive Cybersecurity

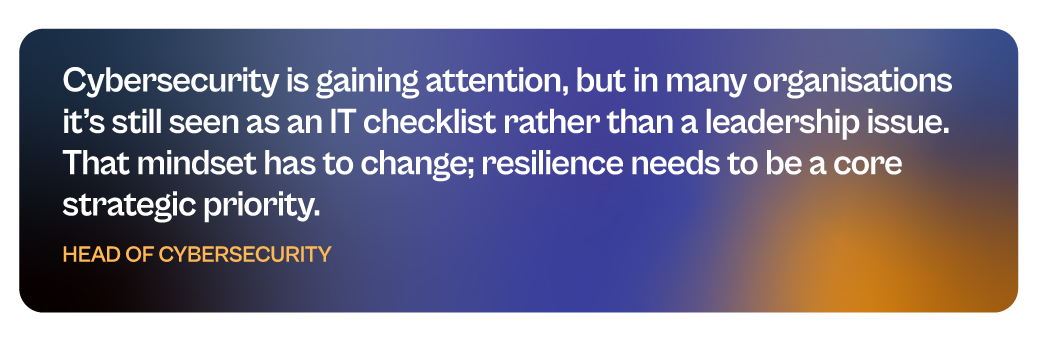

With the rise of digital government, cloud adoption, and cashless ecosystems, Thailand’s attack surface is rapidly expanding. High-profile breaches in healthcare, telecom, and finance have triggered growing public concern around data misuse, fraud, and infrastructure vulnerabilities.

The government has enacted the Cybersecurity Act (2019) and PDPA (2022), and agencies like the National Cybersecurity Agency (NCSA) are stepping up threat monitoring. But cybersecurity maturity across sectors remains uneven. Many SMEs, regional hospitals, and even provincial government systems operate with limited threat intelligence and minimal incident response protocols.

Cybersecurity must now move from compliance to strategic resilience. This includes building sector-specific response plans, launching cyber drills in critical infrastructure, and scaling cyber talent development across the country. Trust in digital services will depend not just on what’s offered, but on how securely it’s delivered.

Theme 4: Scaling Trust Through Local Language, Visibility, and Human Oversight

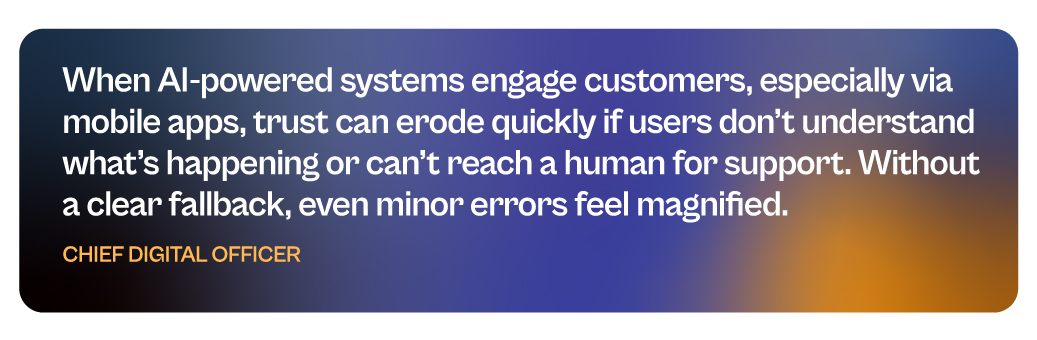

AI systems in Thailand are increasingly interfacing with the public, from chatbots and digital assistants to automated approvals and diagnostics. However, public trust in these systems remains fragile, particularly when users cannot understand how decisions are made or get help when things go wrong.. Language barriers and unclear design only add to the uncertainty.

Many AI tools are built in English-first environments, with limited Thai-language optimisation or cultural context. In rural areas or among older populations, this can create friction and resistance, even when the underlying system works well. Without transparency, user control, or recourse, AI tools risk being seen as alienating rather than empowering.

To build public confidence, AI deployments must prioritise explainability, Thai-language usability, and built-in pathways for human support. This includes interface localisation, clear model intent statements, and fallback mechanisms. Trust will not be built through performance alone, it must be earned through transparency, accessibility, and responsiveness.

