Australia is making meaningful progress on its digital journey, driven by a vibrant tech sector, widespread technology adoption, and rising momentum in AI. But realising its full potential as a leading digital economy will depend on bridging the skills gap, moving beyond surface-level AI applications, accelerating SME digital transformation, and navigating ongoing economic uncertainty. For many enterprises, the focus is shifting from experimentation to execution, using technology to drive efficiency, resilience, and measurable outcomes.

Increasingly, leaders are asking not just how fast Australia can innovate, but how wisely. Strategic choices made now will shape a digital future grounded in national values where technology fuels both economic growth and public good.

These five key realities capture the current state of Australia’s technology landscape, based on insights from Ecosystm’s industry conversations and research.

1. Responsible by Design: Australia’s Path to Trusted AI

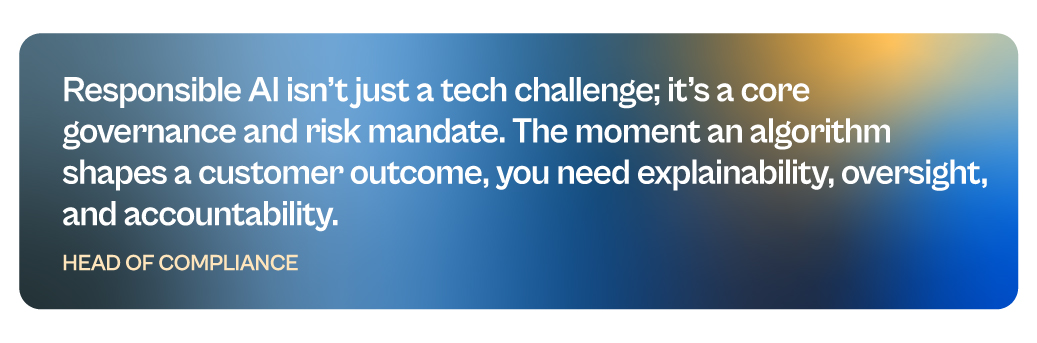

AI in Australia is progressing with a strong focus on ethics and public trust. Regulators like ASIC and the OAIC (Office of the Australian Information Commissioner) have made it clear that AI systems, especially in banking, insurance, and healthcare, must be transparent and fair. Banks like ANZ and Commonwealth Bank, have developed responsible AI frameworks to ensure their algorithms don’t unintentionally discriminate or mislead customers.

Yet a clear gap remains between ambition and readiness. Ecosystm research shows nearly 77% of Australian organisations acknowledge progress in piloting real-world use cases but worry they’re falling behind due to weak governance and poor-quality data.

The conversation around AI in Australia is evolving beyond productivity to include building trust. Success is now measured by the confidence regulators, customers, and communities have in AI systems. The path forward is clear: AI must drive innovation while upholding principles of fairness, transparency, and accountability.

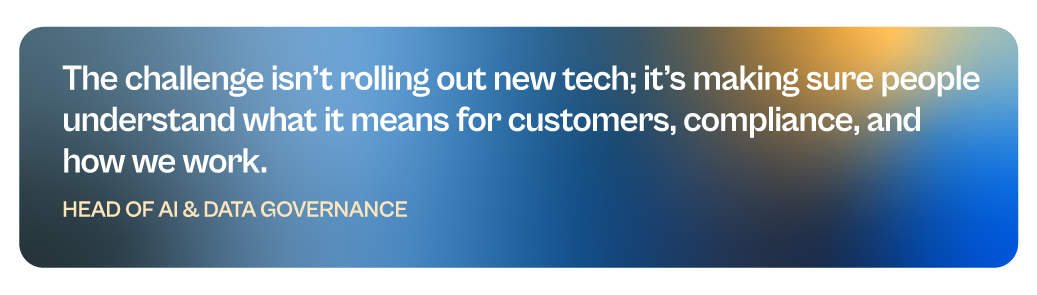

2. The New AI Skillset: Where Data Science Meets Compliance and Context

Australia is on track to face a shortfall of 250,000 skilled workers in tech and business by 2030, according to the Future Skills Organisation. But the gap isn’t just in coders or engineers; it’s in hybrid talent: professionals who can connect AI development with regulatory, ethical, and commercial understanding.

