Consider the sheer volume of information flowing through today’s financial systems: every QR payment, e-KYC onboarding, credit card swipe, and cross-border transfer captures a data point. With digital banking and Open Banking, financial institutions are sitting on a goldmine of insights. But this isn’t just about data collection; it’s about converting that data into strategic advantage in a fast-moving, customer-driven landscape.

With digital banks gaining traction and regulators around the world pushing bold reforms, the industry is entering a new phase of financial innovation powered by data and accelerated by AI.

Ecosystm gathered insights and identified key challenges from senior banking leaders during a series of roundtables we moderated across Asia Pacific. The conversations revealed a clear picture of where momentum is building – and where obstacles continue to slow progress. From these discussions, several key themes emerged that highlight both opportunities and ongoing barriers in the Banking sector.

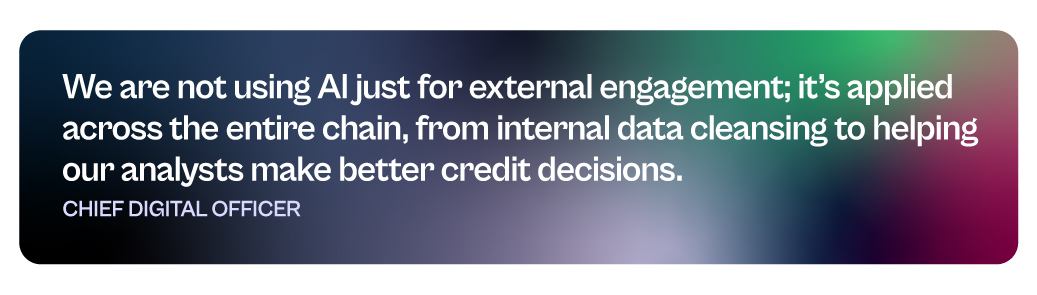

1. AI is Leading to End-to-End Transformation

Banks are moving beyond generic digital offerings to deliver hyper-personalised, data-driven experiences that build loyalty and drive engagement. AI is driving this shift by helping institutions anticipate customer needs through real-time analysis of behavioural, transactional, and demographic data. From pre-approved credit offers and contextual investment nudges to app interfaces that adapt to individual financial habits, personalisation is becoming a core strategy, not just a feature. This is a huge departure from reactive service models, positioning data as a long-term strategic asset.

But the impact of AI isn’t limited to customer-facing experiences. It’s also driving innovation deep within the banking stack, from fraud detection and SME loan processing to intelligent chatbots that scale customer support. On the infrastructure side, banks are investing in agile, AI-ready platforms to support automation, model training, and advanced analytics at scale. These shifts are redefining how banks operate, make decisions, and deliver value. Institutions that integrate AI across both front-end journeys and back-end processes are setting a new benchmark for agility, efficiency, and competitiveness in a fast-changing financial landscape.

2. Regulatory Shifts are Redrawing the Competitive Landscape

Regulators are moving quickly in Asia Pacific by introducing frameworks for Open Banking, real-time payments, and even AI-specific standards like Singapore’s AI Verify. But the challenge for banks isn’t just keeping up with evolving external mandates. Internally, many are navigating a complicated mix of overlapping policies, built up over years of compliance with local, regional, and global rules. This often slows down innovation and makes it harder to implement AI and automation consistently across the organisation.

As banks double down on AI, it is clear that governance can’t be an afterthought. Many are still dealing with fragmented ownership of AI systems, inconsistent oversight, and unclear rules around things like model fairness and explainability. The more progressive ones are starting to fix this by setting up centralised governance frameworks, investing in risk-based controls, and putting processes in place to monitor things like bias and model drift from day one. They are not just trying to stay compliant; they are preparing for what’s coming next. In this landscape, the ability to manage regulatory complexity with speed and clarity, both internally and externally, is quickly becoming a competitive edge.

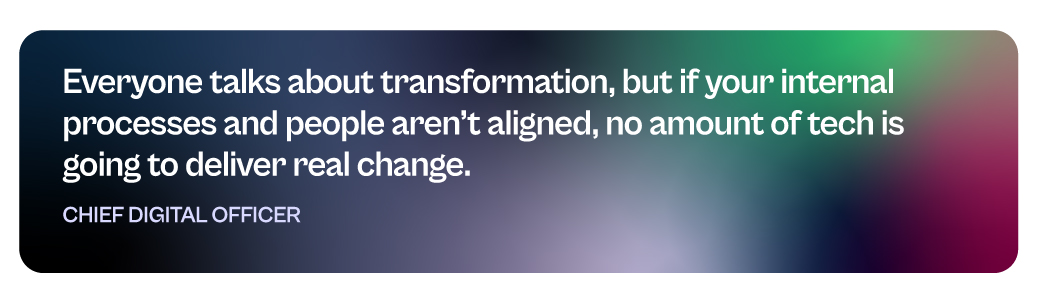

3. Success Depends on Strategy, Not Just Tech

While enthusiasm for AI is high, sustainable success hinges on a clear, aligned strategy that connects technology to business outcomes. Many banks struggle with fragmented initiatives because they lack a unified roadmap that prioritises high-impact use cases. Without clear goals, AI projects often fail to deliver meaningful value, becoming isolated pilots with limited scalability.

To avoid this, banks need to develop robust return-on-investment (ROI) models tailored to their context — measuring benefits like faster credit decisioning, reduced fraud losses, or increased cross-selling effectiveness. These models must consider not only the upfront costs of infrastructure and talent, but also ongoing expenses such as model retraining, governance, and integration with existing systems.