Theme 5: Embedding Governance to Sustain Smart Urban Growth

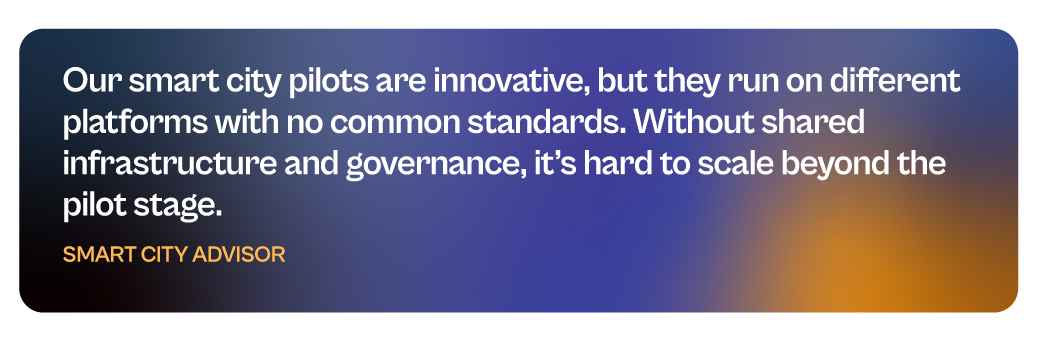

Thailand has made significant headway in its smart city development agenda, with over 30 provinces participating in the national Smart City program. Flagship initiatives in Phuket, Chiang Mai, Khon Kaen, and parts of the EEC have introduced smart traffic systems, e-governance tools, environmental monitoring, and digital tourism platforms.

However, many smart city projects are still pilots, driven by local champions, reliant on short-term grants, and lacking long-term governance structures. Fragmented data, unclear stakeholder roles, and limited collaboration between cities continue to slow scale and national replication.

The Smart City Office under DEPA is working to address these challenges by developing standard frameworks, urban data platforms, and public-private investment models. To maintain momentum, Thailand will need to embed smart city governance in multi-year digital urban strategies, establish shared infrastructure foundations, and invest in capacity-building for local leaders.

For smart cities to succeed, they must move beyond tech demonstrations and deliver real, lasting improvements in liveability, safety, and economic opportunity.

Sustaining Momentum in a Connected Nation

Thailand’s digital future won’t be defined by policy or technology alone; but by how effectively the country aligns infrastructure, skills, services, and trust at scale. The foundations are already being built in classrooms, city halls, data centres, and boardrooms. The real opportunity lies in weaving these efforts into a cohesive, resilient digital fabric. Lasting impact will come not just from momentum, but from turning vision into everyday value for people, communities, and businesses alike.

Leaders Roundtable: Beyond the Breach: Building a Resilient and Innovative Bank

We’ve concluded another successful event! Thanks to everyone for their Valuable contributions.

->Click here to explore hightlights and key takeaways from this Roundtable session.

The global data protection landscape is growing increasingly complex. With the proliferation of privacy laws across jurisdictions, organisations face a daunting challenge in ensuring compliance.

From the foundational GDPR, the evolving US state-level regulations, to new regulations in emerging markets, businesses with cross-border presence must navigate a maze of requirements to protect consumer data. This complexity, coupled with the rapid pace of regulatory change, requires proactive and strategic approaches to data management and protection.

GDPR: The Catalyst for Global Data Privacy

At the forefront of this global push for data privacy stands the General Data Protection Regulation (GDPR) – a landmark legislation that has reshaped data governance both within the EU and beyond. It has become a de facto standard for data management, influencing the creation of similar laws in countries like India, China, and regions such as Southeast Asia and the US.

However, the GDPR is evolving to tackle new challenges and incorporate lessons from past data breaches. Amendments aim to enhance enforcement, especially in cross-border cases, expedite complaint handling, and strengthen breach penalties. Amendments to the GDPR in 2024 focus on improving enforcement efficiency. The One-Stop-Shop mechanism will be strengthened for better handling of cross-border data processing, with clearer guidelines for lead supervisory authority and faster information sharing. Deadlines for cross-border decisions will be shortened, and Data Protection Authorities (DPAs) must cooperate more closely. Rules for data transfers to third countries will be clarified, and DPAs will have stronger enforcement powers, including higher fines for non-compliance.

