Indonesia’s vast, diverse population and scattered islands create a unique landscape for AI adoption. Across sectors – from healthcare to logistics and banking to public services – leaders view AI not just as a tool for efficiency but as a means to expand reach, build resilience, and elevate citizen experience. With AI expected to add up to 12% of Indonesia’s GDP by 2030, it’s poised to be a core engine of growth.

Yet, ambition isn’t enough. While AI interest is high, execution is patchy. Many organisations remain stuck in isolated pilots or siloed experiments. Those scaling quickly face familiar hurdles: fragmented infrastructure, talent gaps, integration issues, and a lack of unified strategy and governance.

Ecosystm gathered insights and identified key challenges from senior tech leaders during a series of roundtables we moderated in Jakarta. The conversations revealed a clear picture of where momentum is building – and where obstacles continue to slow progress. From these discussions, several key themes emerged that highlight both opportunities and ongoing barriers in the country’s digital journey.

Theme 1. Digital Natives are Accelerating Innovation; But Need Scalable Guardrails

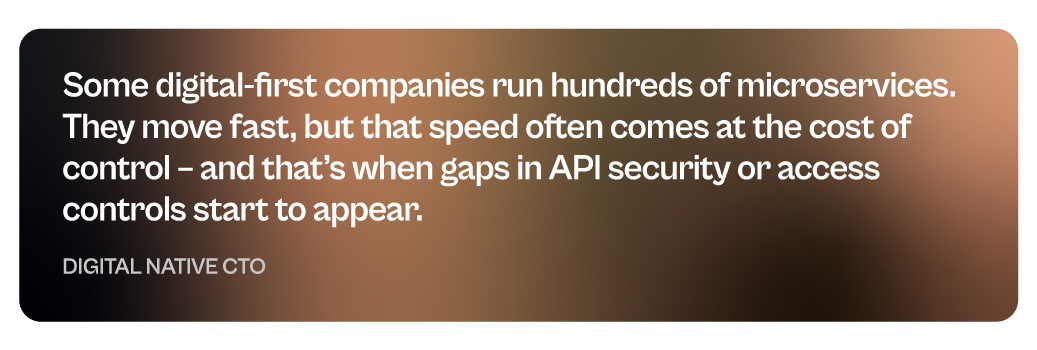

Indonesia’s digital-first companies – especially in fintech, logistics tech, and media streaming – are rapidly building on AI and cloud-native foundations. Players like GoTo, Dana, Jenius, and Vidio are raising the bar not only in customer experience but also in scaling technology across a mobile-first nation. Their use of AI for customer support, real-time fraud detection, biometric eKYC, and smart content delivery highlights the agility of digital-native models. This innovation is particularly concentrated in Jakarta and Bandung, where vibrant startup ecosystems and rich talent pools drive fast iteration.

Yet this momentum brings new risks. Deepfake attacks during onboarding, unsecured APIs, and content piracy pose real threats. Without the layered controls and regulatory frameworks typical of banks or telecom providers, many startups are navigating high-stakes digital terrain without a safety net.

As these companies become pillars of Indonesia’s digital economy, a new kind of guardrail is essential; flexible enough to support rapid growth, yet robust enough to mitigate systemic risk.

A sector-wide governance playbook, grounded in local realities and aligned with global standards, could provide the balance needed to scale both quickly and securely.

Theme 2. Scaling AI in Indonesia: Why Infrastructure Investment Matters

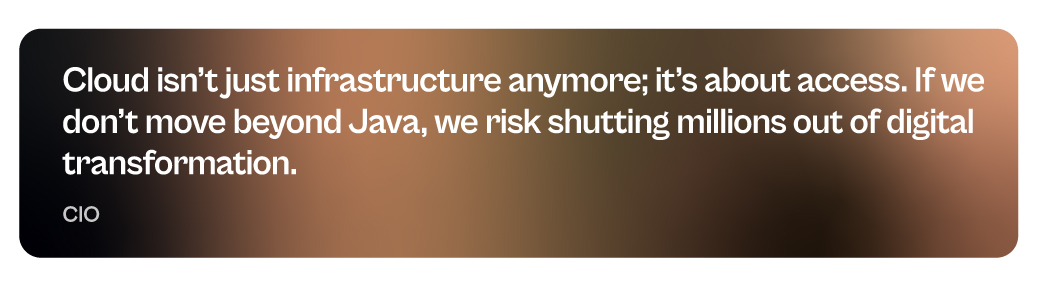

Indonesia’s ambition for AI is high, and while digital infrastructure still faces challenges, significant opportunities lie ahead. Although telecom investment has slowed and state funding tightened, growing momentum from global cloud players is beginning to reshape the landscape. AWS’s commitment to building cloud zones and edge locations beyond Java is a major step forward.