Ethical AI governance is another essential pillar. With growing regulatory scrutiny and public concern about opaque “black box” models, banks must embed transparency, fairness, and accountability into their AI frameworks from the outset. This goes beyond compliance; strong governance builds trust and is key to responsible, long-term use of AI in sensitive, high-stakes financial environments.

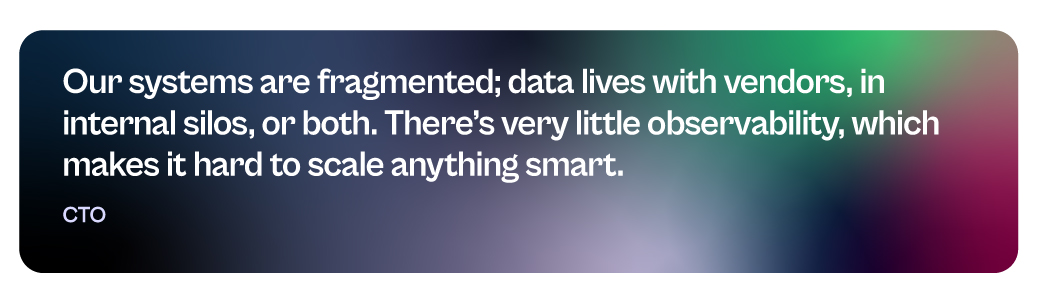

4. Legacy Challenges Still Hold Banks Back

Despite strong momentum, many banks face foundational barriers that hinder effective AI deployment. Chief among these is data fragmentation. Core customer, transaction, compliance, and risk data are often scattered across legacy systems and third-party platforms, making it difficult to access the integrated, high-quality data that AI models require.

This limits the development of comprehensive solutions and makes AI implementations slower, costlier, and less effective. Instead of waiting for full system replacements, banks need to invest in integration layers and modern data platforms that unify data sources and make them AI-ready. These platforms can connect siloed systems – such as CRM, payments, and core banking – to deliver a consolidated view, which is crucial for accurate credit scoring, personalised offers, and effective risk management.

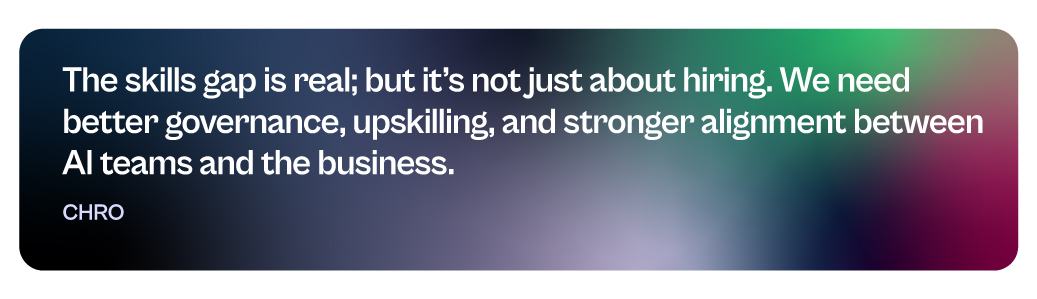

Banks must also address talent gaps. The shortage of in-house AI expertise means many institutions rely on external consultants, which increases costs and reduces knowledge transfer. Without building internal capabilities and adjusting existing processes to accommodate AI, even sophisticated models may end up underused or misapplied.

5. Collaboration and Capability Building are Key Enablers

AI transformation isn’t just a technology project – it’s an organisation-wide shift that requires new capabilities, ways of working, and strategic partnerships. Success depends on more than just hiring data scientists. Relationship managers, credit officers, compliance teams, and frontline staff all need to be trained to understand and act on AI-driven insights. Processes such as loan approvals, fraud escalations, and customer engagement must be redesigned to integrate AI outputs seamlessly.

To drive continuous innovation, banks should establish internal Centres of Excellence for AI. These hubs can lead experimentation with high-value use cases like predictive credit scoring or real-time fraud detection, while ensuring that learnings are shared across business units. They also help avoid duplication and promote strategic alignment.

Partnerships with fintechs, technology providers, and academic institutions play a vital role as well. These collaborations offer access to cutting-edge tools, niche expertise, and locally relevant AI models that reflect the regulatory, cultural, and linguistic contexts banks operate in. In a fast-moving and increasingly competitive space, this combination of internal capability building and external collaboration gives banks the agility and foresight to lead.

The energy at ServiceNow’s Knowledge25 matched the company’s ambitious direction! ServiceNow is repositioning itself as more than just an IT service platform – aiming to be the orchestration layer for the modern enterprise. Over the past two days, I’ve seen a clear focus on platform extensibility, AI-driven automation, and a push into new functional territories like CRM and ERP.

Here are my key takeaways from Knowledge25.

Click here to download “ServiceNow Knowledge25: Big Moves, Bold Bets, and What’s Next” as a PDF.

AI Everywhere: Agents and Control Towers

ServiceNow goes all in on AI Agents – and makes it easy to adopt.

Like Google, Salesforce, and AWS, ServiceNow is betting big on agents. But with a key advantage: it’s already the enterprise layer where workflows live. Its AI Agents don’t just automate tasks; they amplify what’s already working, layer in intelligence, and collaborate with other agents across systems. ServiceNow becomes the orchestration hub, just as it already is for processes and change.

ServiceNow’s AI Control Tower is a critical accelerator for AI at scale. It enforces policies, ensures compliance with internal and regulatory standards, and provides the guardrails needed to deploy AI responsibly and confidently.

The bigger move? Removing friction. Most employees don’t know what agents can do – so they don’t ask. ServiceNow solves this with hundreds of prebuilt agents across finance, risk, IT, service, CRM, and more. No guesswork. Just plug and go.