For organisations, these changes mean increased scrutiny and potential penalties due to faster investigations. Improved DPA cooperation can lead to more consistent enforcement across the EU, making it crucial to stay updated and adjust data protection practices. While aiming for more efficient GDPR enforcement, these changes may also increase compliance costs.

GDPR’s Global Impact: Shaping Data Privacy Laws Worldwide

Despite being drafted by the EU, the GDPR has global implications, influencing data privacy laws worldwide, including in Canada and the US.

Canada’s Personal Information Protection and Electronic Documents Act (PIPEDA) governs how the private sector handles personal data, emphasising data minimisation and imposing fines of up to USD 75,000 for non-compliance.

The US data protection landscape is a patchwork of state laws influenced by the GDPR and PIPEDA. The California Privacy Rights Act (CPRA) and other state laws like Virginia’s CDPA and Colorado’s CPA reflect GDPR principles, requiring transparency and limiting data use. Proposed federal legislation, such as the American Data Privacy and Protection Act (ADPPA), aims to establish a national standard similar to PIPEDA.

The GDPR’s impact extends beyond EU borders, significantly influencing data protection laws in non-EU European countries. Countries like Switzerland, Norway, and Iceland have closely aligned their regulations with GDPR to maintain data flows with the EU. Switzerland, for instance, revised its Federal Data Protection Act to ensure compatibility with GDPR standards. The UK, post-Brexit, retained a modified version of GDPR in its domestic law through the UK GDPR and Data Protection Act 2018. Even countries like Serbia and North Macedonia, aspiring for EU membership, have modeled their data protection laws on GDPR principles.

Data Privacy: A Local Flavour in Emerging Markets

Emerging markets are recognising the critical need for robust data protection frameworks. These countries are not just following in the footsteps of established regulations but are creating laws that address their unique economic and cultural contexts while aligning with global standards.

Brazil has over 140 million internet users – the 4th largest in the world. Any data collection or processing within the country is protected by the Lei Geral de Proteção de Dados (or LGPD), even from data processors located outside of Brazil. The LGPD also mandates organisations to appoint a Data Protection Officer (DPO) and establishes the National Data Protection Authority (ANPD) to oversee compliance and enforcement.

Saudi Arabia’s Personal Data Protection Law (PDPL) requires explicit consent for data collection and use, aligning with global norms. However, it is tailored to support Saudi Arabia’s digital transformation goals. The PDPL is overseen by the Saudi Data and Artificial Intelligence Authority (SDAIA), linking data protection with the country’s broader AI and digital innovation initiatives.

Closer Home: Changes in Asia Pacific Regulations

The Asia Pacific region is experiencing a surge in data privacy regulations as countries strive to protect consumer rights and align with global standards.

Japan. Japan’s Act on the Protection of Personal Information (APPI) is set for a major overhaul in 2025. Certified organisations will have more time to report data breaches, while personal data might be used for AI training without consent. Enhanced data rights are also being considered, giving individuals greater control over biometric and children’s data. The government is still contemplating the introduction of administrative fines and collective action rights, though businesses have expressed concerns about potential negative impacts.

South Korea. South Korea has strengthened its data protection laws with significant amendments to the Personal Information Protection Act (PIPA), aiming to provide stronger safeguards for individual personal data. Key changes include stricter consent requirements, mandatory breach notifications within 72 hours, expanded data subject rights, refined data processing guidelines, and robust safeguards for emerging technologies like AI and IoT. There are also increased penalties for non-compliance.

China. China’s Personal Information Protection Law (PIPL) imposes stringent data privacy controls, emphasising user consent, data minimisation, and restricted cross-border data transfers. Severe penalties underscore the nation’s determination to safeguard personal information.

Southeast Asia. Southeast Asian countries are actively enhancing their data privacy landscapes. Singapore’s PDPA mandates breach notifications and increased fines. Malaysia is overhauling its data protection law, while Thailand’s PDPA has also recently come into effect.