In sectors like finance, AI adoption has stalled not due to lack of tools, but due to a lack of people who can interpret financial regulations and translate them into data science requirements. The same challenge affects healthcare, where digital transformation projects often slow down because technical teams lack domain-specific compliance and risk expertise.

While skilled migration has rebounded post-pandemic, the domestic pipeline remains limited. In response, organisations like Microsoft and Commonwealth Bank are investing in cross-skilling employees in AI, cloud, and risk management. Government initiatives such as CSIRO’s Responsible AI program and UNSW’s AI education efforts are also working to build talent fluent in both technology and ethics.

Despite these efforts, Australia’s shortage of hybrid talent remains a critical bottleneck, shaping not just how fast AI is adopted, but how responsibly and effectively it is deployed.

3. Beyond Coverage: Closing the Digital Gap for Regional Australia

Australia’s vast geography creates a uniquely local digital divide. Despite the National Broadband Network (NBN) rollout, many regional areas still face slow speeds and outages. The 2023 Regional Telecommunications Review found that over 2.8 million Australians remain without reliable internet access. Industries suffer tangible impacts. GrainCorp, a major agribusiness, uses AI to communicate with workers during the harvest season, but regional connectivity gaps hinder real-time monitoring and analytics. In healthcare, the Royal Flying Doctor Service reports that poor internet reliability in remote areas undermines telehealth consultations, particularly crucial for Indigenous communities.

Efforts to address these gaps are underway. Telstra launched satellite services through partnerships with Starlink and OneWeb to cover remote zones. However, these solutions often come with prohibitive costs, particularly for smaller businesses, farms, and community organisations that cannot afford private network infrastructure.

The implications are clear: without reliable and affordable internet, regional enterprises will struggle to adopt AI, cloud-based systems, and digital tools that drive efficiency and equity. The next step must be a coordinated approach involving government, telecom providers, and industry, focused not just on coverage, but on quality, affordability, and support for local innovation. Bridging this digital divide is not simply about infrastructure, it’s about ensuring inclusive access to the tools that power modern business and essential services.

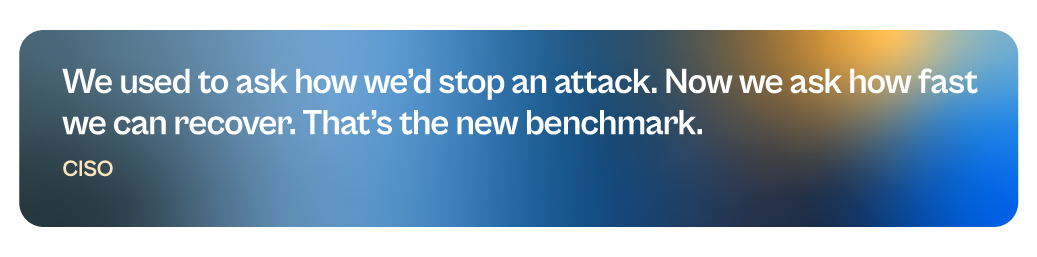

4. Resilience Over Defence: Australia’s Evolving Cybersecurity Focus

Australia’s cyber landscape has shifted sharply following major breaches like Optus, Medibank, and Latitude Financial, which pushed cybersecurity to the top of national agendas. In response, regulators and organisations have adopted a more urgent, coordinated stance. Under the Security of Critical Infrastructure (SOCI) Act, critical sectors must now report serious incidents within hours, enabling faster, government-led responses and stronger collective resilience.

Organisations across sectors are stepping up their defences, moving from reactive measures to proactive preparedness. NAB confirmed that it spends over USD 150M annually on cybersecurity, focusing on real-time threat hunting, simulation exercises, and red teaming. Telstra continues to run annual “cyber war games” involving IT, legal, and crisis communications teams to prepare for worst-case scenarios.

This collective focus signals a broader shift across Australian industries: cybersecurity maturity is no longer judged by perimeter defence alone. Instead, resilience – an organisation’s ability to detect, respond, and recover swiftly – is now the benchmark for protecting critical assets in an increasingly complex threat landscape.