For AI to scale effectively across Indonesia’s diverse archipelago, the next wave of progress will depend on stronger investment incentives for data centres, cloud interconnects, and edge computing.

A proactive government role – through updated telecom regulations, streamlined permitting, and public-private partnerships – can unlock this potential.

Infrastructure isn’t just the backbone of digital growth; it’s a powerful lever for inclusion, enabling remote health services, quality education, and SME empowerment across even the most distant regions.

Theme 3. Cyber Resilience Gains Momentum; But Needs to Be More Holistic

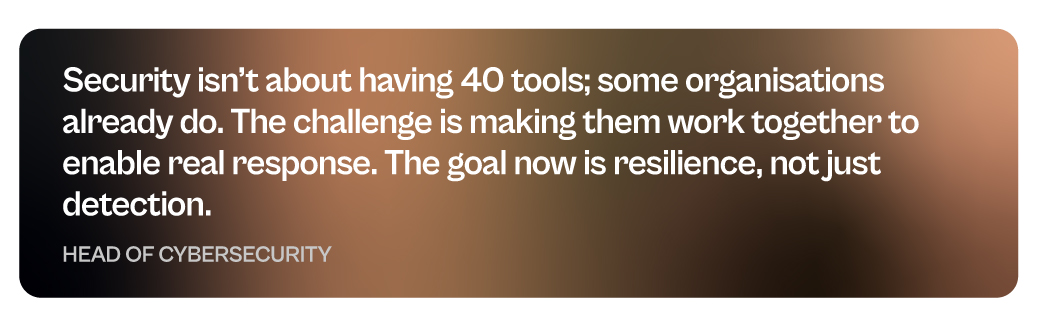

Indonesian organisations are facing an evolving wave of cyber threats – from sophisticated ransomware to DDoS attacks targeting critical services. This expanding threat landscape has elevated cyber resilience from a technical concern to a strategic imperative embraced by CISOs, boards, and risk committees alike. While many organisations invest heavily in security tools, the challenge remains in moving beyond fragmented solutions toward a truly resilient operating model that emphasises integration, simulation, and rapid response.

The shift from simply being “secure” to becoming genuinely “resilient” is gaining momentum. Resilience – captured by the Bahasa Indonesia term “ulet” – is now recognised as the ability not just to defend, but to endure disruption and bounce back stronger. Regulatory steps like OJK’s cyber stress testing and continuity planning requirements are encouraging organisations to go beyond mere compliance.

Organisations will now need to operationalise resilience by embedding it into culture through cross-functional drills, transparent crisis playbooks, and agile response practices – so when attacks strike, business impact is minimised and trust remains intact.

For many firms, especially in finance and logistics, this mindset and operational shift will be crucial to sustaining growth and confidence in a rapidly evolving digital landscape.

Theme 4. Organisations Need a Roadmap for Legacy System Transformation

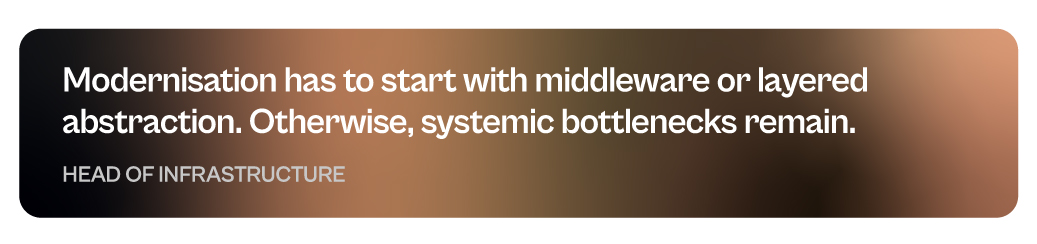

Legacy systems continue to slow modernisation efforts in traditional sectors such as banking, insurance, and logistics by creating both technical and organisational hurdles that limit innovation and scalability. These outdated IT environments are deeply woven into daily operations, making integration complex, increasing downtime risks, and frustrating cross-functional teams striving to deliver digital value swiftly. The challenge goes beyond technology – there’s often a disconnect between new digital initiatives and existing workflows, which leads to bottlenecks and slows progress.