Sitting Above Silos: ServiceNow’s Architectural Advantage

ServiceNow is finally highlighting its architectural edge.

It’s one of the few platforms that can sit above all systems of record – pulling in data as needed, delivering workflows to employees and customers, and pushing updates back into core systems. While most Asia Pacific customers use ServiceNow mainly for IT help desk and service requests, its potential extends much further. Virtually anything done in ERP, CRM, SCM, or HRM systems can be delivered through ServiceNow, often with far greater agility. Workflow changes that once took weeks or months can now happen instantly.

ServiceNow is leaning into this capability more forcefully than ever, positioning itself as the platform that can finally keep pace with constant business change.

Stepping into the Ring: ServiceNow’s CRM & ERP Ambitions

ServiceNow is expanding into CRM and ERP workflows – putting itself in competition with some of the industry’s biggest players.

ServiceNow is boldly targeting CRM as a growth area, despite Salesforce’s dominance, by addressing gaps traditional CRMs miss. Customer workflows extend far beyond sales and service, spanning fulfillment, delivery, supply chain, and compliance. A simple quoting process, for instance, often pulls data from multiple systems. ServiceNow covers the full scope, positioning itself as the platform that orchestrates end-to-end customer workflows from a fundamentally different angle.

Its Core Business Suite – an AI-powered solution that transforms core processes like HR, procurement, finance, and legal – also challenges traditional ERP providers, With AI-driven automation for tasks like case management, it simplifies workflows and streamlines operations across departments.

Closing the Skills Gap: ServiceNow University

To support its vision, ServiceNow is investing heavily in education.

The refreshed ServiceNow University aims to certify 3 million professionals by 2030. This is critical to build both demand (business leaders who ask for ServiceNow) and supply (professionals who can implement and extend the platform).

But the skills shortage is a now problem, not a 2030 problem. ServiceNow must go beyond online learning and push harder on in-person classes, tutorials, and train-the-trainer programs across Asia Pacific. Major cloud providers like AWS broke through when large enterprises started training their entire workforces – not just on usage, but on development. ServiceNow needs similar scale and commitment to hit the mainstream.

Asia Pacific: ServiceNow’s Next Growth Frontier

ServiceNow’s potential is massive – and its opportunities even bigger.

In Asia Pacific, many implementations are partner-led, but most partners are currently focused on the platform’s legacy IT capabilities. To unlock growth, ServiceNow needs to empower its partners to engage beyond IT and connect with business leaders.

Despite broader challenges like shrinking tech budgets, fragmented decision-making, and decentralised tech ownership, ServiceNow has a clear path forward. By upskilling partners, simplifying its narrative, and adapting quickly, it’s well-positioned to continue its growth and surpass the hurdles many other software vendors face.

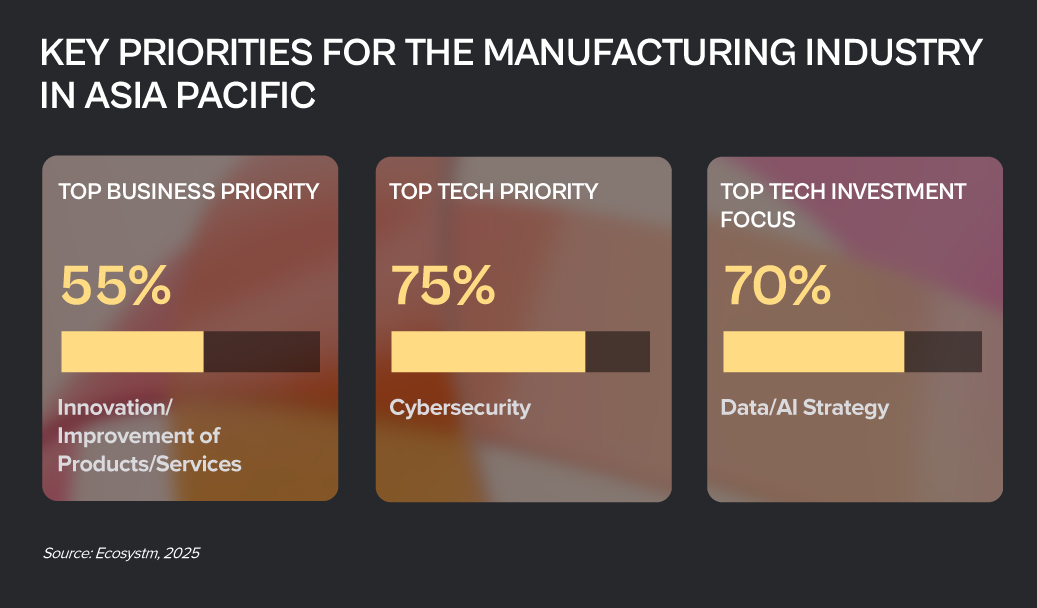

The Manufacturing sector, traditionally defined by stable processes and infrastructure, is now facing a pivotal shift. Rapid technological advancements and shifting global market dynamics have rendered incremental improvements inadequate for long-term competitiveness and growth. To thrive, manufacturers must fundamentally reimagine their entire value chain.

By embracing intelligent systems, enhancing agility, and proactively shaping future-ready operations, organisations can navigate today’s industrial complexities and position themselves for sustained success.

Here are recent examples of Manufacturing transformation in the Asia Pacific.

Click here to download “Future Forward: Reimagining Manufacturing” as a PDF.

Intelligent Automation & Efficiency

Komatsu Australia, a global industrial equipment manufacturer, tackled growing inefficiencies in its small parts department, where teams manually processed hundreds of PDF invoices daily from more than 250 suppliers.

To streamline this, the company deployed intelligent automation – AI now extracts and validates data from invoices against purchase orders and inputs it directly into the legacy mainframe.