5. Designing for the Long Term: Sustainability as a Core Capability

Organisations across Australia are under growing pressure – not only from regulators, but also from investors, customers, and communities – to demonstrate that their digital strategies are delivering real environmental and social outcomes. The bar has shifted from ESG disclosure to ESG performance. Technology is no longer just an efficiency lever; it’s expected to be a catalyst for sustainability transformation.

This expectation is especially acute in Australia’s core industries, where environmental impact is both material and highly scrutinised. In mining, for example, Rio Tinto’s 20-year renewable energy deal with Edify Energy aims to cut emissions by up to 70% at its Queensland aluminium operations by 2028. But the focus on transition is not limited to high-emission sectors. In financial services, institutions are actively supporting the shift to a low-carbon economy, from setting long-term net-zero targets to aligning lending practices with climate goals, including phasing out support for high-emission assets.

Yet for many, the path forward is still fragmented. ESG data often sits in silos, legacy systems constrain visibility, and ownership of sustainability metrics is scattered. Digital transformation efforts that treat ESG as an add-on, rather than embedding it into the foundations of data, governance, and decision-making, risk missing the mark. Australia’s next digital frontier will be measured not just by innovation, but by how effectively it enables a low-carbon, inclusive, and resilient economy.

Shaping Australia’s Digital Future

Australia’s technology journey is accelerating, but significant challenges must be addressed to unlock its full potential. Moving beyond basic digitalisation, the country is embracing advanced technologies as essential drivers of economic growth and productivity. Strong government initiatives and investments are creating a foundation for innovation and building a highly skilled digital workforce. However, overcoming barriers such as talent shortages, infrastructure gaps, and governance complexities is critical. Only by tackling these obstacles head-on and embedding technology deeply across organisations of all sizes can Australia transform automation into true data-driven autonomy and new business models, securing its position as a global digital leader.

GenAI has taken the world by storm, with organisations big and small eager to pilot use cases for automation and productivity boosts. Tech giants like Google, AWS, and Microsoft are offering cloud-based GenAI tools, but the demand is straining current infrastructure capabilities needed for training and deploying large language models (LLMs) like ChatGPT and Bard.

Understanding the Demand for Chips

The microchip manufacturing process is intricate, involving hundreds of steps and spanning up to four months from design to mass production. The significant expense and lengthy manufacturing process for semiconductor plants have led to global demand surpassing supply. This imbalance affects technology companies, automakers, and other chip users, causing production slowdowns.

Supply chain disruptions, raw material shortages (such as rare earth metals), and geopolitical situations have also had a fair role to play in chip shortages. For example, restrictions by the US on China’s largest chip manufacturer, SMIC, made it harder for them to sell to several organisations with American ties. This triggered a ripple effect, prompting tech vendors to start hoarding hardware, and worsening supply challenges.

As AI advances and organisations start exploring GenAI, specialised AI chips are becoming the need of the hour to meet their immense computing demands. AI chips can include graphics processing units (GPUs), application-specific integrated circuits (ASICs), and field-programmable gate arrays (FPGAs). These specialised AI accelerators can be tens or even thousands of times faster and more efficient than CPUs when it comes to AI workloads.

The surge in GenAI adoption across industries has heightened the demand for improved chip packaging, as advanced AI algorithms require more powerful and specialised hardware. Effective packaging solutions must manage heat and power consumption for optimal performance. TSMC, one of the world’s largest chipmakers, announced a shortage in advanced chip packaging capacity at the end of 2023, that is expected to persist through 2024.

The scarcity of essential hardware, limited manufacturing capacity, and AI packaging shortages have impacted tech providers. Microsoft acknowledged the AI chip crunch as a potential risk factor in their 2023 annual report, emphasising the need to expand data centre locations and server capacity to meet customer demands, particularly for AI services. The chip squeeze has highlighted the dependency of tech giants on semiconductor suppliers. To address this, companies like Amazon and Apple are investing heavily in internal chip design and production, to reduce dependence on large players such as Nvidia – the current leader in AI chip sales.

How are Chipmakers Responding?

