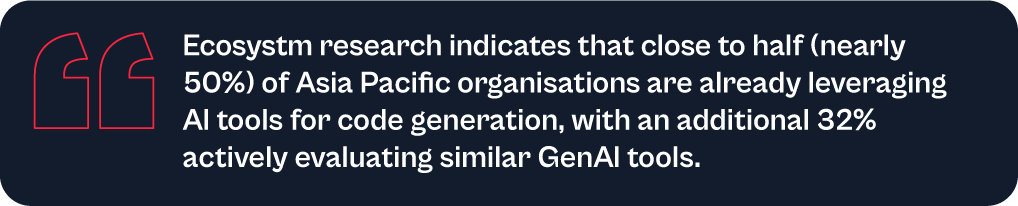

AI tools have become a game-changer for the technology industry, enhancing developer productivity and software quality. Leveraging advanced machine learning models and natural language processing, these tools offer a wide range of capabilities, from code completion to generating entire blocks of code, significantly reducing the cognitive load on developers. AI-powered tools not only accelerate the coding process but also ensure higher code quality and consistency, aligning seamlessly with modern development practices. Organisations are reaping the benefits of these tools, which have transformed the software development lifecycle.

Impact on Developer Productivity

AI tools are becoming an indispensable part of software development owing to their:

- Speed and Efficiency. AI-powered tools provide real-time code suggestions, which dramatically reduces the time developers spend writing boilerplate code and debugging. For example, Tabnine can suggest complete blocks of code based on the comments or a partial code snippet, which accelerates the development process.

- Quality and Accuracy. By analysing vast datasets of code, AI tools can offer not only syntactically correct but also contextually appropriate code suggestions. This capability reduces bugs and improves the overall quality of the software.

- Learning and Collaboration. AI tools also serve as learning aids for developers by exposing them to new or better coding practices and patterns. Novice developers, in particular, can benefit from real-time feedback and examples, accelerating their professional growth. These tools can also help maintain consistency in coding standards across teams, fostering better collaboration.

Advantages of Using AI Tools in Development

- Reduced Time to Market. Faster coding and debugging directly contribute to shorter development cycles, enabling organisations to launch products faster. This reduction in time to market is crucial in today’s competitive business environment where speed often translates to a significant market advantage.

- Cost Efficiency. While there is an upfront cost in integrating these AI tools, the overall return on investment (ROI) is enhanced through the reduced need for extensive manual code reviews, decreased dependency on large development teams, and lower maintenance costs due to improved code quality.

- Scalability and Adaptability. AI tools learn and adapt over time, becoming more efficient and aligned with specific team or project needs. This adaptability ensures that the tools remain effective as the complexity of projects increases or as new technologies emerge.