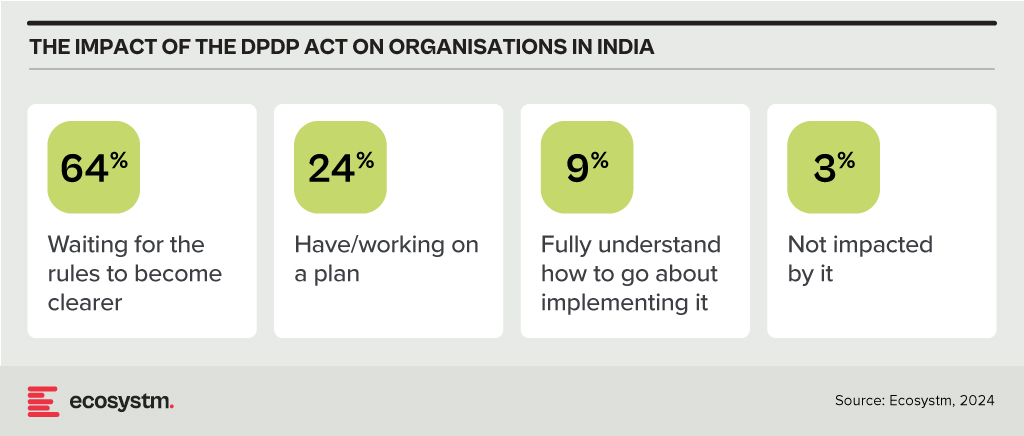

Spotlight: India’s DPDP Act

The Digital Personal Data Protection Act, 2023 (DPDP Act), officially notified about a year ago, is anticipated to come into effect soon. This principles-based legislation shares similarities with the GDPR and applies to personal data that identifies individuals, whether collected digitally or digitised later. It excludes data used for personal or domestic purposes, aggregated research data, and publicly available information. The Act adopts GDPR-like territorial rules but does not extend to entities outside India that monitor behaviour within the country.

Consent under the DPDP Act must be free, informed, and specific, with companies required to provide a clear and itemised notice. Unlike the GDPR, the Act permits processing without consent for certain legitimate uses, such as legal obligations or emergencies. It also categorises data fiduciaries based on the volume and sensitivity of the data they handle, imposing additional obligations on significant data fiduciaries while offering exemptions for smaller entities. The Act simplifies cross-border data transfers compared to the GDPR, allowing transfers to all countries unless restricted by the Indian Government. It also provides broad exemptions to the State for data processing under specific conditions. Penalties for breaches are turnover agnostic, with considerations for breach severity and mitigating actions. The full impact of the DPDP Act will be clearer once the rules are finalised and the Board becomes operational, but 97% of Indian organisations acknowledge that it will affect them.

Conclusion

Data breaches pose significant risks to organisations, requiring a strong data protection strategy that combines technology and best practices. Key technological safeguards include encryption, identity access management (IAM), firewalls, data loss prevention (DLP) tools, tokenisation, and endpoint protection platforms (EPP). Along with technology, organisations should adopt best practices such as inventorying and classifying data, minimising data collection, maintaining transparency with customers, providing choices, and developing comprehensive privacy policies. Training employees and designing privacy-focused processes are also essential. By integrating robust technology with informed human practices, organisations can enhance their overall data protection strategy.

Governments worldwide struggle with intricate social, economic, and environmental challenges. Tight budgets often leave them with limited resources to address these issues head-on. However, innovation offers a powerful path forward.

By embracing new technologies, adapting to cultural shifts, and fostering new skills, structures, and communication methods, governments can find solutions within existing constraints.

Find out how public sector innovation is optimising internal operations, improving service accessibility, bridging the financial gap, transforming healthcare, and building a sustainable future.

Click here to download ‘Innovation in Government: Social, Economic, and Environmental Wins’ as a PDF

Optimising Operations: Tech-Driven Efficiency

Technology is transforming how governments operate, boosting efficiency and allowing employees to focus on core functions.

Here are some real-world examples.

Singapore Streamlines Public Buses. A cloud-based fleet management system by the Land Transport Authority (LTA) improves efficiency, real-time tracking, data analysis, and the transition to electric buses.

Dubai Optimises Utilities Through AI. The Dubai Electricity and Water Authority (DEWA) leverages AI for predictive maintenance, demand forecasting, and grid management. This enhances service reliability, operational efficiency, and resource allocation for power and water utilities.