NVIDIA, one of the largest manufacturers of GPUs, has been forced to pivot its strategy in response to this shortage. The company has shifted focus towards developing chips specifically designed to handle complex AI workloads, such as the A100 and V100 GPUs. These AI accelerators feature specialised hardware like tensor cores optimised for AI computations, high memory bandwidth, and native support for AI software frameworks.

While this move positions NVIDIA at the forefront of the AI hardware race, experts say that it comes at a significant cost. By reallocating resources towards AI-specific GPUs, the company’s ability to meet the demand for consumer-grade GPUs has been severely impacted. This strategic shift has worsened the ongoing GPU shortage, further straining the market dynamics surrounding GPU availability and demand.

Others like Intel, a stalwart in traditional CPUs, are expanding into AI, edge computing, and autonomous systems. A significant competitor to Intel in high-performance computing, AMD acquired Xilinx to offer integrated solutions combining high-performance central processing units (CPUs) and programmable logic devices.

Global Resolve Key to Address Shortages

Governments worldwide are boosting chip capacity to tackle the semiconductor crisis and fortify supply chains. Initiatives like the CHIPS for America Act and the European Chips Act aim to bolster domestic semiconductor production through investments and incentives. Leading manufacturers like TSMC and Samsung are also expanding production capacities, reflecting a global consensus on self-reliance and supply chain diversification. Asian governments are similarly investing in semiconductor manufacturing to address shortages and enhance their global market presence.

Japan is providing generous government subsidies and incentives to attract major foreign chipmakers such as TSMC, Samsung, and Micron to invest and build advanced semiconductor plants in the country. Subsidies have helped to bring greenfield investments in Japan’s chip sector in recent years. TSMC alone is investing over USD 20 billion to build two cutting-edge plants in Kumamoto by 2027. The government has earmarked around USD 13 billion just in this fiscal year to support the semiconductor industry.

Moreover, Japan’s collaboration with the US and the establishment of Rapidus, a memory chip firm, backed by major corporations, further show its ambitions to revitalise its semiconductor industry. Japan is also looking into advancements in semiconductor materials like silicon carbide (SiC) and gallium nitride (GaN) – crucial for powering electric vehicles, renewable energy systems, and 5G technology.

South Korea. While Taiwan holds the lead in semiconductor manufacturing volume, South Korea dominates the memory chip sector, largely due to Samsung. The country is also spending USD 470 billion over the next 23 years to build the world’s largest semiconductor “mega cluster” covering 21,000 hectares in Gyeonggi Province near Seoul. The ambitious project, a partnership with Samsung and SK Hynix, will centralise and boost self-sufficiency in chip materials and components to 50% by 2030. The mega cluster is South Korea’s bold plan to cement its position as a global semiconductor leader and reduce dependence on the US amidst growing geopolitical tensions.

Vietnam. Vietnam is actively positioning itself to become a major player in the global semiconductor supply chain amid the push to diversify away from China. The Southeast Asian nation is offering tax incentives, investing in training tens of thousands of semiconductor engineers, and encouraging major chip firms like Samsung, Nvidia, and Amkor to set up production facilities and design centres. However, Vietnam faces challenges such as a limited pool of skilled labour, outdated energy infrastructure leading to power shortages in key manufacturing hubs, and competition from other regional players like Taiwan and Singapore that are also vying for semiconductor investments.

The Potential of SLMs in Addressing Infrastructure Challenges

Small language models (SLMs) offer reduced computational requirements compared to larger models, potentially alleviating strain on semiconductor supply chains by deploying on smaller, specialised hardware.

Innovative SLMs like Google’s Gemini Nano and Mistral AI’s Mixtral 8x7B enhance efficiency, running on modest hardware, unlike their larger counterparts. Gemini Nano is integrated into Bard and available on Pixel 8 smartphones, while Mixtral 8x7B supports multiple languages and suits tasks like classification and customer support.

The shift towards smaller AI models can be pivotal to the AI landscape, democratising AI and ensuring accessibility and sustainability. While they may not be able to handle complex tasks as well as LLMs yet, the ability of SLMs to balance model size, compute power, and ethical considerations will shape the future of AI development.