Recognising these challenges, many organisations are now investing in middleware solutions, automation, and phased modernisation plans that focus on upgrading key components gradually. This approach helps bridge the gap between legacy infrastructure and new digital capabilities, reducing the risk of enterprise-wide disruption while enabling continuous innovation.

The crucial next step is to develop and commit to a clear, incremental roadmap that balances risk with progress – ensuring legacy systems evolve in step with digital ambitions and unlock the full potential of transformation.

Theme 5. AI Journey Must Be Rooted in Local Talent and Use Cases

Ecosystm research reveals that only 13% of Indonesian organisations have experimented with AI, with most yet to integrate it into their core strategies.

While Indonesia’s AI maturity remains uneven, there is a broad recognition of AI’s potential as a powerful equaliser – enhancing public service delivery across 17,000 islands, democratising diagnostics in rural healthcare, and improving disaster prediction for flood-prone Jakarta.

The government’s 2045 vision emphasises inclusive growth and differentiated human capital, but achieving these goals requires more than just infrastructure investment. Building local talent pipelines is critical. Initiatives like IBM’s AI Academy in Batam, which has trained over 2,000 AI practitioners, are promising early steps. However, scaling this impact means embedding AI education into national curricula, funding interdisciplinary research, and supporting SMEs with practical adoption toolkits.

The opportunity is clear: GenAI can act as an multiplier, empowering even resource-constrained sectors to enhance reach, personalisation, and citizen engagement.

To truly unlock AI’s potential, Indonesia must move beyond imported templates and focus on developing grounded, context-aware AI solutions tailored to its unique landscape.

From Innovation to Impact

Indonesia’s tech journey is at a pivotal inflection point – where ambition must transform into alignment, and isolated pilots must scale into robust platforms. Success will depend not only on technology itself but on purpose-driven strategy, resilient infrastructure, cultural readiness, and shared accountability across industries. The future won’t be shaped by standalone innovations, but by coordinated efforts that convert experimentation into lasting, systemic impact.

Leaders Roundtable: Beyond the Breach: Building a Resilient and Innovative Bank

We’ve concluded another successful event! Thanks to everyone for their Valuable contributions.

->Click here to explore hightlights and key takeaways from this Roundtable session.

Despite an increase in energy efficiency investment, the construction sector’s energy consumption and CO₂ emissions have rebounded to an all-time high. Buildings currently contribute 39% of global energy-related carbon emissions – 28% from operational needs like heating and cooling, and 11% from construction materials.

In the next three decades, with the global population expected to reach 9.7 billion, the construction industry will face the pressure to meet growing infrastructure and housing demands while adapting to stricter environmental regulations.

The urgency of climate action demands that governments mandate low-carbon practices in urban development.

Increase Use of Low-Carbon Materials

Traditional building materials like concrete, steel, and brick are strong and durable but environmentally costly. This high embodied carbon footprint is prompting a shift towards low-carbon alternatives. Indonesia is using ‘green cement’ – made using environmentally friendly materials – in the development of its new futuristic capital Nusantara. This has led to an estimated reduction in carbon emissions of up to 38% per tonne of cement so far.

Nordic countries are setting ambitious targets for low-carbon materials. Starting in 2025, Finland will require life cycle assessments and material declarations in construction to reduce emissions, detailing building components and material origins. Denmark is also prioritising low-carbon materials through energy-efficient designs, sustainable materials, and stringent building codes.

Mandate Whole-Life Carbon Emission Assessments

Whole Life-Cycle Carbon (WLC) emissions encompass all the carbon a building generates throughout its lifespan, from material extraction to demolition and disposal. Assessing WLC gives a comprehensive understanding of a building’s total environmental impact.

The London Plan is a roadmap for future development and achieving the goal of a zero-carbon city. The plan includes provisions for WLC analysis, specific energy hierarchies, and strategies to reduce London’s carbon footprint.

With a bold vision of a fully circular city by 2050, the Amsterdam Circular Strategy 2020-2025 lays out a comprehensive roadmap to achieve this goal. Key elements include mapping material flows to reduce reliance on virgin resources and mandating WLC assessments.

Enforce Clean Construction Standards

From green building codes to tax incentives, governments around the world are implementing innovative strategies to encourage sustainable building practices.

The Philippines’ National Building Code requires green building standards and energy efficiency measures for new buildings.