Automation Boosts Hospital Efficiency. Singapore hospitals are using automation to save man-hours and boost efficiency. Tan Tock Seng Hospital automates bacteria sample processing, increasing productivity without extra staff, while Singapore General Hospital tracks surgical instruments digitally, saving thousands of man-hours.

Tech for Citizens

Digital tools and emerging technologies hold immense potential to improve service accessibility and delivery for citizens. Here’s how governments are leveraging tech to benefit their communities.

Faster Cross-Border Travel. Malaysia’s pilot QR code clearance system expedites travel for factory workers commuting to Singapore, reducing congestion at checkpoints.

Metaverse City Planning. South Korea’s “Metaverse 120 Center” allows residents to interact with virtual officials and access services in a digital environment, fostering innovative urban planning and infrastructure management.

Streamlined Benefits. UK’s HM Revenue and Customs (HMRC) launched an online child benefit claim system that reduces processing time from weeks to days, showcasing the efficiency gains possible through digital government services.

Bridging the Financial Gap

Nearly 1.7 billion adults or one-third globally, remain unbanked.

However, innovative programs are bridging this gap and promoting financial inclusion.

Thailand’s Digital Wallet. Aimed at stimulating the economy and empowering underserved citizens, Thailand disburses USD 275 via digital wallets to 50 million low-income adults, fostering financial participation.

Ghana’s Digital Success Story. The first African nation to achieve 100% financial inclusion through modernised platforms like Ghana.gov and GhanaPay, which facilitate payments and fee collection through various digital channels.

Philippines Embraces QR Payments. The City of Alaminos leverages the Paleng-QR Ph Plus program to promote QR code-based payments, aligning with the central bank’s goal of onboarding 70% of Filipinos into the formal financial system by 2024.

Building a Sustainable Future

Governments around the world are increasingly turning to technology to address environmental challenges and preserve natural capital.

Here are some inspiring examples.

World’s Largest Carbon Capture Plant. Singapore and UCLA joined forces to build Equatic-1, a groundbreaking facility that removes CO2 from the ocean and creates carbon-negative hydrogen.

Tech-Enhanced Disaster Preparedness. The UK’s Lincolnshire County Council uses cutting-edge geospatial technology like drones and digital twins. This empowers the Lincolnshire Resilience Forum with real-time data and insights to effectively manage risks like floods and power outages across their vast region.

Smart Cities for Sustainability. Bologna, Italy leverages the digital twins of its city to optimise urban mobility and combat climate change. By analysing sensor data and incorporating social factors, the city is strategically developing infrastructure for cyclists and trams.

Tech for a Healthier Tomorrow

Technology is transforming healthcare delivery, promoting improved health and fitness monitoring.

Here’s a glimpse into how innovation is impacting patient care worldwide.

Robotic Companions for Seniors. South Korea tackles elder care challenges with robots. Companion robots and safety devices provide companionship and support for seniors living alone.

VR Therapy for Mental Wellness. The UAE’s Emirates Health Services Corporation implements a Virtual Reality Lab for Mental Health, that creates interactive therapy sessions for individuals with various psychological challenges. VR allows for personalised treatment plans based on data collected during sessions.

Southeast Asia’s massive workforce – 3rd largest globally – faces a critical upskilling gap, especially with the rise of AI. While AI adoption promises a USD 1 trillion GDP boost by 2030, unlocking this potential requires a future-proof workforce equipped with AI expertise.

Governments and technology providers are joining forces to build strong AI ecosystems, accelerating R&D and nurturing homegrown talent. It’s a tight race, but with focused investments, Southeast Asia can bridge the digital gap and turn its AI aspirations into reality.

Read on to find out how countries like Singapore, Thailand, Vietnam, and The Philippines are implementing comprehensive strategies to build AI literacy and expertise among their populations.

Download ‘Upskilling for the Future: Building AI Capabilities in Southeast Asia’ as a PDF

Big Tech Invests in AI Workforce

Southeast Asia’s tech scene heats up as Big Tech giants scramble for dominance in emerging tech adoption.