The impact has been sharp: over 300 hours saved annually for one supplier, 1,100 invoices processed in three weeks, and a dramatic drop in manual errors. Employees have shifted to higher-value tasks, and a citizen developer program is enabling staff to build custom automation tools. With a scalable framework in place, Komatsu has not only transformed invoice processing but also set the stage for broader automation across the enterprise.

Data-Driven Insights & Agility

Berger Paints India Ltd., a leader in paints and coatings, needed to scale fast amid rising database loads and complex on-prem systems.

In response, Berger Paints migrated its mission-critical databases and core business applications – covering finance, manufacturing, sales, and asset management – to a high-performance cloud platform.

This shift boosted operational efficiency by 25%, doubled reporting and system response times, and enhanced scalability and disaster recovery with geographically distributed cloud regions. The move simplified access to data, driving faster, insight-driven decision-making. With streamlined infrastructure management and optimised costs, Berger Paints is now poised to leverage advanced technologies like AI/ML, setting the stage for continued innovation and growth.

Connected Operations & Customer Centricity

JSW Steel, one of India’s leading steel producers, set out to shift from a plant-centric model to a customer-first approach. The challenge: integrating complex systems like ERP, CRM, and manufacturing to streamline operations and improve order fulfillment.

With a robust integration platform, JSW Steel connected over 32 systems using 120+ APIs – automating processes and enabling real-time data flow across orders, inventory, pricing, and production.

The results speak for themselves: faster order fulfillment, reduced cost-to-serve, and real-time visibility that optimises scheduling. Scalable, composable APIs now support growth, while a 99.7% success rate across 7.2 million API calls ensures reliability. JSW Steel has transformed how it operates – running faster, serving smarter, and delivering better customer experiences across the entire order-to-cash journey.

Modernising Core Systems & Foundational Transformation

Fujitsu General, a global leader in air conditioning systems, was constrained by a 30-year-old COBOL-based mainframe and fragmented processes. The legacy system posed a Y2K-like risk and limited operational agility.

The company implemented a modern, unified ERP platform to eliminate risk, streamline operations, and boost agility.

By integrating functions across sales, production, procurement, accounting, and HR and addressing unique business needs with low-code development, the company created a clean, adaptable core system. Robust integration connected disparate data sources, while a central repository eliminated silos. The transformation delivered seamless end-to-end operations, standardised workflows, improved agility, and real-time insights – setting Fujitsu General up for continued innovation and long-term resilience.

Powering Growth with a Modern Network

As a critical supplier to India’s infrastructure boom, Hindalco needed to modernise its network across 55 sites – improving app performance, enabling real-time insights, and building a future-ready, sustainable foundation.

Hindalco replaced its ageing hub-and-spoke model with a modern mesh architecture using SD-WAN.

The new architecture prioritised key app traffic, simplified cloud access, and enabled segmentation. Centralised orchestration and SSE integration brought automation and robust security. The impact: 30% lower costs, 50% faster apps, real-time visibility, rapid deployment, and smarter bandwidth. Hindalco now runs on a lean, secure digital backbone – built for agility, performance, and scale.

For marketers, the “golden goal” has always been to deeply understand customers, enabling more effective cross-selling, upselling, and targeted campaigns. The promise of maximising wallet share hinges on this fundamental principle. Imagine having technologies that can analyse customer journeys deeply, uncovering meaningful, real-time insights into customer behaviour and sentiment. This rich, dynamic data could empower marketing teams to move beyond static profiles, gaining immediate visibility into how customers react to campaigns, messages, and interactions across all channels.

Data Fragmentation: The CMO’s Blind Spot

However, achieving this goal has become increasingly difficult. The modern marketing stack, built upon CRM, content marketing platforms, retargeting ad solutions, social listening tools, and countless other applications, often operates in silos. This wide, disconnected array of tools creates a significant challenge: making sense of the fragmented data. Efforts to truly understand customers and identify valuable prospects frequently fall short of desired outcomes. The lack of integration and the sheer volume of disparate data leave marketers struggling to connect the dots and extract actionable insights.

Unified Customer Vision: AI Agents for Intelligent Marketing

The solution lies in leveraging AI agents that operate seamlessly in the background. By implementing AI agents, CMOs can gain a comprehensive understanding of their customers, enabling them to run more effective campaigns, drive greater wallet share, and build stronger, more meaningful customer relationships.

These intelligent agents can bridge the gaps in customer data, sentiment, and campaign perception by accessing and processing information across the entire marketing stack. By learning from metadata, successful and failed campaigns, and a broad range of customer insights – including conversational and digital contact centre data – these agents can provide a unified view of the customer.

What They Bring to the Table

- Unified Data Access. AI agents can traverse siloed marketing applications, extracting and correlating data from various sources.

- Real-Time Insight Generation. They can analyse customer interactions, including social media sentiment, conversational AI data, and voice bot interactions, to provide dynamic, real-time insights.

- Autonomous Action & Adaptation. Agentic workflows can adapt to campaigns, email blasts, and lead generation activities autonomously, refining strategies and messaging on the fly.

- Content Curation & Optimisation. Content curation agents can tailor content based on real-time customer feedback and preferences.

- Proactive Opportunity Identification. By identifying gaps in customer understanding and campaign performance, AI agents can empower marketers to uncover new opportunities for engagement and growth.

Extending AI Agent Value: Practical Applications for the Modern CMO

Beyond unified data access and autonomous action, AI agents offer a wealth of practical applications that can revolutionise marketing operations. Consider the following scenarios:

- Automating Time-Consuming Tasks. Identify and offload repetitive, manual tasks associated with campaign execution and lead generation to a team of AI agents, freeing up valuable human resources for strategic initiatives.