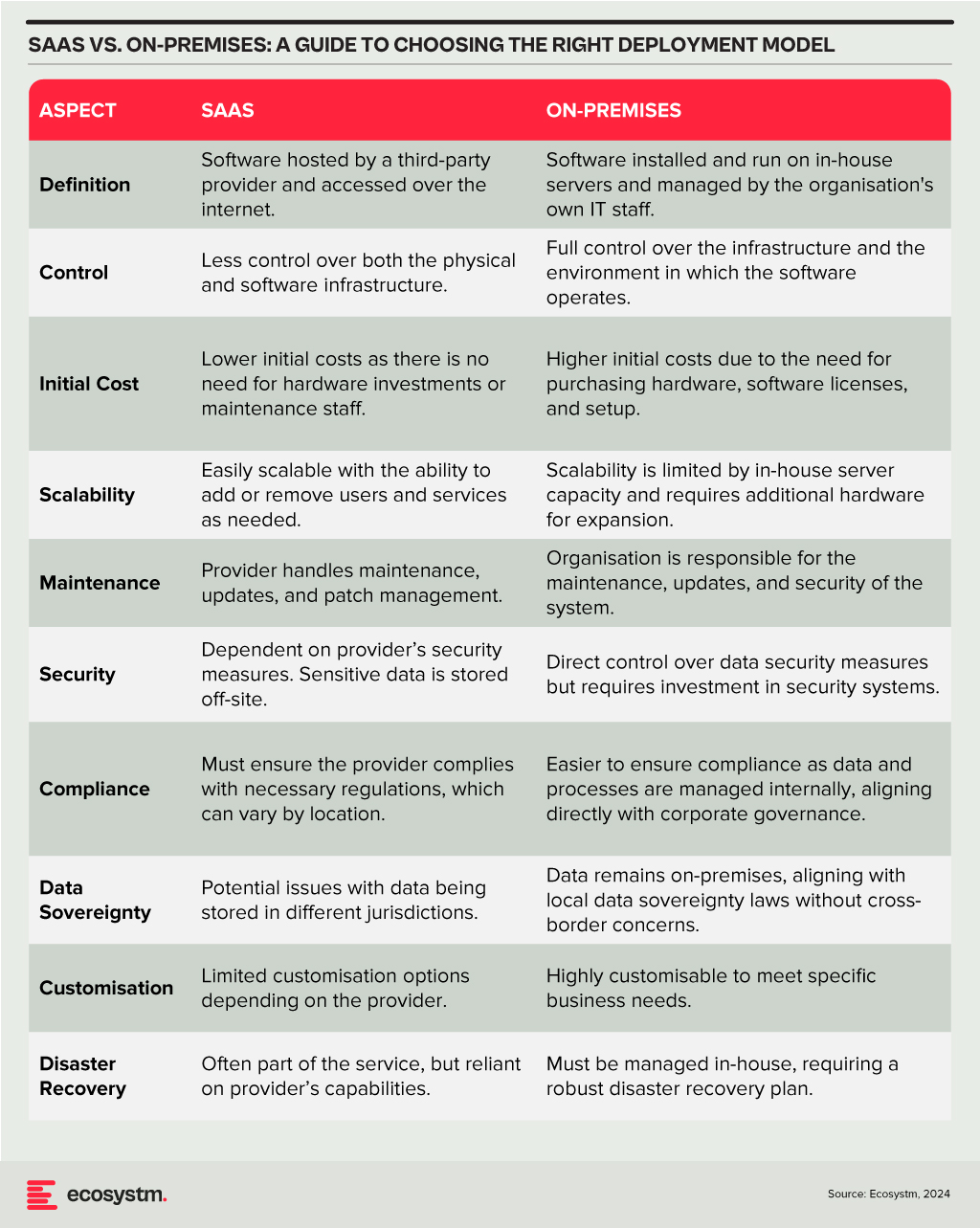

Deployment Models

The choice between SaaS and on-premises deployment models involves a trade-off between control, cost, and flexibility. Organisations need to consider their specific requirements, including the level of control desired over the infrastructure, sensitivity of the data, compliance needs, and available IT resources. A thorough assessment will guide the decision, ensuring that the deployment model chosen aligns with the organisation’s operational objectives and strategic goals.

Technology teams must consider challenges such as the reliability of generated code, the potential for generating biased or insecure code, and the dependency on external APIs or services. Proper oversight, regular evaluations, and a balanced integration of AI tools with human oversight are recommended to mitigate these risks.

A Roadmap for AI Integration

The strategic integration of AI tools in software development offers a significant opportunity for companies to achieve a competitive edge. By starting with pilot projects, organisations can assess the impact and utility of AI within specific teams. Encouraging continuous training in AI advancements empowers developers to leverage these tools effectively. Regular audits ensure that AI-generated code adheres to security standards and company policies, while feedback mechanisms facilitate the refinement of tool usage and address any emerging issues.

Technology teams have the opportunity to not only boost operational efficiency but also cultivate a culture of innovation and continuous improvement in their software development practices. As AI technology matures, even more sophisticated tools are expected to emerge, further propelling developer capabilities and software development to new heights.