Seattle offers expedited permits for projects meeting embodied carbon standards, speeding up eco-friendly construction, and reinforcing the city’s environmental goals.

New Jersey offers businesses a tax credit of up to 5% for using low-carbon concrete and an additional 3% for concrete made with carbon capture technology.

Promote Large-Scale Adaptive Reuse

Large-scale adaptive reuse includes reducing carbon emissions by making existing buildings and infrastructure a larger part of the climate solution.

London’s Battersea Power Station restored its iconic chimneys and Art Deco façade, transforming it into a vibrant hub with residential, commercial, and leisure spaces.

The High Line in New York has been transformed into a public park with innovative landscaping, smart irrigation, and interactive art installations, enhancing visitor experience and sustainability.

Singapore using adaptive reuse to rejuvenate urban and industrial spaces sustainably. The Jurong Town Corporation is repurposing a terrace factory for sustainable redevelopment and preserving industrial heritage. In Queenstown, historical buildings in Tanglin Halt are being reused to maintain historical significance and add senior-friendly amenities.

Establish Circular Economy

As cities worldwide start exploring ways to go circular, some are already looking into different ways to leverage innovative practices to implement circular initiatives.

Toronto is embedding circular criteria into procurement by requiring circular economy profiles, vendor action plans, and encouraging circular design for parklets. The city also recommends actions for transitioning to a circular economy and is developing e-learning on circular procurement for staff.

Japan uses Building Information Modeling to optimise resource consumption and reduce waste during construction, with a focus on using recycled materials to promote sustainability in building projects.

Adopt Electric Vehicles

The share of EVs increased from 4% in 2020 to 18% in 2023 and is expected to grow in 2024. This trend reflects a global shift toward cleaner transportation, driven by technological advancements and rising environmental awareness.

The Delhi EV Policy aims to expand charging infrastructure and incentives, targeting 18,000 charging points by 2024, with 25% EV registrations and one charging outlet per 15 EVs citywide.

Singapore is adopting EVs to reduce land transport emissions as part of its net-zero goal, aiming to cut emissions by 1.5 to 2 million tonnes. The EV Roadmap targets cost parity with internal combustion engine (ICE) vehicles and 60,000 charging points by 2030.

Australia has set new rules to limit vehicle pollution, encouraging car makers to sell more electric vehicles and reduce transportation pollution.

Promote Circular Economy Marketplaces

Circular marketplaces play an important role in the new economy, changing the way we use, manufacture, and purpose materials and products.

The UK’s Material Reuse Portal aggregates surplus construction materials post-deconstruction, offering guidance and connections to service providers. It integrates with various data sources, can be customised for different locations, and provides free access to sustainable materials. Future plans include expanding marketplace partnerships to enhance material reuse.

Build Reuse is a US-based online marketplace specialising in salvaged and surplus building materials. It connects buyers and sellers for reclaimed items like wood, bricks, fixtures, and architectural elements, promoting resource efficiency and reducing construction waste.

Southeast Asia has evolved into an innovation hub with Singapore at the centre. The entrepreneurial and startup ecosystem has grown significantly across the region – for example, Indonesia now has the 5th largest number of startups in the world.

Organisations in the region are demonstrating a strong desire for tech-led innovation, innovation in experience delivery, and in evolving their business models to bring innovative products and services to market.

Here are 5 insights on the patterns of technology adoption in Southeast Asia, based on the findings of the Ecosystm Digital Enterprise Study, 2022.

- Data and AI investments are closely linked to business outcomes. There is a clear alignment between technology and business.

- Technology teams want better control of their infrastructure. Technology modernisation also focuses on data centre consolidation and cloud strategy

- Organisations are opting for a hybrid multicloud approach. They are not necessarily doing away with a ‘cloud first’ approach – but they have become more agnostic to where data is hosted.

- Cybersecurity underpins tech investments. Many organisations in the region do not have the maturity to handle the evolving threat landscape – and they are aware of it.

- Sustainability is an emerging focus area. While more effort needs to go in to formalise these initiatives, organisations are responding to market drivers.

More insights into the Southeast Asia tech market below.

Click here to download The Future of the Digital Enterprise – Southeast Asia as a PDF

The Financial Services industry (FSI) in Indonesia is increasingly investing in digital. This is driven by both user demand and governmental incentives. However, organisations can be at very different stages of their digital maturity. Some organisations are in the early transitional stages while others are investing to enhance capabilities, they started investments in long ago. An understanding of the digital maturity of a typical financial services organisation in Indonesia gives their industry peers an opportunity to benchmark their technology and digital roadmap.