Microsoft is partnering with governments, nonprofits, and corporations across Indonesia, Malaysia, the Philippines, Thailand, and Vietnam to equip 2.5M people with AI skills by 2025. Additionally, the organisation will also train 100,000 Filipino women in AI and cybersecurity.

Singapore sets ambitious goal to triple its AI workforce by 2028. To achieve this, AWS will train 5,000 individuals annually in AI skills over the next three years.

NVIDIA has partnered with FPT Software to build an AI factory, while also championing AI education through Vietnamese schools and universities. In Malaysia, they have launched an AI sandbox to nurture 100 AI companies targeting USD 209M by 2030.

Singapore Aims to be a Global AI Hub

Singapore is doubling down on upskilling, global leadership, and building an AI-ready nation.

Singapore has launched its second National AI Strategy (NAIS 2.0) to solidify its global AI leadership. The aim is to triple the AI talent pool to 15,000, establish AI Centres of Excellence, and accelerate public sector AI adoption. The strategy focuses on developing AI “peaks of excellence” and empowering people and businesses to use AI confidently.

In keeping with this vision, the country’s 2024 budget is set to train workers who are over 40 on in-demand skills to prepare the workforce for AI. The country will also invest USD 27M to build AI expertise, by offering 100 AI scholarships for students and attracting experts from all over the globe to collaborate with the country.

Thailand Aims for AI Independence

Thailand’s ‘Ignite Thailand’ 2030 vision focuses on boosting innovation, R&D, and the tech workforce.

Thailand is launching the second phase of its National AI Strategy, with a USD 42M budget to develop an AI workforce and create a Thai Large Language Model (ThaiLLM). The plan aims to train 30,000 workers in sectors like tourism and finance, reducing reliance on foreign AI.

The Thai government is partnering with Microsoft to build a new data centre in Thailand, offering AI training for over 100,000 individuals and supporting the growing developer community.

Building a Digital Vietnam

Vietnam focuses on AI education, policy, and empowering women in tech.

Vietnam’s National Digital Transformation Programme aims to create a digital society by 2030, focusing on integrating AI into education and workforce training. It supports AI research through universities and looks to address challenges like addressing skill gaps, building digital infrastructure, and establishing comprehensive policies.

The Vietnamese government and UNDP launched Empower Her Tech, a digital skills initiative for female entrepreneurs, offering 10 online sessions on GenAI and no-code website creation tools.

The Philippines Gears Up for AI

The country focuses on investment, public-private partnerships, and building a tech-ready workforce.

With its strong STEM education and programming skills, the Philippines is well-positioned for an AI-driven market, allocating USD 30M for AI research and development.

The Philippine government is partnering with entities like IBPAP, Google, AWS, and Microsoft to train thousands in AI skills by 2025, offering both training and hands-on experience with cutting-edge technologies.

The strategy also funds AI research projects and partners with universities to expand AI education. Companies like KMC Teams will help establish and manage offshore AI teams, providing infrastructure and support.

To mitigate the challenges of cloud vendor lock-in, 44% of organisations in Thailand will prioritise data centre consolidation and infrastructure modernisation in 2024.

Explore the key trends impacting Thailand’s technology adoption. Keep an eye out for more data-backed insights on tech markets across Southeast Asia.

Technology is reshaping the Public Sector worldwide, optimising operations, improving citizen services, and fostering data-driven decision-making. Government agencies are also embracing innovation for effective governance in this digital era.

Public sector organisations worldwide recognise the need for swift and agile interventions. With citizen expectations resembling those of commercial customers, public sector organisations face mounting pressure to break down the barriers to provide seamless service experiences.

Read on to find out how public sector organisations in countries such as Australia, Vietnam, the Philippines, South Korea, and Singapore are innovating to stay ahead of the curve; and what Ecosystm VP Consulting, Peter Carr sees as the Future of Public Sector.

Click here to Download ‘The Future of the Public Sector’ as a PDF

Southeast Asia has evolved into an innovation hub with Singapore at the centre. The entrepreneurial and startup ecosystem has grown significantly across the region – for example, Indonesia now has the 5th largest number of startups in the world.

Organisations in the region are demonstrating a strong desire for tech-led innovation, innovation in experience delivery, and in evolving their business models to bring innovative products and services to market.