- Enhancing Sales Pipeline Intelligence. Leverage AI agents to extract insights from sales pipelines and customer feedback, enabling data-driven campaign adjustments and improved sales alignment.

- Real-Time Sentiment Analysis. Deploy multiple AI agents to monitor customer sentiment across conversations and social media platforms, providing immediate feedback on campaign effectiveness and brand perception.

- Strategic Scenario Planning. Use AI agents to formulate and evaluate various marketing spend scenarios across different channels and agencies, optimising resource allocation and maximising ROI.

- Dynamic Campaign Monitoring. Implement AI agents to track campaign performance in real-time, allowing for immediate adjustments and optimisation.

- Event Sentiment Analysis. Employ AI to monitor customer sentiment during live events, providing immediate insights into audience reactions and engagement.

- Unlocking Conversational Intelligence. Extract valuable insights from sales conversations and contact centre interactions, feeding them into future sales strategies and upselling opportunities. This extends beyond relying solely on CRM data, providing a richer, more nuanced understanding of customer interactions.

By implementing these capabilities, CMOs can transform their marketing operations, moving from reactive to proactive, and ultimately driving greater customer engagement and business success.

The “Wow” Factor: Agentic AI and Unified Data

Ultimately, the pursuit of a seamless customer journey and deeper conversational engagement hinges on bridging the persistent departmental disconnect. Despite each team interacting with the same customer, data remains siloed, hindering a holistic understanding and unified approach.

The missing link lies in fostering a dynamic, interconnected data ecosystem where insights from campaigns, social listening, contact centre conversations, chatbot interactions, VoC programs, marketing applications, and CRM flow freely and mutually reinforce each other.

This is where Agentic AI steps in. By empowering AI agents to adapt and act autonomously across these diverse data sources, we create a symphony of customer intelligence. These agents, working in harmony, unlock the potential for real-time, actionable insights, enabling marketers to craft truly exceptional, “wow” moments that resonate deeply with customers. In essence, Agentic AI transforms fragmented data into a unified, powerful force, driving unparalleled customer experiences and forging lasting brand loyalty.

A lot has been written and spoken about DeepSeek since the release of their R1 model in January. Soon after, Alibaba, Mistral AI, and Ai2 released their own updated models, and we have seen Manus AI being touted as the next big thing to follow.

DeepSeek’s lower-cost approach to creating its model – using reinforcement learning, the mixture-of-experts architecture, multi-token prediction, group relative policy optimisation, and other innovations – has driven down the cost of LLM development. These methods are likely to be adopted by other models and are already being used today.

While the cost of AI is a challenge, it’s not the biggest for most organisations. In fact, few GenAI initiatives fail solely due to cost.

The reality is that many hurdles still stand in the way of organisations’ GenAI initiatives, which need to be addressed before even considering the business case – and the cost – of the GenAI model.

Real Barriers to GenAI

• Data. The lifeblood of any AI model is the data it’s fed. Clean, well-managed data yields great results, while dirty, incomplete data leads to poor outcomes. Even with RAG, the quality of input data dictates the quality of results. Many organisations I work with are still discovering what data they have – let alone cleaning and classifying it. Only a handful in Australia can confidently say their data is fully managed, governed, and AI-ready. This doesn’t mean GenAI initiatives must wait for perfect data, but it does explain why Agentic AI is set to boom – focusing on single applications and defined datasets.

• Infrastructure. Not every business can or will move data to the public cloud – many still require on-premises infrastructure optimised for AI. Some companies are building their own environments, but this often adds significant complexity. To address this, system manufacturers are offering easy-to-manage, pre-built private cloud AI solutions that reduce the effort of in-house AI infrastructure development. However, adoption will take time, and some solutions will need to be scaled down in cost and capacity to be viable for smaller enterprises in Asia Pacific.

• Process Change. AI algorithms are designed to improve business outcomes – whether by increasing profitability, reducing customer churn, streamlining processes, cutting costs, or enhancing insights. However, once an algorithm is implemented, changes will be required. These can range from minor contact centre adjustments to major warehouse overhauls. Change is challenging – especially when pre-coded ERP or CRM processes need modification, which can take years. Companies like ServiceNow and SS&C Blue Prism are simplifying AI-driven process changes, but these updates still require documentation and training.

• AI Skills. While IT teams are actively upskilling in data, analytics, development, security, and governance, AI opportunities are often identified by business units outside of IT. Organisations must improve their “AI Quotient” – a core understanding of AI’s benefits, opportunities, and best applications. Broad upskilling across leadership and the wider business will accelerate AI adoption and increase the success rate of AI pilots, ensuring the right people guide investments from the start.

• AI Governance. Trust is the key to long-term AI adoption and success. Being able to use AI to do the “right things” for customers, employees, and the organisation will ultimately drive the success of GenAI initiatives. Many AI pilots fail due to user distrust – whether in the quality of the initial data or in AI-driven outcomes they perceive as unethical for certain stakeholders. For example, an AI model that pushes customers toward higher-priced products or services, regardless of their actual needs, may yield short-term financial gains but will ultimately lose to ethical competitors who prioritise customer trust and satisfaction. Some AI providers, like IBM and Microsoft, are prioritising AI ethics by offering tools and platforms that embed ethical principles into AI operations, ensuring long-term success for customers who adopt responsible AI practices.

GenAI and Agentic AI initiatives are far from becoming standard business practice. Given the current economic and political uncertainty, many organisations will limit unbudgeted spending until markets stabilise. However, technology and business leaders should proactively address the key barriers slowing AI adoption within their organisations. As more AI platforms adopt the innovations that helped DeepSeek reduce model development costs, the economic hurdles to GenAI will become easier to overcome.