In this Insight, guest author Anupam Verma talks about the technology-led evolution of the Banking industry in India and offers Cloud Service Providers guidance on how to partner with banks and financial institutions. “It is well understood that the banks that were early adopters of cloud have clearly gained market share during COVID-19. Banks are keen to adopt cloud but need a partnership approach balancing innovation with risk management so that it is ‘not one step forward and two steps back’ for them.”

India has been witnessing a digital revolution. Rapidly rising mobile and internet penetration has created an estimated 1 billion mobile users and more than 600 million internet users. It has been reported that 99% of India’s adult population now has a digital identity in the form of Aadhar and a large proportion of the adult Indians have a bank account.

Indians are adapting to consume multiple services on the smartphone and are demanding the same from their financial services providers. COVID-19 has accelerated this digital trend beyond imagination and is transforming India from a data-poor to a data-rich nation. This data from various alternate sources coupled with traditional sources is the inflection point to the road to financial inclusion. Strong digital infrastructure and digital footprints will create a world of opportunities for incumbent banks, non-banks as well as new-age fintechs.

The Cloud Imperative for Banks

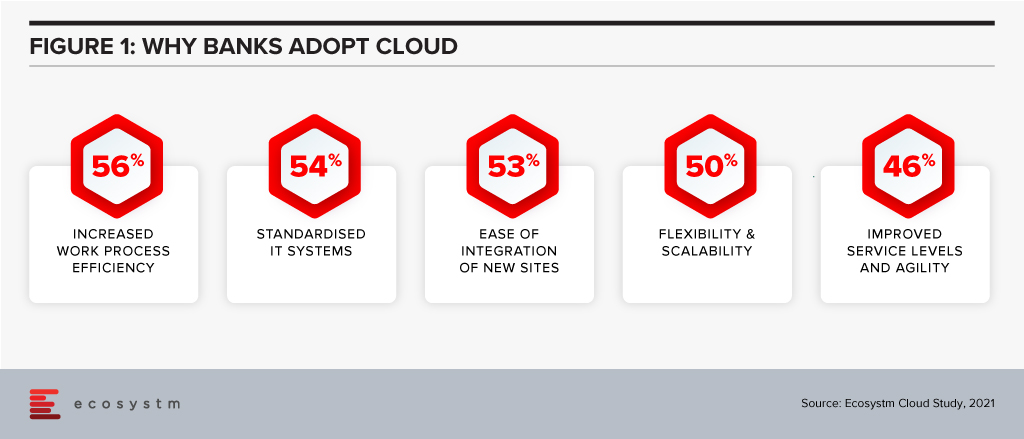

Banks today have an urgent need to stay relevant in the era of digitally savvy customers and rising fintechs. This journey for banks to survive and thrive will put Data Analytics and Cloud at the front and centre of their digital transformation.

A couple of years ago, banks viewed cloud as an outsourcing infrastructure to improve the cost curve. Today, banks are convinced that cloud provides many more advantages (Figure 1).

Banks are also increasingly partnering with fintechs for applications such as KYC, UI/UX and customer service. Fintechs are cloud-native and understand that cloud provides exponential innovation, speed to market, scalability, resilience, a better cost curve and security. They understand their business will not exist or reach scale if not for cloud. These bank-fintech partnerships are also making banks understand the cloud imperative.

Traditionally, banks in India have had concerns around data privacy and data sovereignty. There are also risks around migrating legacy systems, which are made of monolithic applications and do not have a service-oriented architecture. As a result, banks are now working on complete re-architecture of the core legacy systems. Banks are creating web services on top of legacy systems, which can talk to the new technologies. New applications being built are cloud ready. In fact, many applications may not connect to the core legacy systems. They are exploring moving customer interfaces, CRM applications and internal workflows to the cloud. Still early days, but banks are using cloud analytics for marketing campaigns, risk modelling and regulatory reporting.