Here are 5 insights on the patterns of technology adoption in Southeast Asia, based on the findings of the Ecosystm Digital Enterprise Study, 2022.

- Data and AI investments are closely linked to business outcomes. There is a clear alignment between technology and business.

- Technology teams want better control of their infrastructure. Technology modernisation also focuses on data centre consolidation and cloud strategy

- Organisations are opting for a hybrid multicloud approach. They are not necessarily doing away with a ‘cloud first’ approach – but they have become more agnostic to where data is hosted.

- Cybersecurity underpins tech investments. Many organisations in the region do not have the maturity to handle the evolving threat landscape – and they are aware of it.

- Sustainability is an emerging focus area. While more effort needs to go in to formalise these initiatives, organisations are responding to market drivers.

More insights into the Southeast Asia tech market below.

Click here to download The Future of the Digital Enterprise – Southeast Asia as a PDF

Never before has the world experienced a shutdown in both supply and demand which has effectively slammed the brakes on economic activities and forced a complete rethink on how to continue doing business and maintain social interactions. The COVID-19 pandemic has accelerated digitalisation of consumers and enterprises and the telecommunications industry has been the pillar which has kept the world ticking over.

It is unthinkable just how the human race would have coped with such massive disruption, two decades ago in the absence of broadband internet. The technology and telecom sector has seen a rise in their visible importance in recent months. Various findings show that peak level traffic was about 20-30% higher than the levels before the pandemic. The rise in traffic coupled with the fervent growth of the digital economy augurs well for the technology and telecom sector in Southeast Asia.

Revenues Hit Despite Rise in Traffic

Unfortunately, the rise in network traffic has not translated to an increase in revenue for many operators in the region. The winners, that enjoyed YoY growth in Q1 2020 despite challenging circumstances were: Maxis (4.9%) and DiGi (3.4%) in Malaysia; dtac (3.3%) and True (5.7%) in Thailand; PDLT (7.5%) and Globe (1.4%) in the Philippines; and Indosat Ooredoo (7.9%) and XL Axiata (8.8%) in Indonesia. The telecom operators that struggled include: Celcom (-6.1%) and TM (-8.0%) in Malaysia; Singapore’s trio of Singtel (-6.5%), StarHub (-15.2%) and M1 (-10.3%); and AIS (-1.0%) in Thailand.

Key market trends include a dip in prepaid subscribers due to fall in tourist numbers, roaming income losses due to travel restrictions, and a general decline in average revenue per user (ARPU) due to weaker customer spend. The postpaid customer segment was resilient while the fixed broadband revenue stream was stable due to the increase in work from home (WFH) practices. With fixed tariffs, there are no incremental gains with an increase in usage. Voice revenue has been hit with the increase in collaboration-based communication applications such as Zoom and Microsoft Teams.

Equipment sales fell as global supply chains were severely disrupted and impacted new sign-ups of the more premium customers. Most markets in Southeast Asia depend on retail outlets as a key channel to the market, which has been hampered.

With the job losses across the world, bad debts and weakened customer spend is inevitable and it is imperative that the operators provide for reflective pricing strategies, listen to new customer requirements to ensure customer retention and strengthening of their market position. In May, Verizon’s CEO Hans Vestberg said nearly 800,000 of their subscribers were unable to pay their monthly bills. Discussions with operators in Southeast Asia also highlighted this as a current concern.

Enterprise Segment Target for New Growth

Ecosystm research shows that enterprises in Southeast Asia are increasingly considering telecom operators as go-to-market partners (Figure 1). Enterprises are demanding more than just devices and connectivity and with the fervent digital transformation (DX) efforts underway, services such as managed services, business application services, cybersecurity and network services are in demand. Technology vendors have an opportunity to partner with the right telecom operator in each market to enhance their IT market offerings, ahead of the 5G rollouts.

The broad 5G ecosystem inculcates cross-sector innovation and greater collaboration leading to new business models and exciting new opportunities. Singtel is the leading operator in the region and has the enterprise segment contributing approximately 65% to its revenue in its domestic market. In the World Communications Award 2019, Singtel won both “Best Enterprise Service” and “The Broadband Pioneer” awards. This places Singtel in a fine position to capitalise on the 5G enterprise services.