In my last Ecosystm Insights, I spoke about why organisations need to think about the Voice of the Customer (VoC) quite literally. Organisations need to listen to what their customers are telling them – not just to the survey questions they responded to, answering pre-defined questions that the organisations want to hear about.

The concept of customer feedback is evolving, and how organisations design and manage VoC programs must also change. Technology is now capable of enabling customer teams to tap into all those unsolicited, and often unstructured, raw feedback sources. Think contact centre conversations (calls, chats, chatbots, emails, complaints, call notes), CRM notes, online reviews, social media, etc. Those are all sources of raw customer feedback, waiting to be converted into customer insights.

Organisations can now find the capability of extracting customer insight from raw data across a wide range of solutions, from VoC platforms, data management platforms, contact centre solutions, text analytics players, etc. The expanding tech ecosystem presents opportunities for organisations to enhance their programs. However, navigating this breadth of options can also be confusing as they strive to identify the most suitable tools for their requirements.

As CX programs mature and shift from survey feedback to truly listening to customers, the demand for tech solutions tailored to various needs increases.

Where are tech vendors headed?

As part of my job as CX Consultant & Tech Advisor, I spend a lot of time working with my clients. But I also spend a lot of time speaking with technology vendors, who provide the solutions my clients need. Over the last few weeks and months there’s been a flurry of activity across the CX technology market with lots of product announcements around one specific topic. You guessed it, GenAI.

So, I invested some time in finding out how tech vendors are evolving their offerings. From Medallia, InMoment, Thematic, LiquidVoice, Concentrix, Snowflake, Nice, to Tethr – a broad variety of different vendors, but all with one thing in common; they help analyse customer feedback data.

And I like what I hear. The conversation has not been about GenAI because of GenAI, but about use cases and real-life applications for CX practitioners, including Insights & Research team, Contact Centre, CX, VoC, Digital teams, and so on. The list is long when we include everyone who has a role to play in creating, maintaining, and improving customer experiences.

It’s no wonder that many different vendors have started to embed those capabilities into their solutions and launch new products or features. The tech landscape is becoming increasingly fragmented at this stage.

What are an organisation’s tech options?

- The traditional VoC platform providers typically offer some text analytics capabilities (although not always included in the base price) and have started to tap into the contact centre solutions as well. Some also offer some social media or online review analysis, leaving organisations with a relatively good understanding of customer sentiment and a better understanding of their CX.

- Contact centre solutions are traditionally focused on analysing calls for Quality Assurance (QA) purposes and use surveys for agent coaching. Many contact centre players have evolved their portfolios to include text analytics or conversational intelligence to extract broader customer insights. Although at this stage they’re not always shared with the rest of the organisation (one step at a time…).

- Conversational analytics/intelligence providers have emerged over the last few years and are a powerhouse for contact centre and chatbot conversations. The contact centre really is the treasure trove of customer insights, although vastly underutilised for it so far!

- CRMs are the backbone of the customer experience management toolkit as they hold a vast amount of metadata. They’ve also been able to send surveys for a while now. Analysing unstructured data however (whether survey verbatim or otherwise) isn’t one of their strengths. This leaves organisations with a lot of data but not necessarily insights.

- Social media listening tools are often standalone tools used by the social media teams. There are not many instances of them being used for the analysis of other unstructured feedback.

- Digital/website feedback tools, in line with some of the above, are centred around collecting feedback, not necessarily analysing the unstructured feedback.

- Pure text analytics players are traditionally focused on analysing surveys verbatim. As this is their core offering, they tend to be proficient in it and have started to broaden their portfolios to include other unstructured feedback sources.

- Customer Data Platforms (CDP)/ Data Management Platforms (DMP) are more focused on quantitative data about customers and their experiences. Although many speak about their ability to analyse unstructured feedback as well, it doesn’t appear to be their strengths.

Conclusion

But what does that leave organisations with? Apart from very confused tech users trying to find the right solution for their organisation.

At this stage, there is immense market fragmentation, with many vendors from different core capabilities starting to incorporate capabilities to analyse unstructured data in the wake of the GenAI boom. However, a market convergence is expected.

While we watch how the market unfolds, one thing is certain. Organisations and customer teams will need to adjust – and that includes the tech stack as well as the CX program set up. With customer feedback now coming from anywhere within or outside the organisation, there is a need for a consolidated source of truth to make sense of it all and move from raw data to customer insights. While organisations will benefit immensely from a consolidated customer data repository, it’s also crucial to break down organisational silos at the same time and democratise insights as widely as possible to enable informed decision-making.

Customer feedback is at the heart of Customer Experience (CX). But it’s changing. What we consider customer feedback, how we collect and analyse it, and how we act on it is changing. Today, an estimated 80-90% of customer data is unstructured. Are you able and ready to leverage insights from that vast amount of customer feedback data?

Let’s begin with the basics: What is VoC and why is there so much buzz around it now?

Voice of the Customer (VoC) traditionally refers to customer feedback programs. In its most basic form that means organisations are sending surveys to customers to ask for feedback. And for a long time that really was the only way for organisations to understand what their customers thought about their brand, products, and services.

But that was way back then. Over the last few years, we’ve seen the market (organisations and vendors) dipping their toes into the world of unsolicited feedback.

What’s unsolicited feedback, you ask?

Unsolicited feedback simply means organisations didn’t actually ask for it and they’re often not in control over it, but the customer provides feedback in some way, shape, or form. That’s quite a change to the traditional survey approach, where they got answers to questions they specifically asked (solicited feedback).