FSI in Indonesia is intensely competitive with a large number of players. There is competition from the fintech start-up community that is increasing market size and has driven a growing reliance on digital. Why is creating an exceptional customer experience a key differentiator in this competitive market? What are the impacts of OJK regulations on customer data management? How can a financial organisation create a single customer view across multiple channels and deliver personalised marketing initiatives?

Read this whitepaper to find out how digital-savvy customers are driving transformation in the financial services industry in Indonesia including:

- The key business priorities for 2021

- The shift in engagement strategies and channels

- The dependence on technology to support their marketing strategy

Click below to download the whitepaper

(Clicking on this link will take you to the Sitecore website where you can download the whitepaper)

Organisations are increasingly investing in digital. However, they are at different stages of their digital maturity. Some companies are in the early transitional stages while others are investing to upgrade capabilities they instituted long ago. An understanding of the digital maturity of a typical organisation in your market/industry can help you benchmark your technology and. digital roadmap.

This ebook presents some key findings for financial services within Indonesia. You will get insights on impact of COVID-19 on transformation journeys, key business priorities for 2021, and the shift in engagement strategies and channels.

Click below to download the eBook

(Clicking on this link will take you to Sitecore website where you can download the eBook)

Never before has the world experienced a shutdown in both supply and demand which has effectively slammed the brakes on economic activities and forced a complete rethink on how to continue doing business and maintain social interactions. The COVID-19 pandemic has accelerated digitalisation of consumers and enterprises and the telecommunications industry has been the pillar which has kept the world ticking over.

It is unthinkable just how the human race would have coped with such massive disruption, two decades ago in the absence of broadband internet. The technology and telecom sector has seen a rise in their visible importance in recent months. Various findings show that peak level traffic was about 20-30% higher than the levels before the pandemic. The rise in traffic coupled with the fervent growth of the digital economy augurs well for the technology and telecom sector in Southeast Asia.

Revenues Hit Despite Rise in Traffic

Unfortunately, the rise in network traffic has not translated to an increase in revenue for many operators in the region. The winners, that enjoyed YoY growth in Q1 2020 despite challenging circumstances were: Maxis (4.9%) and DiGi (3.4%) in Malaysia; dtac (3.3%) and True (5.7%) in Thailand; PDLT (7.5%) and Globe (1.4%) in the Philippines; and Indosat Ooredoo (7.9%) and XL Axiata (8.8%) in Indonesia. The telecom operators that struggled include: Celcom (-6.1%) and TM (-8.0%) in Malaysia; Singapore’s trio of Singtel (-6.5%), StarHub (-15.2%) and M1 (-10.3%); and AIS (-1.0%) in Thailand.

Key market trends include a dip in prepaid subscribers due to fall in tourist numbers, roaming income losses due to travel restrictions, and a general decline in average revenue per user (ARPU) due to weaker customer spend. The postpaid customer segment was resilient while the fixed broadband revenue stream was stable due to the increase in work from home (WFH) practices. With fixed tariffs, there are no incremental gains with an increase in usage. Voice revenue has been hit with the increase in collaboration-based communication applications such as Zoom and Microsoft Teams.

Equipment sales fell as global supply chains were severely disrupted and impacted new sign-ups of the more premium customers. Most markets in Southeast Asia depend on retail outlets as a key channel to the market, which has been hampered.

With the job losses across the world, bad debts and weakened customer spend is inevitable and it is imperative that the operators provide for reflective pricing strategies, listen to new customer requirements to ensure customer retention and strengthening of their market position. In May, Verizon’s CEO Hans Vestberg said nearly 800,000 of their subscribers were unable to pay their monthly bills. Discussions with operators in Southeast Asia also highlighted this as a current concern.

Enterprise Segment Target for New Growth

Ecosystm research shows that enterprises in Southeast Asia are increasingly considering telecom operators as go-to-market partners (Figure 1). Enterprises are demanding more than just devices and connectivity and with the fervent digital transformation (DX) efforts underway, services such as managed services, business application services, cybersecurity and network services are in demand. Technology vendors have an opportunity to partner with the right telecom operator in each market to enhance their IT market offerings, ahead of the 5G rollouts.