The remote working world is irreversible, and banks also understand that cloud will form the backbone for internal communication, virtual desktops, and virtual collaboration.

Strategy for Cloud Service Providers (CSPs)

It is estimated that India’s public cloud services market is likely to become the largest market in the Asia Pacific behind only China, Australia, and Japan. Ecosystm research shows that 70% of banking organisations in India are looking to increase their cloud spending. Whichever way one looks at it, cloud is likely to remain a large and growing market. The Financial Services industry will be one of the prominent segments and should remain a focus for cloud service providers (CSPs).

I believe CSPs targeting India’s Banking industry should bucket their strategy under four key themes:

- Partnering to Innovate and co-create solutions. CSPs must work with each business within the bank and re-imagine customer journeys and process workflow. This would mean banking domain experts and engineering teams of CSPs working with relevant teams within the bank. For some customer journeys, the teams have to go back to first principles and start from scratch i.e the financial need of the customer and how it is being re-imagined and fulfilled in a digital world.

CSPs should also continue to engage with all ecosystem partners of banks to co-create cloud-native solutions. These partners could range from fintechs to vendors for HR, Finance, business reporting, regulatory reporting, data providers (which feeds into analytics engine).

CSPs should partner with banks for experimentation by providing test environments. Some of the themes that are critical for banks right now are CRM, workspace virtualisation and collaboration tools. CSPs could leverage these themes to open the doors. API banking is another area for co-creating solutions. Core systems cannot be ‘lifted & shifted’ to the cloud. That would be the last mile in the digital transformation journey. - Partnering to mitigate ‘fear of the unknown’. As in the case of any key strategic shift, the tone of the executive management is important. A lot of engagement is required with the entire senior management team to build the ‘trust quotient’ of cloud. Understanding the benefits, risks, controls and the concept of ‘shared responsibility’ is important. I am an AWS Certified Cloud Practitioner and I realise how granular the security in the cloud can be (which is the responsibility of the bank and not of the CSP). This knowledge gap can be massive for smaller banks due to the non-availability of talent. If security in the cloud is not managed well, there is an immense risk to the banks.

- Partnering for Risk Mitigation. Regulators will expect banks to treat CSPs like any other outsourcing service providers. CSPs should work with banks to create robust cloud governance frameworks for mitigating cloud-related risks such as resiliency, cybersecurity etc. Adequate communication is required to showcase the controls around data privacy (data at rest and transit), data sovereignty, geographic diversity of Availability Zones (to mitigate risks around natural calamities like floods) and Disaster Recovery (DR) site.

- Partnering with Regulators. Building regulatory comfort is an equally important factor for the pace and extent of technology adoption in Financial Services. The regulators expect the banks to have a governance framework, detailed policies and operating guidelines covering assessment, contractual consideration, audit, inspection, change management, cybersecurity, exit plan etc. While partnering with regulators on creating the framework is important, it is equally important to demonstrate that banks have the skill sets to run the cloud and manage the risks. Engagement should also be linked to specific use cases which allow banks to effectively compete with fintech’s in the digital world (and expand financial access) and use cases for risk mitigation and fraud management. This would meet the regulator’s dual objective of market development as well as market stability.

Financial Services is a large and growing market for CSPs. Fintechs are cloud-native and certain sectors in the industry (like non-banks and insurance companies) have made progress in cloud adoption. It is well understood that the banks that were early adopters of cloud have clearly gained market share during COVID-19. Banks are keen to adopt cloud but need a partnership approach balancing innovation with risk management so that it is ‘not one step forward and two steps back’ for them.

The views and opinions mentioned in the article are personal.

Anupam Verma is part of the Leadership team at ICICI Bank and his responsibilities have included leading the Bank’s strategy in South East Asia to play a significant role in capturing Investment, NRI remittance, and trade flows between SEA and India.