Unsolicited feedback is important for many reasons:

- Organisations can tap into a much wider range of feedback sources, from surveys to contact centre phone calls, chats, emails, complaints, social media conversations, online reviews, CRM notes – the list is long.

- Surveys have many advantages, but also many disadvantages. From only hearing from a very specific customer type (those who respond and are typically at the extreme ends of the feedback sentiment), getting feedback on the questions they ask, and hearing from a very small portion of the customer base (think email open rates and survey fatigue).

- With unsolicited feedback organisations hear from 100% of the customers who interact with the brand. They hear what customers have to say, and not just how they answer predefined questions.

It is a huge step up, especially from the traditional post-call survey. Imagine a customer just spent 30 min on the line with an agent explaining their problem and frustration, just to receive a survey post call, to tell the organisation what they just told the agent, and how they felt about the experience. Organisations should already know that. In fact, they probably do – they just haven’t started tapping into that data yet. At least not for CX and customer insights purposes.

When does GenAI feature?

We can now tap into those raw feedback sources and analyse the unstructured data in a way never seen before. Long gone are the days of manual excel survey verbatim read-throughs or coding (although I’m well aware that that’s still happening!). Tech, in particular GenAI and Large Language Models (LLMs), are now assisting organisations in decluttering all the messy conversations and unstructured data. Not only is the quality of the analysis greatly enhanced, but the insights are also presented in user-friendly formats. Customer teams ask for the insights they need, and the tools spit it out in text form, graphs, tables, and so on.

The time from raw data to insights has reduced drastically, from hours and days down to seconds. Not only has the speed, quality, and ease of analysis improved, but many vendors are now integrating recommendations into their offerings. The tools can provide “basic” recommendations to help customer teams to act on the feedback, based on the insights uncovered.

Think of all the productivity gains and spare time organisations now have to act on the insights and drive positive CX improvements.

What does that mean for CX Teams and Organisations?

Including unsolicited feedback into the analysis to gain customer insights also changes how organisations set up and run CX and insights programs.

It’s important to understand that feedback doesn’t belong to a single person or team. CX is a team sport and particularly when it comes to acting on insights. It’s essential to share these insights with the right people, at the right time.

Some common misperceptions:

- Surveys have “owners” and only the owners can see that feedback.

- Feedback that comes through a specific channel, is specific to that channel or product.

- Contact centre feedback is only collected to coach staff.

If that’s how organisations have built their programs, they’ll have to rethink what they’re doing.

If organisations think about some of the more commonly used unstructured feedback, such as that from the contact centre or social media, it’s important to note that this feedback isn’t solely about the contact centre or social media teams. It’s about something else. In fact, it’s usually about something that created friction in the customer experience, that was generated by another team in the organisation. For example: An incorrect bill can lead to a grumpy social media post or a faulty product can lead to a disgruntled call to the contact centre. If the feedback is only shared with the social media or contact centre team, how will the underlying issues be resolved? The frontline teams service customers, but organisations also need to fix the underlying root causes that created the friction in the first place.

And that’s why organisations need to start consolidating the feedback data and democratise it.

It’s time to break down data and organisational silos and truly start thinking about the customer. No more silos. Instead, organisations must focus on a centralised customer data repository and data democratisation to share insights with the right people at the right time.

In my next Ecosystm Insights, I will discuss some of the tech options that CX teams have. Stay tuned!

Banks, insurers, and other financial services organisations in Asia Pacific have plenty of tech challenges and opportunities including cybersecurity and data privacy management; adapting to tech and customer demands, AI and ML integration; use of big data for personalisation; and regulatory compliance across business functions and transformation journeys.

Modernisation Projects are Back on the Table

An emerging tech challenge lies in modernising, replacing, or retiring legacy platforms and systems. Many banks still rely on outdated core systems, hindering agility, innovation, and personalised customer experiences. Migrating to modern, cloud-based systems presents challenges due to complexity, cost, and potential disruptions. Insurers are evaluating key platforms amid evolving customer needs and business models; ERP and HCM systems are up for renewal; data warehouses are transforming for the AI era; even CRM and other CX platforms are being modernised as older customer data stores and models become obsolete.

For the past five years, many financial services organisations in the region have sidelined large legacy modernisation projects, opting instead to make incremental transformations around their core systems. However, it is becoming critical for them to take action to secure their long-term survival and success.

Benefits of legacy modernisation include:

- Improved operational efficiency and agility

- Enhanced customer experience and satisfaction

- Increased innovation and competitive advantage

- Reduced security risks and compliance costs

- Preparation for future technologies

However, legacy modernisation and migration initiatives carry significant risks. For instance, TSB faced a USD 62M fine due to a failed mainframe migration, resulting in severe disruptions to branch operations and core banking functions like telephone, online, and mobile banking. The migration failure led to 225,492 complaints between 2018 and 2019, affecting all 550 branches and required TSB to pay more than USD 25M to customers through a redress program.

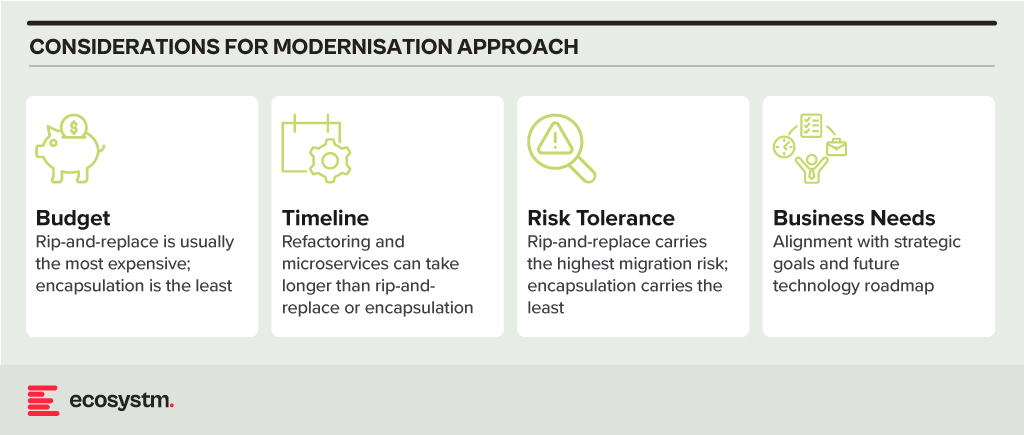

Modernisation Options

- Rip and Replace. Replacing the entire legacy system with a modern, cloud-based solution. While offering a clean slate and faster time to value, it’s expensive, disruptive, and carries migration risks.