5G Needed Now More Than Ever

The pandemic has seen a rise in network traffic, onboarding of the digital customer and rapid DX of businesses which has whetted the appetite for faster broadband speeds and new services. Southeast Asia countries stand to profit from the trade war between the US and China and 5G features of low latency and higher security can boost adoption of IoT, Smart Manufacturing and broader Industry 4.0 goals to drive the economy.

Fixed Wireless in Southeast Asia is expected to be very popular considering the low penetration of fibre to the home (with the exception of Singapore) and will provide enterprises with a viable secondary connection to the internet. Popular applications – including video streaming and gaming – which are speed, latency and volume hungry will also be a target market for operators. Mobile operators that do not have a fixed broadband offering can enter this space and provide a serious “wireless fibre” alternative to homes and businesses.

Governments and telecom regulators ought to make spectrum available to the major telecom operators as soon as possible in order to ensure that the cutting edge 5G communications services are made available to consumers and businesses. Many experts believe 5G can raise the competitiveness of a nation.

Recent research from World Economic Forum (WEF) has found that significant economic and social value can be gained from the widespread deployment of 5G networks, with 5G facilitating industrial advances, productivity and improving the bottom line while enabling sustainable cities and communities. GSMA notes that mobile technologies and services in the wider Asia Pacific region generated USD 1.6 trillion of economic value while the mobile ecosystem supported 18 million jobs as well as contributing USD 180 billion of funding to the public sector through taxation.

US-China Trade War Threatens to Change Equipment Supplier Landscape

Despite severe pressures caused by the US-China trade war, Huawei posted an impressive 13.1% YoY growth in 1H 2020 registering revenue of USD 64.88 billion. Both Huawei and ZTE generate approximately 60% of their business from their domestic markets which is critical with the current unfavourable global sentiments. Huawei has diversified its business and built its consumer devices business which should withstand the disruptions caused by the political challenges.

Ericsson and Nokia stand to benefit from Huawei’s current global position and this was evident with the wins for the 5G contracts by Singtel and JVCo (Singtel and M1). The JVCo announced it selected Nokia to build the Radio Access Network (RAN) for the 5G standalone (SA) mmWave network infrastructure in the 3.5GHz radio frequency band. Singtel selected Ericsson to provide for the RAN on the same mmWave network.

However, while there is an opportunity for NEC and Samsung to join the party, Huawei is expected to do well in most other countries in Southeast Asia.

The Rise of the Digital Economy in Southeast Asia

A recent Google report valued the internet economy in Southeast Asia at USD 100 billion in 2019, more than tripling since 2015, and the sector is expected to hit USD 300 billion in 2025. With a population of approximately 570 million people, the region has some of the fastest-growing internet economies in the world.

The Indonesia market is the largest in the region and is expected to hit USD 133 billion from USD 40 billion in 2025. Indonesia’s lack of a world-class telecom infrastructure coupled with their slowness in 5G adoption has not impeded the country’s attractiveness for global technology investors who see the 270 million population as an immense opportunity. US tech giants, Facebook, Google, and PayPal have invested in Indonesia to reap the benefits from the growing digital economy powered by unicorns such as Gojek, Bukalapak, Tokopedia. In June 2020, Google Cloud launched in Jakarta, only the second in the region after Singapore with the four big unicorns being anchor customers.

In 2025, Google predicts Thailand to be the second-largest internet economy worth USD 50 billion. The internet economy for Singapore, Malaysia and the Philippines are estimated to be over USD 27 billion each. Shopee and Lazada are the top eCommerce apps in the region and have seen an increase in sales due to the disruption in the Retail industry. In-store shopping contributes to more than 50% of Retail in Singapore and Malaysia – this provides a tremendous opportunity for eCommerce players.

While movement restrictions are gradually being lifted, some things may never return where they were before COVID-19. Public debts have risen with numerous aids and handouts impacting economic growth forecast and rising unemployment is impacting customer spending power. On the plus side, DX of businesses and sharp onboarding of customers have redefined interactions, and sectors such as Education, are going online which will boost the digital economy. While the challenges are evident, exciting times are ahead for the technology and telecom sector in Southeast Asia.