The broad 5G ecosystem inculcates cross-sector innovation and greater collaboration leading to new business models and exciting new opportunities. Singtel is the leading operator in the region and has the enterprise segment contributing approximately 65% to its revenue in its domestic market. In the World Communications Award 2019, Singtel won both “Best Enterprise Service” and “The Broadband Pioneer” awards. This places Singtel in a fine position to capitalise on the 5G enterprise services.

5G Needed Now More Than Ever

The pandemic has seen a rise in network traffic, onboarding of the digital customer and rapid DX of businesses which has whetted the appetite for faster broadband speeds and new services. Southeast Asia countries stand to profit from the trade war between the US and China and 5G features of low latency and higher security can boost adoption of IoT, Smart Manufacturing and broader Industry 4.0 goals to drive the economy.

Fixed Wireless in Southeast Asia is expected to be very popular considering the low penetration of fibre to the home (with the exception of Singapore) and will provide enterprises with a viable secondary connection to the internet. Popular applications – including video streaming and gaming – which are speed, latency and volume hungry will also be a target market for operators. Mobile operators that do not have a fixed broadband offering can enter this space and provide a serious “wireless fibre” alternative to homes and businesses.

Governments and telecom regulators ought to make spectrum available to the major telecom operators as soon as possible in order to ensure that the cutting edge 5G communications services are made available to consumers and businesses. Many experts believe 5G can raise the competitiveness of a nation.

Recent research from World Economic Forum (WEF) has found that significant economic and social value can be gained from the widespread deployment of 5G networks, with 5G facilitating industrial advances, productivity and improving the bottom line while enabling sustainable cities and communities. GSMA notes that mobile technologies and services in the wider Asia Pacific region generated USD 1.6 trillion of economic value while the mobile ecosystem supported 18 million jobs as well as contributing USD 180 billion of funding to the public sector through taxation.

US-China Trade War Threatens to Change Equipment Supplier Landscape

Despite severe pressures caused by the US-China trade war, Huawei posted an impressive 13.1% YoY growth in 1H 2020 registering revenue of USD 64.88 billion. Both Huawei and ZTE generate approximately 60% of their business from their domestic markets which is critical with the current unfavourable global sentiments. Huawei has diversified its business and built its consumer devices business which should withstand the disruptions caused by the political challenges.

Ericsson and Nokia stand to benefit from Huawei’s current global position and this was evident with the wins for the 5G contracts by Singtel and JVCo (Singtel and M1). The JVCo announced it selected Nokia to build the Radio Access Network (RAN) for the 5G standalone (SA) mmWave network infrastructure in the 3.5GHz radio frequency band. Singtel selected Ericsson to provide for the RAN on the same mmWave network.

However, while there is an opportunity for NEC and Samsung to join the party, Huawei is expected to do well in most other countries in Southeast Asia.

The Rise of the Digital Economy in Southeast Asia

A recent Google report valued the internet economy in Southeast Asia at USD 100 billion in 2019, more than tripling since 2015, and the sector is expected to hit USD 300 billion in 2025. With a population of approximately 570 million people, the region has some of the fastest-growing internet economies in the world.

The Indonesia market is the largest in the region and is expected to hit USD 133 billion from USD 40 billion in 2025. Indonesia’s lack of a world-class telecom infrastructure coupled with their slowness in 5G adoption has not impeded the country’s attractiveness for global technology investors who see the 270 million population as an immense opportunity. US tech giants, Facebook, Google, and PayPal have invested in Indonesia to reap the benefits from the growing digital economy powered by unicorns such as Gojek, Bukalapak, Tokopedia. In June 2020, Google Cloud launched in Jakarta, only the second in the region after Singapore with the four big unicorns being anchor customers.

In 2025, Google predicts Thailand to be the second-largest internet economy worth USD 50 billion. The internet economy for Singapore, Malaysia and the Philippines are estimated to be over USD 27 billion each. Shopee and Lazada are the top eCommerce apps in the region and have seen an increase in sales due to the disruption in the Retail industry. In-store shopping contributes to more than 50% of Retail in Singapore and Malaysia – this provides a tremendous opportunity for eCommerce players.

While movement restrictions are gradually being lifted, some things may never return where they were before COVID-19. Public debts have risen with numerous aids and handouts impacting economic growth forecast and rising unemployment is impacting customer spending power. On the plus side, DX of businesses and sharp onboarding of customers have redefined interactions, and sectors such as Education, are going online which will boost the digital economy. While the challenges are evident, exciting times are ahead for the technology and telecom sector in Southeast Asia.