- Refactoring. Rewriting key components of the legacy system with modern languages and architectures. It’s less disruptive than rip-and-replace but requires skilled developers and can still be time-consuming.

- Encapsulation. Wrapping the legacy system with a modern API layer, allowing integration with newer applications and tools. It’s quicker and cheaper than other options but doesn’t fully address underlying limitations.

- Microservices-based Modernisation. Breaking down the legacy system into smaller, independent services that can be individually modernised over time. It offers flexibility and agility but requires careful planning and execution.

Financial Systems on the Block for Legacy Modernisation

Data Analytics Platforms. Harnessing customer data for insights and targeted offerings is vital. Legacy data warehouses often struggle with real-time data processing and advanced analytics.

CRM Systems. Effective customer interactions require integrated CRM platforms. Outdated systems might hinder communication, personalisation, and cross-selling opportunities.

Payment Processing Systems. Legacy systems might lack support for real-time secure transactions, mobile payments, and cross-border transactions.

Core Banking Systems (CBS). The central nervous system of any bank, handling account management, transactions, and loan processing. Many Asia Pacific banks rely on aging, monolithic CBS with limited digital capabilities.

Digital Banking Platforms. While several Asia Pacific banks provide basic online banking, genuine digital transformation requires mobile-first apps with features such as instant payments, personalised financial management tools, and seamless third-party service integration.

Modernising Technical Approaches and Architectures

Numerous technical factors need to be addressed during modernisation, with decisions needing to be made upfront. Questions around data migration, testing and QA, change management, data security and development methodology (agile, waterfall or hybrid) need consideration.

Best practices in legacy migration have taught some lessons.

Adopt a data fabric platform. Many organisations find that centralising all data into a single warehouse or platform rarely justifies the time and effort invested. Businesses continually generate new data, adding sources, and updating systems. Managing data where it resides might seem complex initially. However, in the mid to longer term, this approach offers clearer benefits as it reduces the likelihood of data discrepancies, obsolescence, and governance challenges.

Focus modernisation on the customer metrics and journeys that matter. Legacy modernisation need not be an all-or-nothing initiative. While systems like mainframes may require complete replacement, even some mainframe-based software can be partially modernised to enable services for external applications and processes. Assess the potential of modernising components of existing systems rather than opting for a complete overhaul of legacy applications.

Embrace the cloud and SaaS. With the growing network of hyperscaler cloud locations and data centres, there’s likely to be a solution that enables organisations to operate in the cloud while meeting data residency requirements. Even if not available now, it could align with the timeline of a multi-year legacy modernisation project. Whenever feasible, prioritise SaaS over cloud-hosted applications to streamline management, reduce overhead, and mitigate risk.

Build for customisation for local and regional needs. Many legacy applications are highly customised, leading to inflexibility, high management costs, and complexity in integration. Today, software providers advocate minimising configuration and customisation, opting for “out-of-the-box” solutions with room for localisation. The operations in different countries may require reconfiguration due to varying regulations and competitive pressures. Architecting applications to isolate these configurations simplifies system management, facilitating continuous improvement as new services are introduced by platform providers or ISV partners.

Explore the opportunity for emerging technologies. Emerging technologies, notably AI, can significantly enhance the speed and value of new systems. In the near future, AI will automate much of the work in data migration and systems integration, reducing the need for human involvement. When humans are required, low-code or no-code tools can expedite development. Private 5G services may eliminate the need for new network builds in branches or offices. AIOps and Observability can improve system uptime at lower costs. Considering these capabilities in platform decisions and understanding the ecosystem of partners and providers can accelerate modernisation journeys and deliver value faster.

Don’t Let Analysis Paralysis Slow Down Your Journey!

Yes, there are a lot of decisions that need to be made; and yes, there is much at stake if things go wrong! However, there’s a greater risk in not taking action. Maintaining a laser-focus on the customer and business outcomes that need to be achieved will help align many decisions. Keeping the customer experience as the guiding light ensures organisations are always moving in the right direction.

Organisations are moving beyond digitalisation to a focus on building market differentiation. It is widely acknowledged that customer-centric strategies lead to better business outcomes, including increased customer satisfaction, loyalty, competitiveness, growth, and profitability.

AI is the key enabler driving personalisation at scale. It has also become key to improving employee productivity, empowering them to focus on high-value tasks and deepening customer engagements.

Over the last month – at the Salesforce World Tour and over multiple analyst briefings – Salesforce has showcased their desire to solve customer challenges using AI innovations. They have announced a range of new AI innovations across Data Cloud, their integrated CRM platform.

Ecosystm Advisors Kaushik Ghatak, Niloy Mukherjee, Peter Carr, and Sash Mukherjee comment on Salesforce’s recent announcements and messaging.

Read on to find out more.

Download Ecosystm VendorSphere: Salesforce AI Innovations Transforming CRM as a PDF